History: Intel

The Traitorous Eight

The Intel story started in 1957, when eight young scientists, ages 26 to 33, six of them holding PhDs, walked out of William Shockley’s toxic laboratory in Mountain View, California.

Shockley, the co-inventor of the transistor and 1956 Nobel laureate, had recruited brilliant talent but was an erratic, authoritarian manager obsessed with commercially inviable products. He reportedly put his employees on lie detectors!

On 18 September 1957, these eight men defected together:

Julius Blank (Mechanical Engineer)

Victor Grinich (Electronics Engineer)

Jean Hoerni (Physicist)

Eugene Kleiner (Engineer)

Jay Last (Physicist)

Gordon Moore (Chemist)

Robert Noyce (Physicist)

Sheldon Roberts (Metallurgist)

Shockley branded them as the Traitorous Eight.

These eight young men with financial backing from Sherman Fairchild founded Fairchild Semiconductor. By the mid 1960s, the company grew to 12,000 employees and $130m in annual sales, becoming second only to Texas Instruments.

Among the great achievements of Fairchild, there were 2 that stood out:

Jean Hoerni’s 1959 planar process revolutionized transistor manufacturing.

Robert Noyce built on Hoerni's planar process and invented the monolithic integrated circuit (IC), which created the silicon IC industry.

Fairchild eventually spawned over 100 spin-off companies, including Intel, AMD, National Semiconductor, and Xilinx.

However, the parent company, Fairchild Camera and Instruments didn’t want to reinvest profits back into R&D for semiconductors.

Robert Noyce and Gordon Moore were frustrated and quit. They partnered and founded Intel on 18 July 1968. Arthur Rock, provided the financing and served as Chairman. They raised $2.5m in convertible debentures from private investors, and each founder put up $250,000 of their own money.

To get the name Intel, they paid $15,000 to buy the name from a Midwestern hotel chain (named Intelco).

The original mission was semiconductor memory: Moore proposed that silicon-based memory chips could replace the magnetic core memory then standard in computers. Noyce’s business plan was famously one page long — the real equity was the founders’ reputation.

Holocaust Survivor: Andrew Grove

The author of the 1996 book Only The Paranoid Survive, Andrew Grove (birth name: András István Gróf), joined Intel as employee #3 on its day of incorporation. He was a Holocaust survivor who escaped Hungary during the 1956 revolution and arrived in America at age 20 with virtually nothing. Grove went on to get his PhD in chemical engineering from UC Berkeley. He had worked under Gordon Moore at Fairchild and followed him to Intel.

Grove rose through the ranks as Director of Engineering (1968), President and COO (1979), and CEO (1987). His management philosophy demanded open, vigorous debate regardless of hierarchy.

There were no executive perks: no reserved parking, no fancy offices, no private dining rooms.

He taught at Stanford’s Graduate School of Business for 24 years and was named Time Magazine’s Man of the Year for 1997.

Intel’s early product breakthroughs were remarkable. The 1103 DRAM (1970), a 1,024-bit dynamic RAM chip, became the bestselling semiconductor memory chip in the world by 1972, replacing magnetic core memory and establishing Intel’s revenue base.

The Intel 4004 (1971) was the world’s first commercial general-purpose microprocessor: 4-bit chip with 2,300 transistors originally designed for a Japanese calculator company Busicom. Intel bought back the design rights for just $60,000 when Busicom hit financial trouble. The 8080 (1974) 8-bit processor powered the Altair 8800 and inaugurated the personal computing (PC) revolution.

Gordon Moore's 1965 paper argued that the number of components would double every year. This was later revised to doubling every 2 years.

By 1975, a new memory chip contained exactly 65,536 transistors, accurate to within a single percentage point of Moore’s decade-old prediction. This became what is now known as “Moore's Law”, coined in 1970 by Caltech professor Carver Mead. This became a self-fulfilling prophecy that set the industry’s R&D cadence for the next 50 years.

Intel created the DRAM market and held effectively 100% market share in the early 1970s, still controlling roughly 83% as late as 1974. But by the early 1980s, Japanese manufacturers (NEC, Hitachi, Fujitsu) were producing memory chips with yields up to 40% higher, with consistently superior quality that Hewlett-Packard publicly confirmed.

Japanese firms had access to cheap government-backed capital, operated highly automated fabs, and competed with ruthless aggression. Grove once obtained an internal Japanese competitor memo directing salespeople:

Win with the 10% rule… Find AMD and Intel sockets… Quote 10% below their price… If they requote, go 10% AGAIN… Don’t quit until you WIN!

Only The Paranoid Survive (1996)

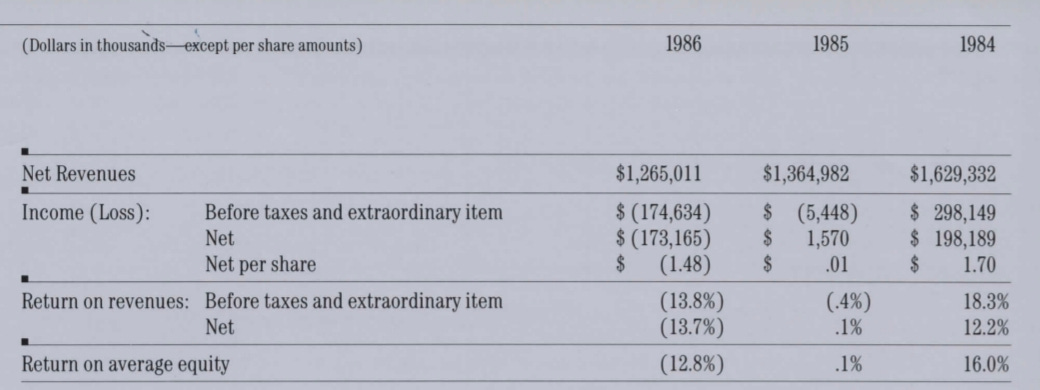

Competition intensified through the mid-1980s. Intel’s DRAM market share collapsed from 83% in 1974 to 1.3% by 1984.

In 1986, Intel faced its very first major financial loss of $173m. They closed 8 plants and retrenched one-third of their employees (7,200 people).

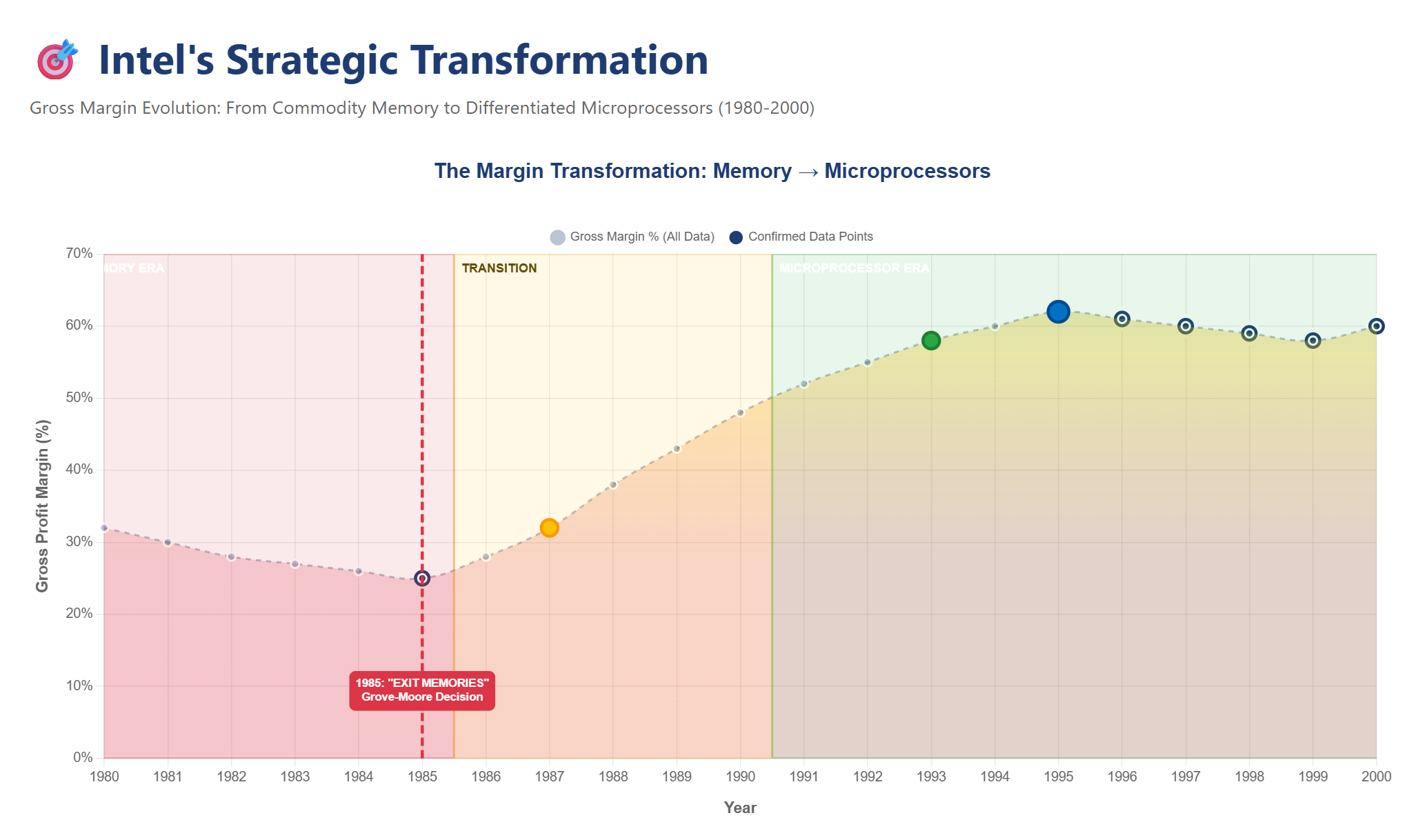

Among the endless debates on how to compete with the Japanese, Moore and Grove decisively exited the memory market.

They pivoted toward the x86 processor architecture, born with the 8086 chip in 1978. IBM had chosen the Intel 8088 for the original IBM PC because Intel offered better pricing, adequate supply, and the 8-bit external bus allowed use of cheaper peripheral components. The IBM PC’s open architecture spawned the clone market, and the installed base of x86 software created an ecosystem lock-in that made switching architectures prohibitively expensive.

Grove’s most consequential strategic decision for the microprocessor era was making the 80386 (i386) sole-sourced. Previously, IBM had demanded multiple suppliers, forcing Intel to license x86 to AMD and others.

For the 32-bit i386, Grove gambled that Intel could manufacture reliably on its own.

Copy Exactly: Craig Barrett

Craig Barrett, who would become the successor of Andrew Grove in 1998, was tasked to overhaul manufacturing. He implemented the famous “Copy Exactly” methodology, replicating fab processes identically across plants, making sole-sourcing credible. This decision meant all profits and market control stayed with Intel, setting the foundation for the 1990s golden era.

The strategy and execution was brilliant and Intel gross margins doubled:

On 22 March 1993, the first Pentium processor was launched equipped with x86 chip, with 3.1 million transistors priced at $878.

Intel enjoyed a massive 90% market share and became the world’s largest semiconductor company. Throughout the dot-com craze they launched these iconic products:

November 1995: Pentium Pro

May 1997: Pentium II

February 1999: Pentium III

Intel would hold on to the #1 position for CPU producer until today (2026)!

On the marketing front, the Intel Inside campaign in 1991 was perhaps the best marketing effort in business history. Intel provided OEMs a 6% rebate on processor purchases, allocated to a Joint Marketing Fund covering up to 50% of advertising costs. The OEM must display the Intel Inside logo on products and advertisements.

By the end of 1992, over 500 OEMs had joined the program, with 70% of eligible ads carrying the logo. Intel’s advertising spend escalated from an initial investment of $250m to $1.2b by 1997.

Intel went from being a chip hidden inside a PC to a household name.

Revenues went from $3.9b in 1990 to $20.9b in 1996. Net income was $5.2b, nearly 25% net margins. By 2000, Intel had $33.7b of revenues.

The “Wintel” virtuous cycle between Microsoft Windows and Intel chips was formidable; they optimized for each other creating a virtuous upgrade cycle that powered the vast majority of the world’s PC.

Each new Windows version demanded more processing power; each new Intel chip enabled more capable software.

But the journey was not all smooth. The Pentium FDIV bug, discovered internally in 1994 and publicly exposed by Lynchburg College math professor Thomas Nicely, caused incorrect results in certain floating-point divisions due to 5 missing entries in a lookup table. Intel initially dismissed it, claiming a typical user would encounter an error only once every 27,000 years. IBM contradicted this, claiming errors every 24 days, and halted all sales of Intel-powered PCs. On 20 December 1994, Intel reversed course and offered free replacements. The $475m pre-tax charge (1995) was Intel’s first CPU recall.

In terms of competition, AMD was the only meaningful rival with 10—15% market share through most of the decade. AMD’s products were competitive on price but not performance. Only the Athlon (June 1999) matched Intel, and AMD narrowly beat Intel to the 1GHz milestone in March 2000.

In the midst of the dot-com mania, Intel’s market cap under Andrew Grove’s leadership grew 45x from $4b (1987) to $197b (1998). He stepped down as CEO and Craig Barrett took over, then 2 years later the dot-com bubble burst and Intel’s shares lost over 80% from 2000—2003.

Regardless, Intel continued to maintain leadership by staying ahead of nodes manufacturing technology.

2006: 65nm Core 2 Duo

2007: 45nm Penryn

2010: 32nm Westmere

2012: 22nm Ivy Bridge

2014: 14nm Broadwell

The 22nm Ivy Bridge was a landmark: Intel became the first company to produce FinFET (Fin Field-Effect Transistor) transistors at commercial scale, a full 3 years before TSMC and Samsung adopted FinFET at 16nm/14nm in 2015. In a 2014 presentation, Intel claimed manufacturing leads of 3.25 years in strained silicon, 3.75 years in high-K metal gate technology, and 3.5 years in 3D transistors (TSMC was still on planar transistors).

Intel’s server CPU dominance was even more absolute. The Xeon line held over 99% of the server CPU market through the 2000s and into the mid-2010s, with estimated margins of 60—70%. AMD’s Opteron was briefly competitive (2003—2006) but faded after Intel’s Xeon 5500 (2009) restored clear leadership. AMD did not become competitive in servers again until the EPYC launch in 2017.

The MBA Leader: Paul Otellini

The leadership transition from engineer-CEOs to business-CEOs tracks perfectly with Intel’s decline. The first 4 CEOs were all scientists and engineers. The 5ᵗʰ CEO Paul Otellini was the first one without a technical degree.

Otellini had a BA in Economics and MBA from UC Berkeley. He joined Intel in the same year as his predecessor, Craig Barrett, in 1974. Otellini managed the IBM account in 1980, served as HR chief in 1989, ran the Pentium development as Head of Microprocessor Products Group, and became President/COO before taking over the CEO role in 2005.

Although Intel’s revenues grew from $34b to $53b during his 8 year tenure, he made a strategic error by declining Apple’s request for ARM-based chips for their iPhone.

With a background in finance, Otellini forecasted the cost and volumes but Apple was only willing to pay a certain price that was below his forecasted cost. It turns out that his cost estimates were wrong and volumes were 100x of what anyone thought.

Compounding this error, Intel sold its XScale ARM processor business to Marvell for $600m in 2006, exiting the ARM mobile market entirely just as the smartphone revolution started.

This opened a wide door of opportunity for TSMC.

In 2010, Apple’s COO Jeff Williams had dinner with Morris Chang, planting the seeds of a partnership. By 2014, TSMC manufactured Apple’s A8 chip on its 20nm process for the iPhone 6.

By 2016, TSMC was Apple’s exclusive chip manufacturer, and Apple sent $2b per year to TSMC in 2014, this revenue stream for TSMC grew 12x to $24b in 2025. In March 2017, TSMC market cap surpassed Intel for the first time.

Four Years Late: Brian Krzanich

The 6ᵗʰ CEO, Brian Krzanich, took over leadership in 2013. He had a degree in chemistry and joined Intel as an engineer in 1982, served as COO before being promoted to CEO. Unfortunately, his leadership failed in the area of manufacturing. The 10nm node, originally targeted for H2 2016, attempted an ambitious 2.7x density increase over 14nm using DUV rather than adopting EUV lithography.

Meanwhile, TSMC executed its node transitions on schedule, below are the years of full volume production:

2018: N7 (7nm, DUV)

2019: N7+ (7nm, first commercial EUV process)

2020: N5 (5nm, full EUV)

2022: N3 (3nm)

Samsung also moved to EUV, beginning mass production of its 7nm in 2019.

The late adoption of EUV caused a cascading series of delays and Intel was stuck on 14nm for 7 years (2014—2021)! Only until Meteor Lake (2023) did Intel mass produce their first EUV process, by then Intel was 4 years behind.

In 2017, Krzanich exercised stock options and sold his shares worth $24m after Intel learned that all its chips sold in the last decade had a security vulnerability. In 2018, an investigation was launched after an employee reported that Krzanich engaged in a consensual relationship with a subordinate. On 21 June 2018, he was ousted as the CEO.

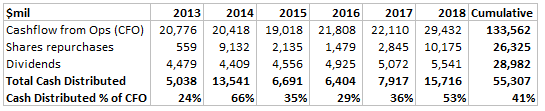

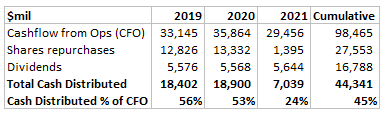

During his tenure, Intel aggressively repurchased shares and paid dividends. Cumulatively, 41% of operating cash flow was returned to shareholders instead of reinvested into Intel’s manufacturing capabilities:

The financial optimizing mindset destroyed the manufacturing-first culture that the founders of Intel built.

Another MBA: Bob Swan

Apparently, Intel didn’t learn their lesson from letting finance executives run the company. Bob Swan joined Intel as CFO in 2016 and was appointed CEO from 2019 to 2021. Another finance background CEO, he returned more cash to shareholders:

In July 2020, Swan disclosed that their 7nm process was approximately 12 months behind target. Intel’s manufacturing problems were worsening. An engineer had not run Intel in nearly two decades, and it showed.

Prodigy Returns: Pat Gelsinger

Pat Gelsinger grew up in rural Pennsylvania and was raised on family farms. As a teenager, he received a high score on a Lincoln Tech electronics test and won a scholarship. At a tender age of 18, he joined Intel as a quality control technician. While at Intel, Gelsinger earned his degree in electrical engineering and his master’s degree from Stanford.

At Intel, he became a design engineer on the i386 team. He became the chief architect of the 80486 processor at age 25, his initials “PG” were etched into every i386 die. Andrew Grove mentored him throughout his career, and at 32, Gelsinger became Intel’s youngest VP. He was named Intel’s first Chief Technology Officer in 2001.

Pat Gelsinger is nothing short of prodigal.

He left Intel in 2009 to join EMC as President/COO, then became CEO of VMware in August 2012. His tenure there was a massive success.

Gelsinger returned to Intel as CEO on 15 February 2021, succeeding Bob Swan, following activist pressure from Dan Loeb (Third Point Management).

The first thing he did was to rebuild Intel’s manufacturing leadership while simultaneously becoming a contract chip manufacturer for outside customers through a new business unit called Intel Foundry Services (IFS).

He announced an ambitious “five nodes in four years” roadmap. Committed to huge capital investments:

$20b for 2 new Arizona fabs

$20b for 2 Ohio fabs

€30b for Magdeburg, Germany fab

€17b for Ireland Fab 34

$3.5b for advanced packing in New Mexico

Total US investments exceeded $100b.

However, the execution was not there.

Intel won a $3b Department of Defense contract and announced Amazon Web Services as a foundry customer, but failed to land a truly transformative external commercial client.

The attempted acquisition of Tower Semiconductor, which would have bolstered foundry capabilities, was blocked by Chinese regulators.

Revenue peaked at $79b in 2021 but declined sharply: $63b (2022), $54b (2023), $53b billion (2024).

IFS lost $7b in 2023. Q3 2024 reported $16.6b loss.

Intel suspended dividends, retrenched 15% of workforce (15,000 job cuts).

The stock was removed from the Dow Jones index in November 2024, replaced by Nvidia.

The Board gave up on Pat and told him to leave. This was a mistake as manufacturing capabilities takes years to rebuild, and Gelsinger was doing the right thing. The short term financial thinking was the very cause of Intel’s problems in the first place.

In fact, the current 18A process (2nm) that managed to pull Intel back into the race, was Gelsinger’s plan.

Outsider: Lip Bu Tan

Intel’s current CEO, Lip Bu Tan, took the role on 12 March 2025. He’s the first outsider CEO.

Lip Bu’s defining achievement was transforming Cadence Design Systems, where he served as CEO from 2009 to 2021. The company provides Electronic Design Automation (EDA) software which helps chip designers in circuit simulation. During his tenure, Cadence stock price grew 40x. In 2022, he won the Robert N. Noyce Award in 2022, the industry’s highest honour.

Lip Bu had served on Intel’s board from September 2022 but resigned abruptly on August 2024, reportedly frustrated with Intel’s bloated workforce, bureaucratic culture, and attitude toward contract manufacturing.

Entering as an outsider, Lip Bu’s message was clear, in an email to employees he wrote:

Under my leadership, Intel will be an engineering-focused company. We will push ourselves to develop the best products, listen intently to our customers and hold ourselves accountable.

In a July 2025 memo, he wrote:

Over the past several years, the company invested too much, too soon — without adequate demand. In the process, our factory footprint became needlessly fragmented and underutilized. We must correct our course.

Lip Bu’s direction is the same as Gelsinger. But his execution was different.

Cancelled Magdeburg and Wroclaw fab projects.

Slowed Ohio construction.

15—25% workforce cuts.

Demand driven approach, only investing in new capacity only when customer commitments are confirmed.

However, Intel’s foundry operations were still losing $10.3b in 2025. The unknown is whether they can convert manufacturing into commercial success before accumulated losses test the Board’s patience again.

Last Notes

Intel’s story is one of extraordinary invention, near-fatal complacency, and an uncertain but technologically promising resurrection.

The company that created the DRAM chip, the microprocessor, and the modern PC ecosystem nearly destroyed itself through a decade of financial engineering, missed inflection points in mobile, and manufacturing hubris.

Three facts frame the challenge ahead:

$152b spent on stock buybacks since 1990

$11.1b invested by the US government to keep Intel alive

15+ foundry customers for TSMC N2 process, while Intel has only a few for 18A.