History: Bernie Madoff

Intro

Bernard “Bernie” Madoff ran the largest Ponzi scheme in modern history. At its peak, it was reported to have $65b of assets.

To be an investor with Bernie Madoff was to be a member of an elite club, a circle that included Hollywood celebrities, titans of industry, and the world’s most venerable charities. His firm, Bernard L. Madoff Investment Securities (BLMIS), was a technological and market-making powerhouse, ranking as the sixth-largest market maker for S&P500 stocks.

Madoff himself was a legend, a former Chairman of the NASDAQ, a pioneer of the very electronic trading systems that formed the bedrock of modern finance, and a respected elder statesman whose counsel was sought by regulators.

The $65b figure attached to his name represented not the value of a brilliant investment portfolio, but the sum of decades of lies printed on paper statements and mailed to thousands of victims around the globe.

The central question of this saga is not just that a fraud occurred, but how this specific man, so deeply woven into the fabric of the financial system, could orchestrate a deception of such magnitude for so long?

This is the story of a journey into the heart of a colossal lie.

Foundations

The bedrock of Madoff’s fraud was the unimpeachable legitimacy of his public career. His carefully cultivated persona as a market innovator and Wall Street elder statesman was not merely a cover for his crimes; it was the essential ingredient that made them possible.

He built a reputation so powerful that it created a cognitive shield, deflecting skepticism and blinding both investors and regulators for decades.

Bernard Lawrence Madoff was born in Queens, New York, in 1938, to parents who had their own troubled history with finance. His father, Ralph, and mother, Sylvia, ran a small broker-dealer operation called Gibraltar Securities out of their home. But the firm was shut down by the Securities and Exchange Commission (SEC) for failing to file required financial reports, earning the family a reputation for shady dealings.

Madoff’s own beginnings were modest. He worked as a lifeguard and installed sprinkler systems to save money, attended Hofstra University, and briefly enrolled at Brooklyn Law School before dropping out.

In 1960, with $5,000 of his own savings and a $50,000 loan from his father-in-law, Madoff launched Bernard L. Madoff Investment Securities (BLMIS).

Early Career

Madoff began his career not as a money manager, but as a market maker in the gritty world of “penny stocks” traded on the over-the-counter (OTC) market. In the 1960s, it relied on paper “Pink Sheets” and telephone negotiations. It was here that Madoff established his legitimate genius.

He was a visionary who recognized the transformative power of technology. BLMIS became a key early adopter and developer of the computer systems that automated trading, helping to transform the loose network of OTC dealers into the world’s first electronic stock exchange: the NASDAQ.

This role as a technological pioneer was the core of his legitimate fame. He made trading faster, cheaper, and more efficient. He also pioneered the controversial but legal practice of “payment for order flow” in which he paid retail brokerage firms a small fee per share to execute their customers’ orders through his firm.

This strategy allowed BLMIS to capture enormous trading volume, at one point handling as much as 9% of all trades on the New York Stock Exchange.

Madoff’s success was legitimate: his market-making business was genuinely innovative and profitable.

This legitimate success was inextricably linked to the fraud that followed. His deep, technical knowledge of market structure, gained from decades of market-making, gave him an unparalleled understanding of how the system worked. But more importantly, how its regulatory loopholes could be exploited.

He would later serve as non-executive chairman of NASDAQ, creating a powerful cognitive bias. Regulators and investors alike found it nearly impossible to conceive that a man who had helped write the rules of the game would be its most flagrant cheater.

The legitimacy did not just hide the fraud; it actively nourished and protected it.

Social Engineering

Madoff masterfully leveraged his success into an unassailable reputation. He served three terms as the non-executive chairman of NASDAQ in 1990, 1991, and 1993, advised the SEC on electronic trading, and was held in very high regard by colleagues and regulators who saw him as an industry expert.

This reputation was amplified by a brilliant marketing strategy built on exclusivity.

Gaining access to Madoff’s secretive investment advisory business was portrayed as a rare privilege. He often required a minimum investment of $1m and was known to turn potential investors away; a tactic taken from the luxury business playbook.

This strategy was a masterstroke of social engineering, playing directly to the egos of the wealthy. He cultivated friendships in the exclusive social circles of Manhattan and the Palm Beach Country Club, using the glowing recommendations of his high networth clients to attract an ever-expanding network of new capital.

His story of being a “poor kid from Queens” who outsmarted the Wall Street establishment was a powerful part of this mystique. It positioned him as a brilliant outsider who had discovered a secret to beating the market.

The 17th Floor

Madoff’s firm operated in 3 separate floors in the Manhattan Lipstick Building.

The legitimate market-making and proprietary trading businesses occupied floors 18 and 19.

Hidden away on the 17th floor was the secret engine of the fraud: the investment advisory business. This operation was staffed by a small, loyal group of employees. It was kept a closely guarded secret from the vast majority of the firm’s personnel, including Madoff’s own sons who worked on the legitimate trading floors.

Madoff’s investment advisory arm, which managed billions of dollars, was never registered with the SEC. A fact that was accepted as an “open secret on Wall Street”.

How the Ponzi Worked

Madoff’s operation was a classic Ponzi scheme, in which money from new investors is used to pay “returns” to earlier investors, with no actual investment activity generating profits.

On the 17th floor, this was the reality. Despite account statements showing billions of dollars in blue-chip stocks and options, not a single security was ever bought or sold.

The entire operational flow was simple. All incoming investor funds were deposited into a single business account at Chase Manhattan Bank: Account 703. When an investor wished to make a withdrawal, the money was simply paid out from this massive pool of cash, which was constantly being replenished by new investments.

The entire $65b enterprise was nothing more than a checking account.

The fraud involved no complex algorithms or sophisticated trading; it was a primitive scheme of falsifying paper records.

This simplicity was its greatest strength. It was easy to control, left minimal digital traces, and was perfectly hidden behind the dazzling curtain of technological sophistication projected by his legitimate business on the floors above.

Employees like Madoff’s longtime secretary, Annette Bongiorno, would use The Wall Street Journal to find historical stock prices on days when the market had performed well.

They would then “backdate” fictitious trades, creating records to show that clients had “bought” stocks at their lowest price for a given day and “sold” them at their highest, generating the steady returns Madoff had promised.

This fabricated data was then entered into a computer system, which generated flawlessly professional-looking monthly statements and trade confirmations. These documents, mailed by the thousands, were the tangible proof of Madoff’s genius and the sole basis for his clients’ belief that their fortunes were growing.

The Options Pitch

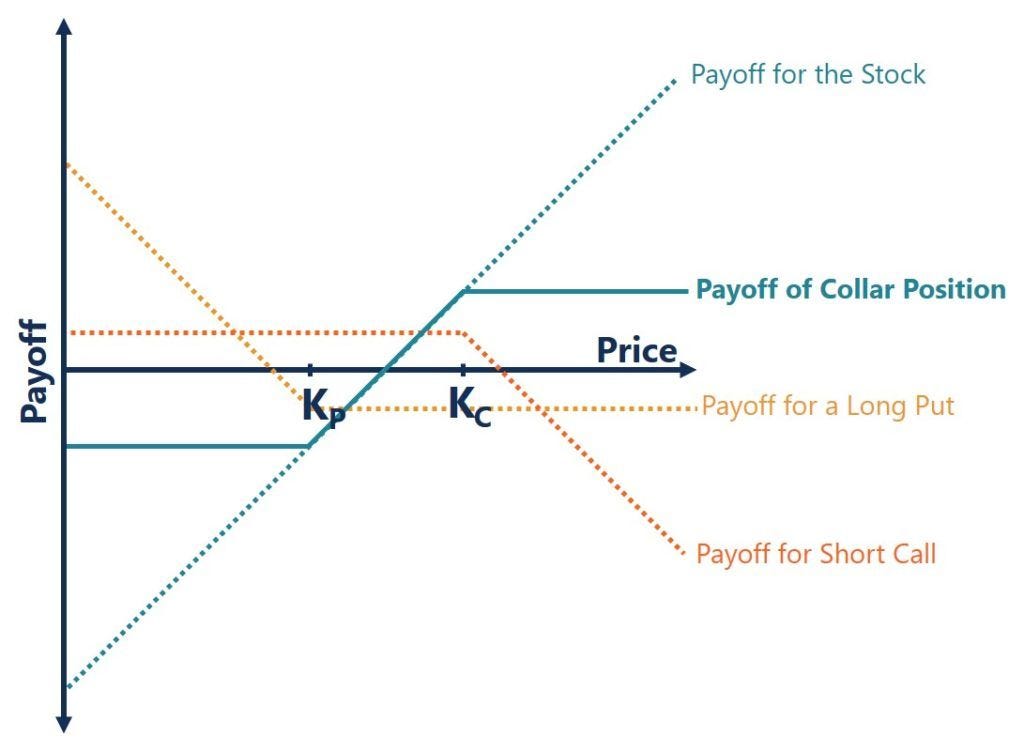

To sell his fraud to a sophisticated clientele, Madoff needed more than just a reputation. He had to come up with an investment strategy.

He chose a legitimate but complex investment approach known as the “split-strike conversion”. This strategy was technical enough to sound credible, yet opaque enough to discourage scrutiny.

This was how Madoff explained it in 3 steps:

Buy a basket of blue-chip stocks from the S&P100 index that would mimic the broader market’s movements.

Sell out-of-the-money call options on the index. This generates premium income and caps the potential upside of the stock portfolio.

Using the income from #2 to buy out-of-the-money put options on the index. This acts as insurance, establishing a floor that protects the portfolio from significant market downturns.

This is essentially a collar strategy:

Madoff’s pitch was that his unique skill in timing the market and picking stocks allowed him to execute this strategy to perfection, generating remarkably consistent returns of 10-12% annually, year after year, with almost no volatility, regardless of what the market was doing.

When you have multi-millions of dollars, this promise of steady 10% returns every year was the dream.

Harry Markopolos

The first person to systematically prove the impossibility of Madoff’s claims was Harry Markopolos, a quantitative financial analyst from Boston.

In 1999, his boss at a rival firm asked him to reverse-engineer Madoff’s strategy to create a competing product. Within hours of analyzing the numbers, Markopolos concluded that Madoff was a fraud. Sadly, his reasoning repeatedly fell on the deaf ears of the SEC.

Options Market Volume

The most obvious piece of evidence was the sheer lack of available options. For Madoff’s strategy to work at the scale he claimed (tens of billions of dollars), he would have needed to buy and sell a huge volume of S&P100 index options.

Markopolos demonstrated that the total trading volume of these options on the entire Chicago Board Options Exchange was often a small fraction of what Madoff would have needed for his hedges alone. The market was simply not big enough for him to be telling the truth.

Flawless Performance

Madoff’s reported returns was a smooth, steady climb with almost no down months. Anyone with a basic understanding of financial markets knows that such a thing doesn’t exist.

Even a perfectly hedged strategy is subject to volatility.

A legitimate collar strategy is a trade-off: an investor sacrifices significant upside potential to pay for the downside protection. In many market conditions, it would underperform a simple index fund. Madoff’s claimed ability to consistently generate double-digit returns while being fully hedged defied the most fundamental law of finance: there is no reward without risk. His performance was simply too good to be true.

The longer he produced these impossible returns, the more believable they became. Each year of steady gains, especially during market downturns like the 1987 crash or the dot-com bust, became further “proof” of his unique talent.

This created a powerful feedback loop where the fraud’s longevity became its own best defense: if it was a fraud, why could it endure so long?

The Cast of Characters

Below is the list of Madoff’s inner circle and their ultimate fates:

Frank DiPascali

CFO / Director of Options.

He was a key lieutenant, managing the day-to-day fraud, fabricating records, and devising the split-strike conversion narrative. DiPascali pleaded guilty in 2009 and died of lung cancer in 2015 while awaiting sentencing.

Annette Bongiorno

Longtime Secretary. She handled top client accounts, generated fake trading tickets using historical data, and worked for Madoff for 40 years. Bongiorno was convicted and sentenced to 6 years in prison.

David Kugel

Bond Trader. He provided legitimate arbitrage trade data that was falsified for the Ponzi scheme’s fake statements. Kugel pleaded guilty and cooperated with prosecutors.

Daniel Bonventre

Director of Operations. He falsified accounting records to disguise the fraud and make the firm appear profitable. Bonventre was convicted and sentenced to 10 years in prison.

Here’s the list of feeder funds that earned fees from simply funneling money to Madoff. These funds had no incentives to do any rigorous due diligence, as far as they are concerned, the transaction fees were their golden goose.

J. Ezra Merkin

Money Manager (Ascot Partners). He channeled billions into Madoff’s fund from clients, including charities and universities. Merkin settled lawsuits for hundreds of millions of dollars.

Fairfield Greenwich

Investment Firm. This was the largest feeder fund, channeling over $7.5b to Madoff, often without clients’ knowledge. Fairfield Greenwich faced liquidation and extensive litigation.

Carl Shapiro

Philanthropist / Investor. An early and major investor who, along with his son-in-law Robert Jaffe, funneled huge sums to Madoff. Shapiro returned $625m in a settlement with the trustee.

Madoff’s immediate family members were also involved…

Peter Madoff

Brother / Chief Compliance Officer. He created a sham compliance program and signed off on false regulatory filings. Peter Madoff pleaded guilty to falsifying records and was sentenced to 10 years in prison.

Mark Madoff

Son / Trader. He worked in the legitimate market-making business and reported his father to authorities. Mark Madoff committed suicide on December 11, 2010, the second anniversary of his father’s arrest.

Andrew Madoff

Son / Trader. He also worked in the legitimate market-making business and reported his father to authorities. Andrew Madoff died of lymphoma in 2014.

Ruth Madoff

Wife. She maintained ignorance of the scheme, famously asking, “What’s a Ponzi scheme?” She attempted suicide with his husband on Christmas Eve 2008. She forfeited the majority of her assets, retaining $2.5m.

Regulatory Failures

For over 16 years, the SEC received numerous credible, detailed, and substantive warnings about Madoff, yet it failed to take the most basic investigative steps that would have uncovered the fraud.

Avellino & Bienes (1992)

The SEC’s first and perhaps most consequential failure occurred in 1992. The agency launched an investigation into Avellino & Bienes (A&B), an accounting firm that was effectively an exclusive feeder fund for Madoff. The SEC found that A&B was selling unregistered securities and noted their “curiously steady” high returns, even suspecting they were operating a Ponzi scheme. The investigation revealed that all of the firm’s client funds were invested with a single, unnamed manager: Bernie Madoff.

The SEC forced A&B to shut down and return all money to its investors. This triggered a panic within Madoff’s office.

Madoff had his team fabricate three years of financial records overnight to match the books A&B had on file. He then borrowed money against a client’s stock to secure a loan to cover the hundreds of millions in redemptions. Miraculously, every A&B investor was paid out in full.

The SEC’s catastrophic error was its failure to investigate Madoff himself. Despite knowing he was the sole manager of a suspected Ponzi scheme, the agency never examined his operations.

Instead of exposing him, this event massively enhanced Madoff’s reputation! A Wall Street Journal article hailed him as the savior who had protected investors, and his profile soared.

This moment was pivotal. It taught Madoff that the SEC could be beaten and that his reputation was a nearly impenetrable shield, emboldening him to expand the fraud.

Whistleblower Markopolos

Beginning in May 2000, Harry Markopolos began a relentless, 9-year campaign to expose Madoff. He made multiple detailed submissions to the SEC, each more urgent than the last.

His 2005 submission, a 21-page memo titled “The World’s Largest Hedge Fund is a Fraud” was a masterclass in forensic financial analysis.

It laid out nearly 30 clear red flags, methodically proving that Madoff’s claimed returns were mathematically impossible.

The SEC conducted several examinations of Madoff’s firm between 2004 and 2007. Yet they were easily fooled every time. The single most critical failure, highlighted in the post-mortem report by the SEC’s own Inspector General, was that the agency’s staff never took the simple, standard step of verifying Madoff’s assets and trades with an independent third party.

Madoff claimed he was clearing trades through European counterparties, but the SEC only ever asked Madoff himself for proof, which he easily fabricated. They never called the Depository Trust Company (DTC) or the European banks to confirm the existence of the billions in assets Madoff claimed to hold.

This failure was due to reputation capture. Madoff was a Wall Street legend who had helped the SEC design modern trading systems. The junior examiners sent to investigate him were psychologically and professionally outmatched. This institutional fear of challenging a powerful figure allowed the greatest financial fraud in history to continue unchecked for nearly another decade.

The Silver Bullet

The autumn of 2008 saw the global financial system unravel. The collapse of Lehman Brothers and the near-failure of AIG triggered a worldwide panic. As legitimate investments cratered, Madoff’s clients, who had long viewed their accounts as their safest and most liquid assets, began requesting redemptions.

This was the “silver bullet” to put any Ponzi to death.

What began as a trickle of withdrawals soon became a flood. Panicked investors, needing cash to cover losses elsewhere, tried to pull their money out all at once. By the end of the year, investors had requested redemptions totaling an astonishing $7b.

Madoff had only about $300m left in the Chase bank account. He frantically sought a new infusion of cash from wealthy investors but nobody was interested.

The game was over.

On December 3, 2008, he pulled his trusted lieutenant, Frank DiPascali, aside and admitted the truth.

A week later, on December 10, Madoff held the firm’s annual Christmas party, handing out bonuses early in an attempt to use up the remaining cash.

That evening, his sons, Mark and Andrew, who worked in the legitimate trading arm of the firm and had grown increasingly concerned and confronted him about the unusual payments.

Madoff took them into their Manhattan penthouse and revealed the truth.

Confession and Arrest

The sons were devastated. They immediately cut ties with their father, left the apartment, and contacted a lawyer.

The next morning, their attorney alerted federal authorities. On December 11, 2008, two FBI agents arrived at Madoff’s home.

When they confronted him with the accusation and asked if there was an innocent explanation, Madoff calmly confessed.

He was arrested on the spot.

Madoff’s confession was not a moment of moral collapse but a final, calculated act of control. Knowing the scheme was doomed and his arrest was imminent, he chose to end it on his own terms. By confessing first to his sons and then immediately to the FBI while insisting he acted alone.

He controlled the initial narrative, attempting to position himself as the sole perpetrator to shield his family and loyal employees from prosecution. It was the final move of a man who, having lost the game, was determined to dictate how the board was cleared.

Human Toll

The scope of the devastation was immense. The headline figure of $65b represented the fabricated paper wealth on clients’ final statements; the actual cash losses were estimated to be between $18b and $20b.

Thousands of victims, ranging from celebrities like Kevin Bacon and Holocaust survivor Elie Wiesel to ordinary retirees, teachers, and small family foundations, lost their life savings overnight.

The human impact was profound and tragic.

Respected financiers like Thierry de la Villehuchet killed himself in his 22nd-floor office by sleeping pills and slit his left wrist. He was the first casualty.

Retired British army officer William Foxton shot himself in the head after losing his family’s fortunes.

Charitable organizations, such as the JEHT Foundation, were forced to close their doors, abruptly ending their work on social justice issues.

The tragedy extended deep into Madoff’s own family and friends. Publicly shamed and facing a barrage of lawsuits and death threats, the family disintegrated.

On the second anniversary of his father’s arrest, Mark Madoff hung himself in his New York apartment. Following the death threats, his wife asked a court to change her surname for protection.

His younger son, Andrew Madoff, who blamed the stress of the scandal for the return of his cancer, died of lymphoma in 2014.

A friend and associate, Jeffry Picower, was also sued and was found dead in a swimming pool at his Florida home.

The mastermind, Bernard Madoff, pleaded guilty to 11 federal felonies, including securities fraud, mail fraud, wire fraud, and perjury. On June 29, 2009, he was sentenced to the maximum term of 150 years in federal prison, where he died in April 2021.

He was cremated, and his ashes remained unclaimed by his family.