HEI: Heico

History

Heico (HEI) was founded in 1957 as Heinicke Instruments Company, but the story really begins in the late 1980s, when one of Larry Mendelson’s kids stumbled upon it.

Laurans “Larry” Mendelson was a New Yorker who, while attending Columbia Business School a decade after Buffett, took the same security analysis course Buffett had. After graduation, Mendelson moved to Florida and made a lot of money in real estate, but he put his value-investing skills to work in the stock market as well. In the 1980s, his sons Eric and Victor attended Columbia as undergraduates; while they were there, Larry asked them to look for undervalued securities in their spare time. Interest rates were falling, stocks were modestly priced, and Larry was looking for a business he and his sons could take over and run.

In keeping with Ben Graham’s tradition, the Mendelsons didn’t particularly care what the business did. It just needed to be cheap, poorly managed, and located in Florida, where the family wanted to stay.

One day, while doing research in the Columbia law school library, Victor found HEICO, which appeared to meet the family’s criteria. The company specialized in making medical-laboratory equipment, but it had made a series of acquisitions, including one in the aerospace business. By the time Victor found HEICO, it had been public for nearly thirty years but barely made any money.

The Mendelsons saw HEICO as a company whose shares they could buy in the open market and then agitate for change.

HEICO’s appeal lay not in the liquidation value of its assets, but in the latent earnings potential of its aerospace subsidiary.

Several years before, an engine on a Boeing 737 had caught fire during takeoff in Manchester, England. 55 people died, and authorities later determined that a malfunction in one of the engine’s combustion chambers caused the fire. Regulators ordered airlines around the world to replace these combustors at regular intervals immediately.

When the component’s manufacturer, Pratt & Whitney, couldn’t meet the surge in demand, half of the world’s 737s were grounded.

Because HEICO had been authorized by the Federal Aviation Administration (FAA) to make a generic version of this combustor, business was good when the Mendelsons discovered it. What intrigued them, however, was not the one-off combustor demand but the idea of using HEICO as a platform to produce thousands of generic spare parts for the airlines.

Current management was doing nothing to exploit the opportunity. Unlike the auto industry, in which generic components can be sold without any regulatory approval, every airline part must be blessed by the FAA and similar international bodies.

If the FAA had approved the generic manufacture of a critical jet engine part, why wouldn’t it approve other less critical parts? And if HEICO secured such approval, wouldn’t the airlines be interested in an alternative source for spares?

Original Equipment Manufacturers (OEMs) like Pratt & Whitney and General Electric enjoyed monopolistic positions in almost all their replacement parts. Rather than innovate their way to increased profitability, GE and the rest raised prices far above the rate of inflation and, lacking an alternative, the airlines had no choice but to pay.

As they learned more about airline spare parts, the Mendelsons discovered that HEICO could produce and sell generics at a 30% to 40% discount and still make healthy profits and returns on capital. The Mendelsons also found that there were few patents or intellectual-property rights attached to aerospace replacement parts.

In 1989, the Mendelsons and their allies bought 15% of HEICO’s stock in the open market. After a proxy fight, they secured four seats on the board and named Larry Mendelson the new CEO. He immediately sold HEICO’s lab business and focused on the market for airplane spares.

The early years were hard. It was clear that HEICO had a low-cost advantage over branded manufacturers, and in theory the FAA and the airlines loved a cheaper alternative. However, in practice from the perspective of an FAA bureaucrat, they don’t have incentives to approve a part that could risk a plane failure. The perspective of an airline purchasing manager was the same. As a result, for nearly a decade, only a few non-critical parts were approved for manufacture each year.

But the Mendelsons didn’t lose conviction in their initial thesis for HEICO. Realizing that the perception of safety was the main obstacle, they focused on producing parts of the highest quality, and in 1997, Lufthansa vindicated their conviction when it bought a 20% stake in HEICO’s spare-parts subsidiary. As part of the deal, Lufthansa began to order generics in bulk.

Business got a lot easier for HEICO after that. Lufthansa ended up investing in HEICO’s Parts Manufacturer Approval (PMA) business acquiring 20% of it, which is a stake they actually still hold. This massively accelerated PMA development but it also gave HEICO an unique information advantage where they were able to use Lufthansa’s technical data and Lufthansa could pick out the highest volume, highest value parts for them to PMA.

HEICO could sell parts to Lufthansa and other airlines immediately after approval. This launched HEICO into being the leader in the space. They now have a portfolio of 19,500 parts and have also built out the largest non-OEM repair and overhaul network as well as acquired about 50 other electronic technologies business that make up that segment. To round it up, since the Mendelsons took over HEICO in 1990, sales have compounded annually at 15%, net income at 18%, and that’s driven a 21% annual stock price return.

Today, HEICO is still family run with father Larry (age 86) as CEO and Chairman, sons Eric (59) and Victor (52) run the 2 business segments Flight Support Group and Electronic Technologies Group respectively.

Market Characteristics

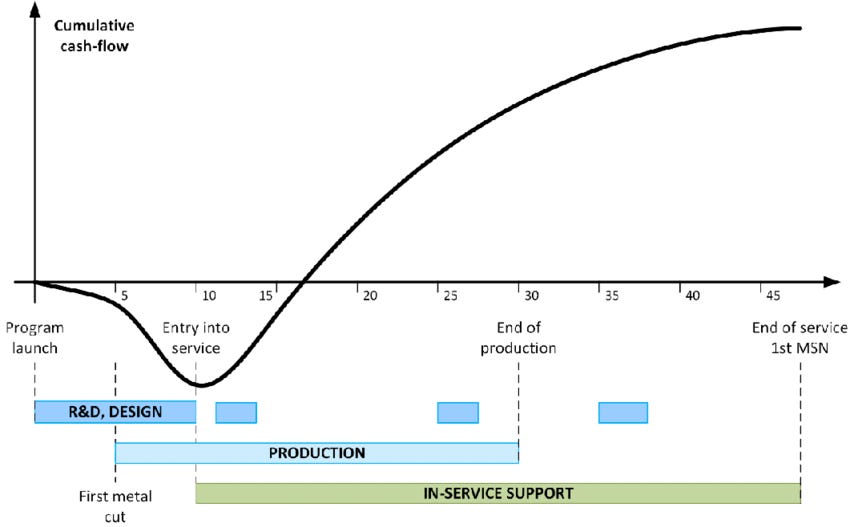

Extremely Long Product Cycles

The average life of an aircraft is about 25 to 30 years plus the product run of 10 to 20 years. The parts and maintenance cycle is at least 35 years long. This features predictable revenues, with the only declines during these major events: 9/11 (2001), GFC (2009), COVID (2020).

The above lifecycle chart shows that the initial few years produces low margin profiles because of the upfront R&D cost. The money is made is the aftermarket since the products last so long and it is complusory to maintain parts, this is where manufacturers make their margins.

HEICO provides a cheaper alternative in this highly profitable aftermarket. They have a cost advantage because, unlike OEMs, HEICO does not incur those heavy R&D cost.

Highly Regulated

The only way a company can sell a replacement part to an airline is if it’s approved by FAA.

The process is highly technical and robust to test for quality and safety features. It also takes substantial time to get approval, justify the demand, carry out tests… to finally bring to market, on average it takes 9 to 12 months to get added into PMA list.

This proves to be advantageous for HEICO, who finds itself behind a regulatory curtain. But this will be a daunting task for new entrants.

Consistent Growth Drivers

There are 2 markets: OEM and aftermarket parts and services. The OEM is dominated by the global duopoly of Boeing and Airbus manufacturing new airplanes. The aftermarket is fragmented with players selling to airlines maintenance.

Typically aftermarket players get into the market by initially having an OEM part sold to Boeing/Airbus. So underneath the OEMs there are actually many suppliers providing the components; OEMs don’t design and manufacture much of these components.

Revenues are driven by predictable recurring maintenance spend because parts have to be replaced on a repeatable cycle based on time and utilisation.

On the boarder demand equation, revenue passenger miles has been trending up for the last 20 years at a CAGR of ~3%. This is highly correlated to GDP and we don’t expect the correlation to break.

Total addressable market for commercial aircraft PMA is estimated at $11.3b. On revenues basis, HEICO has less than 10% share.

Coexistence with OEMs

When HEICO competes with OEMs the goal is not to exceed 30% of market share. The rationale is if HEICO takes too much market share, they will incentivize OEMs to cut prices, and when they cut prices then the incentives for airlines to PMA is diminished.

HEICO also don’t manufacture life-limited parts which are parts that have to be replaced after a certain amount of flight cycles. These are usually the most highly engineered, most safety critical and highest margins parts for the OEMs.

The dynamics are such that HEICO is trying to incentivize behaviour where both parties can coexist.

Operating Lessors

One sector of the industry that has remained resistant to PMA parts is operating lessors, most of which stipulate the use of OEM parts in the return conditions in their lease contracts, partly because PMA parts reduce the value of the aircraft and engines concerned. Some low-cost airlines avoid using PMA parts simply because they have their aircraft on short-term leases with operating lessors.

Crown Jewel: HEICO’s PMA Business

To produce a PMA part, HEICO takes an OEM part and reverse engineer it, without the high upfront R&D costs, then they go through a robust certification process with FAA. This is in fact more robust than the OEM process because OEMs are certified on an overall basis, not part-by-part basis.

The parts HEICO produces tend to focus on less safety critical components, making it easier to maintain quality, get approval and sell to airlines.

Finally the airlines themselves have to approve of that part. So there are multiple levels of qualification process before a part ends up into the airplane, this creates a significant barrier to entry because suppliers can only run so fast in terms of new parts developments.

Competition: PMA vs OEM

Cost Savings

Cost is a major value proposition in the airlines ecosystem. HEICO does not incur the R&D costs as the OEMs and therefore can sell parts at a 30% to 40% discount. Due to OEMs having a duopoly structure, it is not uncommon for OEMs to raise prices every year above the inflation rate.

So when HEICO sells at initial discount, they could raise prices and yet still be cheaper than OEMs in the future simply due to the lower starting price. This incentivizes longer term relationships between HEICO and airlines.

Secondary Supply Source

Another benefit of PMA is to act as a second source when there are supply chain disruptions. HEICO tends to do well in rough industry environments because those are the period where airlines are seeking lower costs.

Quality & Reputation

PMA parts are also of higher quality than OEMs because the whole OEM equipment have a long product cycle, so those parts within the larger equipment tend not to be improved very much over the life cycle. So many years later, when the part is PMA, it is manufactured with better materials. HEICO sold over 80 million parts and had zero service issues issued, zero air-worthiness directives and zero inflight shutdowns due to their parts. This is not a quality assurance than an OEM can claim to have.

However, there is also an argument that airlines are not always worried about price. Nobody gets fired for buying an OEM part, but when they start looking at PMA parts, it adds friction to the sales process and adds a bit more risk.

Competition: PMA vs PMA

There are about 2,300 PMA players in the US; it’s a highly fragmented marketplace.

HEICO is by far the largest in the PMA space with over 14,000 parts and producing 500 new parts every year. It acquired the second largest competitor, Wencor, in 2023 for $2.05b ($1.9b cash + $150m stock) with a portfolio of ~7,000 parts, giving the combined entity ~21,000 parts.

However, there are no intellectual proprietary rights to shield HEICO from competition. HEICO differentiates by providing integrated solutions instead of just selling commoditized parts. For example, HEICO gives their clients access to inventories and manpower (engineers to fix/replace parts).

New entry to the PMA space is very difficult due to both regulatory barriers and time taken to bring products into the market. Even with HEICO having long relationships with FAA and airlines, they can only produce ~500 new parts each year.

Another competitive advantage is the knowledge required to reverse engineer parts in an efficient manner. It is not a simple engineering process to manufacture airplane parts.

Business Segments

Flight Support Group (FSG)

60% revenues, ~20% op margins. Run by Eric Mendelson.

The PMA business lies in here.

FSG uses technology to design and manufacture jet engine and aircraft component replacement parts. They make FAA-approved replacement parts for jet engines that can be substituted for original parts, including air foils, bearings, and fuel pump gears.

FSG repairs, overhauls and distributes jet engine and aircraft components, avionics and instruments for domestic and foreign commercial air carriers and aircraft repair companies, as well as military and business aircraft operators.

Electronic Technologies Group (ETG)

40% revenues, ~26% op margins. Run by Victor Mendelson.

ETG designs, manufactures and sells various types of electronic, data and microwave, and electro-optical products, including infrared simulation and test equipment, laser rangefinder receivers and electrical power supplies.

This portfolio is heavily diversified with over 100,000 SKUs, each are mission-critical technology which cost a fraction of the much larger system they serve. We could think of these products as analog semiconductors (transmitting data with waves instead of digital) but with less cyclical and growth.

It comprises of about 50 acquired businesses and sell things like antennas, RF (radio-frequency) switches, microwave power modules etc. Fun fact: NASA’s Mars Rover has 4 different HEICO subsidiaries in ETG supplying flight hardware (Apex Microtechnology, Sierra Microwave Technology, 3D PLUS and VPT).

Components in ETG are highly engineered that go within systems of fighter jets and weapon systems as well as medical devices.

A first glance would tell us that these segments look very different. And while the businesses are very unique, there is some complementary attributes. ETG has some manufacturing capabilities in low-cost solutions that FSG is able to leverage. So HEICO ends up having crossovers of different suppliers.

Although they’re never vertically integrated, the segment presidents are often incentivized and encouraged to work together and able to use the resources from both to complement each other.

Another reason why ETG makes sense is that it produces a lot of steady cash flow and that allows for a capital allocation in terms of acquisitions.

The biggest piece of ETG is defence. It is dependent on government budget, which tends to be non-cyclical because defence spending is more driven by the global threat environment than the economic cycle. Operating margins are above 20% due to the price inelasticity of customers.

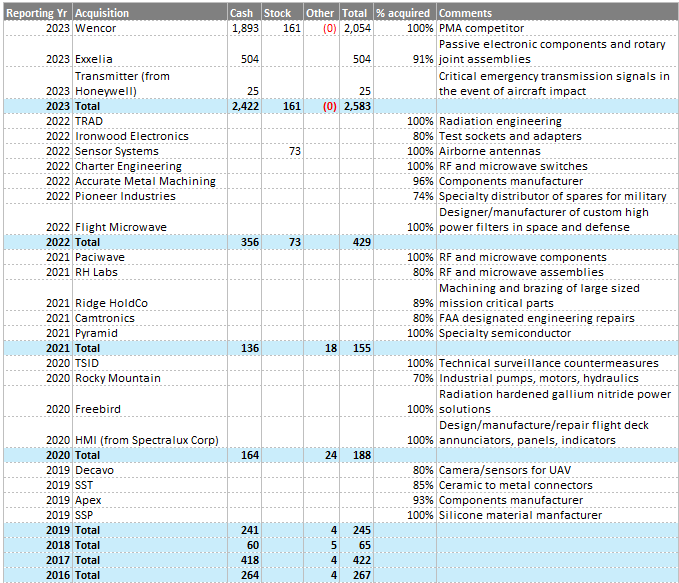

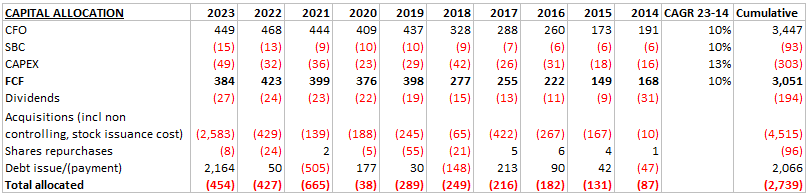

Acquisitions

Since the Mendelsons took over, they have done ~98 acquisitions and only divested 2. They deployed ~$5b for M&A over 34 years with less than $10m cumulative impairment cost. That is quite amazing on the discipline to not overpay.

List of acquisitions:

The list is quite long and HEICO does not provide most details in terms of cash paid. Below is a summarized table:

We find it difficult to assess the multiples that management paid for these acquisitions due to the lack of information. We can prehaps look to the ROIC at entity level of ~10% and conclude that HEICO is at least reinvesting capital at this rate.

Insiders Ownership & Incentives

The Mendelsons own ~8% of shareholders equity. The rest of the Board owns ~2.5%. But most importantly, the employees own ~2% of the company. Since 1985, HEICO gifts stock in the 401(k) plan as a percentage of compensation per year (it was 6% in 2023: 10K, pg 107).

As of 2023, there are 7,900 current and former employees taking part in this matching plan (their long-serving secretary is a millionaire because of this).

There are over 400 employees at HEICO that have over $1m of HEICO stock in their 401(k). On average, HEICO employees own more in stock than they make in annual compensation.

Incentives are paid out with reference to adjusted net income, EBITDA and operating cashflows.

In 2006, the Board approved the Leadership Compensation Plan (LCP), which is a deferred compensation plan. The LCP is currently available to approximately 570 employees and to the Board members. Participating employees may contribute a portion of their compensation to the LCP and HEICO will match salary contributions at a specified fraction of each employee’s salary contribution.

In addition, the Committee and Board of Directors retained discretion to contribute additional amounts to each participant’s account in the LCP. In 2023, they made contributions to some executives in an effort to “catch up” for retirement benefits not paid to them prior to 2007.

Comparison with Transdigm

Both companies have similar exposures from a defense and aftermarket perspective. They generate most of their profits through parts and are run by talented management teams.

Both have a decentralized M&A program as core to their capital allocation, and both try to align an ownership mentality within the culture.

But their strategies are opposite in a lot of ways.

HEICO tends to leave acquired subsidiaries alone, while TransDigm has been very willing to go in and cut costs and divest pieces and they are very effective in doing that.

HEICO employs low levels of leverage debt to EBITDA of 2.8x, while TransDigm runs at 6x.

HEICO’s entire value proposition tends to rely on operating customer savings, TransDigm is known for raising prices. But the good news is they really don’t compete as much as most people think and a lot of ways end up working together.

Why they don’t compete?

TransDigm has over 300,000 parts while HEICO has 21,000. There is a 14x differential in total number of parts.

However, revenues of TransDigm’s aftermarket parts business are $2.2b (2023 10K, F-39). HEICO has $1b, which means the unit price of TransDigm products are much lower than HEICO.

TransDigm will often take for some of their more high-value parts and go have a PMA company be their distributor. Wencor actually is the main distributor for a few of TransDigm’s key product lines. Now that Wencor is acquired by HEICO, the situation is more advantageous for HEICO.

Financial Model

Free cashflow tends to convert at more than 100% of net income due to mismatch of amortization expense and the low levels of CAPEX. Amortization is high because of acquisitions, but that doesn’t require cash to replace the assets.

Dual class shares structure: Class A shares have 1/10 vote, non-Class A has 1 vote.

Risk #1: More Acquisitions?

Can HEICO continue investing cashflows for acquisitions of larger size? The Wencor deal for $2b is probably the largest deal that fits HEICO’s business model.

We think that there is plenty of room to do a lot of smaller deals because the supply chain is just so fragmented and so diverse. But we also think it will trend towards ETG segment rather than FSG.

Risk #2: PMA Parts Failure

The biggest risk is that a part failure causes a plane crash. Although they have a long track record of quality, we cannot rule out this risk

Risk #3: OEMs Retaliation

HEICO has grown to be a very significant player and they are able to offer a lot more system-level customer saving solutions.

So we think there is a risk going forward that OEMs start fighting back. OEMs have advantages of long-term service agreements with warranties. They are also not shy for doing anti-competitive activities in the past.

Valuation

HEICO is well known and it’s quite expensive in relation to cashflows and earnings. We are not sure if there is anything we can add here other than a DCF?

Conclusion

After some research, the PMA space is admittedly still a black box to us. For example, we don’t know what drives airlines to select which PMA manufacturer. Is it simply due to price, reliability and availability? How high is the engineering knowledge barrier such that other companies fall behind HEICO?

On acquisitions, other than Wencor, there isn’t enough information for us to measure the price HEICO paid. As a generalist, the industry specifics also prevented us from truly understanding the economics of the business.