GOOGL: Alphabet (1)

Preface

We currently have a position on GOOGL, it was bought at a cost basis of $50/share and added more during the COVID crash. In Q1 2024, we mostly took profit at $140/share and reinvested into WRB. Now it represents only 2.6% of the fund with the remaining cost basis of $68/share.

Usually we would write about the business before buying, but GOOGL was numerically cheap back then. As we continued to learn more about the business model, we feel that we can write something meaningful.

We skip its history and dive straight into the business economics.

Value Proposition

We think that there are 2 fundamental value proposition that GOOGL provides:

Information Discovery

Tech Infrastructure

Information Discovery

During the 1990s, the world saw the invention of internet search engines. They provided faster, more accurate and more adaptable way to access information on the internet. However, GOOGL was not the first one. Early players like Archie (created by students at McGill University in 1990) and WebCrawler in 1994 laid the foundations of search but lacked efficient indexing capabilities. Yahoo, also launched in 1994, worked initially as a directory of websites categorized by humans.

GOOGL was late to the scene but introduced an important innovation called PageRank. Unlike competitors that ranked pages by clicks, PageRank prioritised relevance through citations and delivered superior results.

Fast forward to today, GOOGL commands ~90% of global search market, but search dominance does not automatically imply information discovery dominance, which is the current challenge that GOOGL faces.

The information discovery value proposition is challenged on 3 fronts:

Social Media: Platforms like Facebook, Instagram and Tiktok are preferred for product discovery, providing recommendations from real people.

E-commerce: Amazon and Walmart provide more specific results for consumers with buying intent.

Artifical Intelligence: AI chatbots can summarize and extract key insights for complex queries with human language interaction.

Of course, GOOGL is also a fierce competitor with products that enhance their search ecosystem. For example, Gmail, Google Translate, Google Meet and Google Maps are features that widen the information discovery moat.

Particularly, Google Maps has become a very important segment of the business with Apple Maps being the main competitor. In Q3 2024 earnings call, CEO Sundar Pichai mentioned that Google Maps surpassed 2 billion monthly users, although they don’t disclose revenue numbers but it was estimated that in 2023 it generated $11b revenues. The growth is superb, compared to only $3b in 2019.

These platforms enhance the ecosystem by having two-sided network effects. As more people use the platforms, it attracts more suppliers willing to pay for advertisements, which in turn attracts more users. The loop reinforces itself.

On the smartphone front, GOOGL acquired the Android operating system (OS) as a defensive measure to protect its search business, along with an attempt to take some hardware market share with Pixel smartphones. By pre-loading Google platforms on these devices, it encourages their existing user base to stay in the ecosystem.

It won’t be a stretch to think that GOOGL will integrate AI into all these platforms as well. The integrated services across its portfolio of products serve consumers with efficient information discovery, and this value proposition is unlikely to be eroded given the huge talent pool GOOGL attracts to improve its products.

Another area of information discovery can be attributed to how consumers seek entertainment today. Every Big Tech player has a hand in the entertainment market given that time spent on leisure has increased over the past 50 years. The more important change is the level of interaction with entertainment mediums which leads to monetisation like subscriptions, direct purchases and advertising revenues.

Companies have 2 roles to play in entertainment: content creation (game developers, music labels, film) or distributors (Netflix, Instagram). The “content creation” role is weaker because it’s subject to cycles and limited shelf life; the marginal utility of watching a movie diminishes over time, resulting in the need to continuously create new content. Barriers to entry are also low with today’s technology. This can be seen at Sony, who realised this and switched from solely owning exclusive content to licensing its content to third parties, effectively becoming a distributor of content.

On the other hand, distributors extract the most economic value as they control the platforms which media is delivered to consumers.

GOOGL owns YouTube and Android OS app store which gives huge economic advantages on the distributor role.

On the importance of distributors & platforms, Eric Schmidt in his book “How Google Works” wrote:

First, the Internet has made information free, copious, and ubiquitous; practically everything is online.

Second, mobile devices and networks have made global reach and continuous connectivity widely available.

And third, cloud computing has put practically infinite computing power and storage and a host of sophisticated tools and applications at everyone’s disposal, on an inexpensive, pay-as-you-go basis.

Before the Android OS, Apple had launched the iPhone in 2007 with a far superior computing and user interface than anything available in the market. There was an opportunity for a second player as Apple had opted for a closed system. Then one year later in 2008, GOOGL open-sourced its Android software and partnered with existing smartphone manufacturers like Nokia, Motorola and Samsung.

The beauty of owning the OS is a near 100% gross margin, combine this with 71% of global market share (it was 2.4% in 2009!) and we see Google Play earning $51b revenues in 2024 (14.5% of total revenues).

YouTube (YT) is yet another miracle. Initially acquired in 2006 for $1.65b it reported $36.1b of revenues in 2024, more than 21x the purchase price! Other than Facebook and Instagram, we don’t think there is another more integrated ecosystem than YT for content creators. GOOGL isn’t afraid to cannibalise on YT ads revenue by diversifying into subscription fees. Out of the $36.1b revenues, we estimate about 45% to 50% come from subscriptions which are nearly 100% margins, this move is definitely better than full ads model where GOOGL pays content creators 55% margins.

Tech Infrastructure

Tech companies have historically monetised the by-product of computing power in different ways. For example, IBM realised that it could provide consulting services alongside its core business. However, this type of monetisation is not scalable, because consulting revenues depend on how many consultants are hired.

To avoid this problem, Big Tech have turned to more scalable and profitable ways to monetise, giving rise to the cloud compute market. GOOGL competes using Google Cloud Platform (GCP) against formidable players like Microsoft (Azure) and Amazon (AWS).

The benefits of cloud compute for businesses is very important. For example, think about the many businesses which need to track and monitor delivery fleets and inventory levels; or financial companies which need virtual machines to collaborate on a global scale.

Governments also rely on cloud compute to support their operations due to the large amounts of data. For example, the UK tax authorities shifted to AWS while saving 50% costs.

Big Tech players have the compute power and resources to provide these services at an attractive margin. In 2024, AWS had operating margins of 38%, the highest since 2014, Azure reports 47%, while GCP has 14%. Although GCP has the lowest margins, it just only recently turned profitable in 2023.

On April 2008, GOOGL entered the cloud market after realising their internal data processing needs could be extended to other businesses. Microsoft also noticed the shift in the software market from traditional on-premise to cloud and launched Azure in the same year.

The cloud business is characterised by first-mover advantage, because there are significant cost involved when switching cloud providers and such decisions impact company-wide operations. The 2 competitors are very strong; AWS had a 2 year head start and provides excellent service and bandwidth. Azure has competitive advantages from system integration with their suite of productivity tools (MS Office).

GOOGL being the last among them has found advantages in AI and machine learning with TensorFlow and Vertex AI as key selling points. This is likely due to GOOGL being an early pioneer in machine learning, especially in areas like search algorithms and natural language processing.

There are structural reasons why the cloud market can have multiple profitable leaders. First, it is common for large companies to have 2 or more cloud providers for security and risk management reasons.

Second, regulatory concerns on the concentration risk to any one public cloud provider is flagged as an issue for financially systemic important institutions.

Third, some companies will opt to have alternative cloud providers to reduce reliance on Amazon as a direct competitor. For example, Home Depot, Target and eBay are some of the big retail players that have chosen GCP instead.

Unit Economics

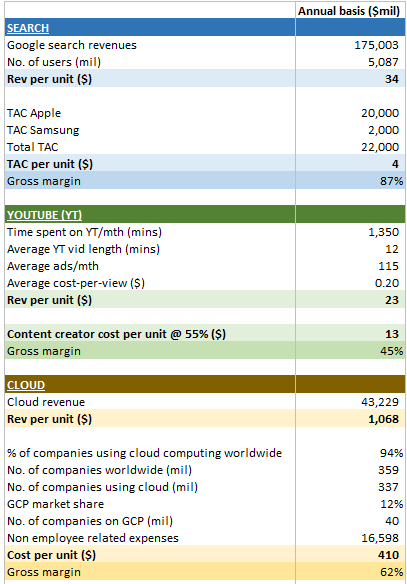

GOOGL does not provide gross margin profiles for Search, YT and Cloud segments. We attempt a bottom-up approach to estimate and verify the common belief that Search fetches the highest gross margins followed by Cloud and YT.

Search

There are an estimated 5.6 billion internet users of which Google Search has 91.5% market share, take the reported Search revenues and find the revenue per unit = $34.

Traffic Acquisition Cost (TAC) are mainly paid to Apple and Samsung with reports suggesting $20b and $2b per year respectively. So TAC per unit = $4. Not surprising, gross margins are high at 87%.

YouTube

We estimate the average person spends 45 mins per day (1,350 mins/month) on YT and the average length of a video is 12 mins. So per month, users see on average 115 ads, with each ad having cost-per-view of $0.2. Then, revenue per unit = $23.

We know that GOOGL pays content creators 55%, implying gross margins of 45%.

Cloud (GCP)

The number of companies worldwide is estimated at 359 million, 94% of them are using some form of cloud service.

GCP has 12% market share, meaning ~40 million businesses use it. From the 10K pg. 88, the non-employee related cloud expenses is $16.6b, so cost per unit = $410.

Revenue per unit = $1,068 (reported cloud revenues of $43.2b divided by 40 million business), so gross margins is 62%. To sense check, Google’s pricing calculator estimates $1,174 for 5 instances of compute and 6,000GB of storage.

The Reason for Estimation

The implication of this exercise shows:

1. Search and Cloud are the most important segments of GOOGL. Estimating future cashflows should weigh heavily on the assessment of these segments.

2. Gross margins in Search are very lucrative, and they have almost zero marginal cost to onboard another advertiser or end user. They have a replicable blueprint which essentially is copy & paste code. GOOGL is beholden to Apple & Samsung as they pay to be the default search engine. This relationship presents an investment risk.

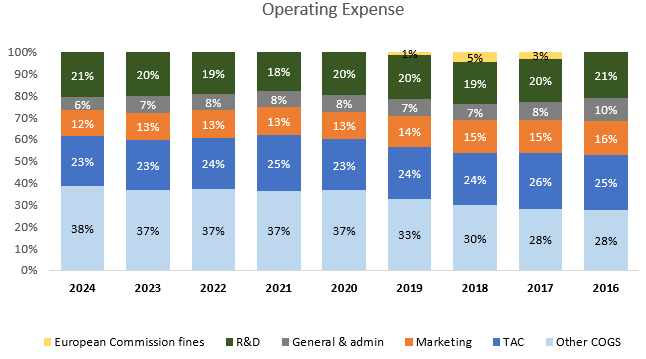

3. Operating expenses eat up 26% of revenues (overall operating margins of 32% vs. gross margins of 58%). This is a significant amount and we should see the cost breakdown.

Operating Expense Breakdown

The cost trend that is increasing in “Other COGS” contains datacenter depreciation expenses and YT payments to content creators. This is explained by increased AI related CAPEX and YT growing into a larger share of revenues.

GOOGL will likely become a more capital intensive business over time, resulting in higher depreciation charges, whether or not revenues will more than cover these expenses depends on our ability to assess the future of AI monetisation.

Today, GOOGL has datacentres in 25 locations (8 in the US), with a further 13 under development in regions like Malaysia, Mesa (Arizona) and the UK. Some of these locations host multiple datacentres; Singapore hosts 4 data centres, with the most recent data centre opened last year.

Other Bets Segment

GOOGL has a separate non-core segment called “Other Bets” which hosts various projects and startups. These include Calico (biotechnology), CapitalG (growth fund invested in startups from Crowdstrike, Duolingo, Lyft, and Stripe), Google Fiber (fibre optics), Wing (drone delivery), Waymo (self-driving car), X.company (R&D) and Verily (life sciences).

Among these companies, Google Fiber and Verily contribute the most to earnings, while Waymo is valued at $45b. Waymo recently hit 200,000 paid trips per week for its autonomous ride-hailing service.

Industry Comments

Digital Advertising

The digital advertising market is dominated by a few key players: GOOGL, META and Amazon account for 66% of global digital ads revenue. GOOGL holds 37%, followed by META 20%. Although it seems like a strong market position, these players face high competitive pressures.

Many think that META is a main threat to GOOGL, but Amazon actually is a bigger threat. Just as GOOGL has expanded into Amazon’s cloud market, the latter has aggressively scaled their digital advertising. From 2019 to 2024, Amazon ads segment grew revenues faster than Search, YT and META. Even compared to the faster growing YT, over the past 6 years, Amazon ads revenue CAGR at 33% while YT had 22%.

This threat of retail media networks does not just end with Amazon. In fact, Walmart and Target have invested heavily in this segment, allowing advertisers to place ads directly on e-commerce platforms. The advantage is obvious, it’s a very targeted ad placement that offers better returns on marketing spend.

Samsung Relationship

Samsung has been a crucial partner for GOOGL in the Android ecosystem and default search engine agreements. Their partnership dates back to 2009 when Samsung transitioned from Microsoft’s Windows Mobile to Android with the launch of its Galaxy smartphones. Today, Samsung ships ~19% of global smartphones and collects $8b over 4 years to make Google the default search.

Samsung also provide key hardware components for Pixel smartphones.

Apple Relationship

Historically, GOOGL and Apple maintained a strong relationship; GOOGL former CEO, Eric Schmidt, even served on Apple’s board from 2006 to 2009. However, the launch of Android OS placed the two companies in direct competition. There are also anti-competitive regulatory scrutiny on GOOGL payment of $20b annually to Apple for default search.

GOOGL estimated that it could lose 60% to 80% of query volume if Apple replaced its default search engine, translating to revenue loss of $28.2b to $32.7b. The net effect would be losing $8b to $13b of operating income.

Nvidia Relationship

Nvidia is the dominant player in GPU chips technology and it is even more important now given that AI is a parallel compute problem. GOOGL cloud services use Nvidia’s Blackwell chips, which means the availability of these chips is a supply chain concern.

GOOGL has diversified by going directly to TSMC to produce its own AI chips called Tensor Processing Units (TPU).

Pricing Power

GOOGL utilises an auction based pricing model that is influenced by macroeconomic factors such as the general economy, consumer financial health and seasonal flux. This means GOOGL has limited control over pricing.

See below the annual growth rates of the key operational KPI:

Over the past 8 years, the cost-per-click for advertisers decreased by -55%, while the volume of paid clicks increased by an impressive +934%.

Google Network ads on third-party websites has only grown at +12% largely reflecting the shift from desktop websites to smartphones environment. For impressions, the smartphone environment is more valuable to advertisers, which explains cost-per-impression increase of +42%.

All these suggests that GOOGL pricing model is highly sensitive to demand and supply changes. For example, the most significant declines in cost-per-click occurred during periods of rapid growth in paid clicks (2015 – 2020).

For GOOGL to justify higher prices, it has to offer improved products. For example, investments in its Performance Max (a goal-based campaign type that leverages Google’s AI to optimize ad performance across all Google Ads inventory). Such productivity tools for advertisers are some of the ways it can hike prices, although it does come at some investment cost.

Supplier Risks

Clearly, Apple is a crucial distributor of Google’s search engine. This dependency was likely the main reason why GOOGL wants to vertically integrate with products like Android OS, Pixel and Chromebook. But, so far, these investments have not fully offset this supplier risk.

Valuation

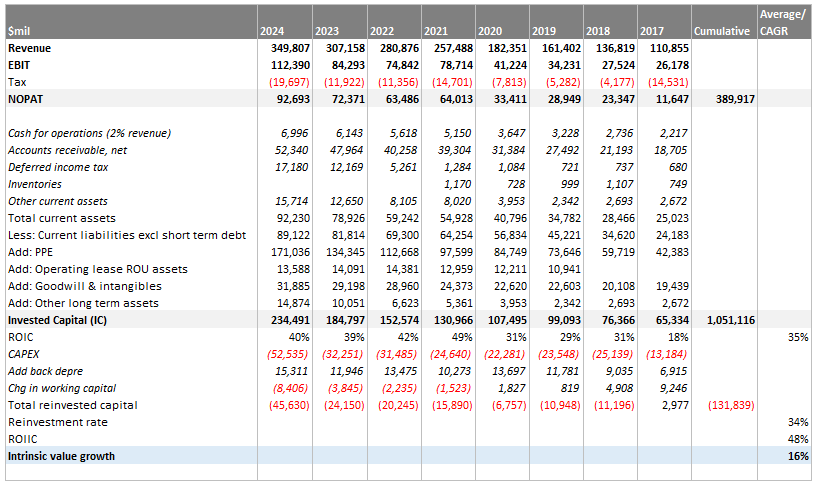

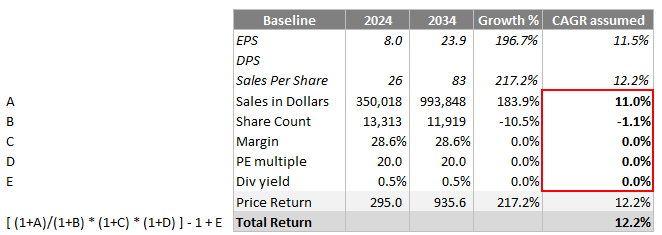

We estimate that GOOGL grew intrinsic value at 16% CAGR for the past 8 years. For context, business performance had CAGR 15% (market cap CAGR 18%, PE ratio -5%, shares outstanding -2%).

Suppose the average ROIC = 35% and our hurdle rate r = 15%, at current PE = 20, what is the implied growth rate (g)?

Let’s do some investing math…

(1) g = RR * ROIC

(2) Distributable cash = (1 – RR) * E

where g = growth rate, RR = reinvestment rate, E = earnings

Intuitively, the company’s growth rate (g) depends on its rate of reinvestment (RR) and the returns it can generate on that investment (ROIC). Equation (1) tells us that high ROIC companies can achieve the same rate of growth as low ROIC companies with a lower reinvestment rate.

Similarly, the earnings a company has leftover to distribute to its owners depends on this rate of reinvestment. Equation (2) tells us that if both companies produce similar earnings (E), then the high ROIC company has more cash leftover for redistribution. This relationship is central to value creation.

Then we can proceed to derive the implied PE in terms of ROIC:

(3) P = D / (r – g) , where r = required rate of return, D = distributable cash

(4) P = (1 – RR) * E / (r – g) … from (2)

(5) P/E = (1 – RR) / (r – g)

(6) P/E = [(1 – (g / ROIC)] / (r – g) … substituting (1)

Rearranging, we get P/E = (ROIC – g) / [(r – g) * ROIC]

Substitute ROIC = 35%, r = 15%, PE = 20. Solve for g = 12%.

How can we rationalize that GOOGL can continue to grow intrinsic value at historical rates well above the implied 12%?

Variables of revenues:

Search: Faces increased competition from social media and e-commerce peers.

Cloud: More growth is likely, boosted by AI investments.

Subscriptions: YT continues to drive growth.

Variables of expenses:

Depreciation: Higher due to CAPEX growth.

Sales & Marketing, SG&A: Likely to maintain same cost/revenue ratios.

Other Bets: Continue to make losses.

Admittedly, we don’t have the expertise to estimate these variables, particularly we don’t know the potential returns on CAPEX. If we breakdown returns by their factors, an implied growth of 12% can be achieved by:

If sales dollars compound at 11% for the next decade and share count decrease by -1.1%, with no changes in margins and PE multiple, total shareholder CAGR will be above 12%. For context, the past 5 years sales had CAGR 14%.

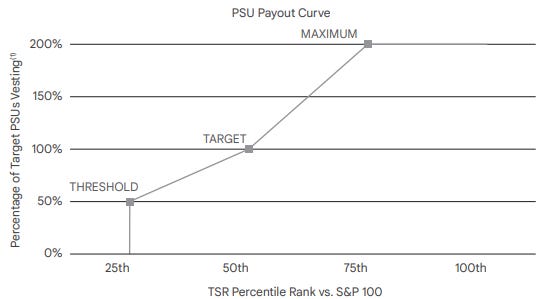

Triple Class Shares Structure

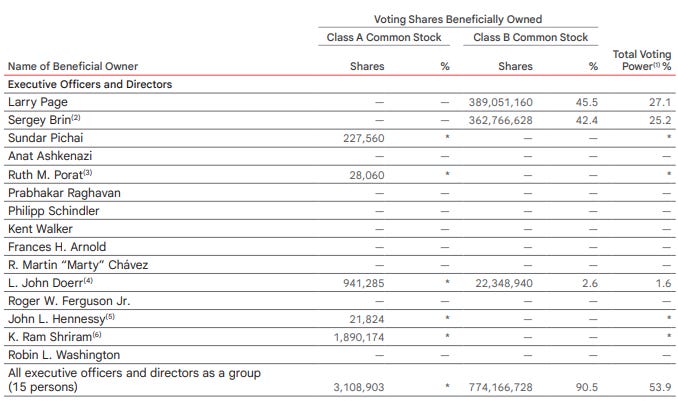

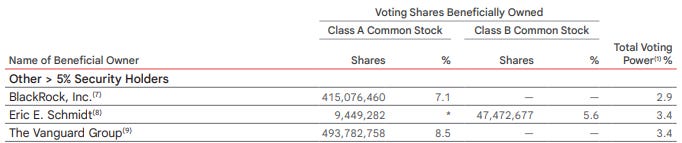

GOOG (Class C) has no voting rights, while GOOGL (Class A) has 1 vote per share. There’s a third Class B category held by insiders (John Doerr, Eric Schmidt) and founders (Larry and Sergey), these shares have 10 votes per share and are not publicly traded. Class B shareholders collectively have 57.3% voting power:

Incentives

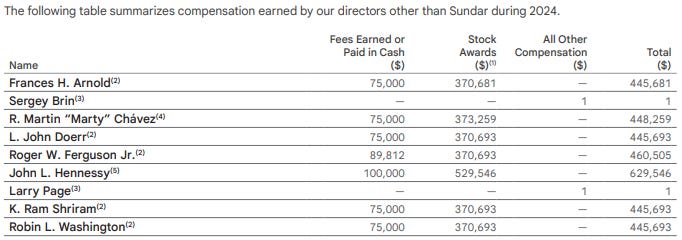

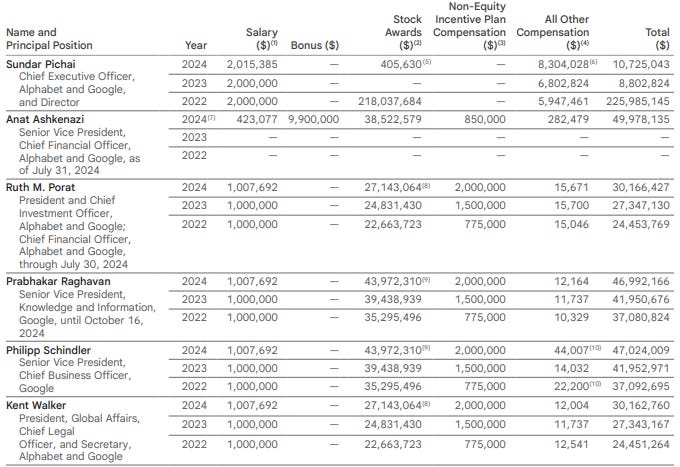

Founders Larry and Sergey sit on the Board of Directors and get only symbolic $1 pay. The other directors are rewarded in cash and much more in stock:

CEO Sundar Pichai has annual salary of $2m, this has not increased since 2020. Although this salary is a small amount, the stock based compensation (SBC) is huge. Here’s the payout for the executive team:

These are the elements that determine SBC:

Total shareholders returns relative to S&P100 companies.

Alphabet’s overall business performance, and the scope of role, impact, and performance of each recipient.

Each recipient’s outstanding and unvested equity awards, and the vesting schedules of those awards.

The result depends on the position on their payout curve: