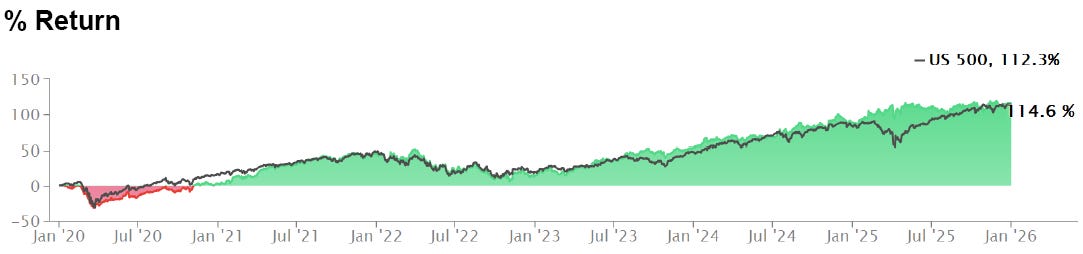

Fund Performance: FY2025

Returns (net of fees)

Inception date: End of December 2019.

Money weighted returns:

Time weighted returns:

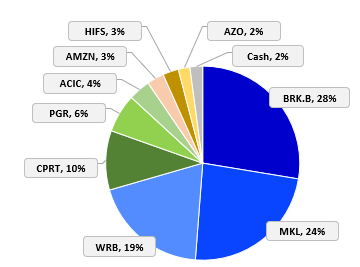

Allocation

For more info: Search [Business Analysis] category. We write about all our positions.

Berkshire Hathaway (BRK.B)

BRK has been and remains as our largest position. The economics of BRK is very diversified and the benefits of profitable insurance float effectively allows BRK to own more assets than their regulatory capital allows.

As of end 2025, Warren Buffett officially retired as CEO. Greg Abel will obviously bring his own ideas to the job and we have already started to see some changes from a structural standpoint, but we expect it to remain business as usual.

We have written about the main challenges that Greg will face.

We think BRK has a greater chance of survival for the next century than any other company that we can understand.

Markel (MKL)

MKL operates in the P&C insurance market and have greatly improved financial reporting this year. We have said that MKL was undervalued for a long time and have continually added shares.

The corporate strategy is wonderful:

Underwrite profitably.

Reserves should be more redundant than deficient.

Invest the insurance float into public equities and diversify by wholly owning non-insurance private businesses.

Run them in a decentralized manner, collect free cashflows and centralize capital allocation at headquarters.

Basically, it’s the Berkshire playbook done at a smaller scale.

W R Berkley (WRB)

WRB operates as a decentralized insurance holding company which they effectively build complete companies around the type of expertise needed to excel in specialized markets and geographical territories. The result is WRB comprising of 59 businesses, each selling insurance in their own narrowly focused products, industry or territory. WRB has been underwriting profitably since 2001, while the whole P&C industry frequently makes losses.

The founder, William Berkley, still owns 20% of the company and his son (CEO) owns about 1.1%.

Copart (CPRT)

We waited 3 years for CPRT stock to be cheap enough, this year it has fallen significantly and so we rapidly built a 10% position. CPRT benefits from predictable trends from total loss frequency and the inflection of consignment to agency model in Europe. They operate in a duopoly and their competitor is much weaker in financial and operating terms.

The two-sided network effects and 90% ownership of land have been long-term strategic decisions that compound value.

It runs with no debt and management is very disciplined in capital allocation, refusing to repurchase shares unless they are very cheap. This is in stark contrast with most large companies that automatic repurchase shares without reference to intrinsic value.

Progressive (PGR)

We owned PGR since early 2020. The insurer is #2 in terms of premiums written in US auto insurance, overtaking Berkshire’s GEICO in recent years. Armed with a deep dataset and a pioneer in usage-based insurance, PGR is well-known for its underwriting prowess. It has been underwriting profitably since 2006.

Taking advantage of the hard market, PGR has re-priced higher aggressively in 2024 and has slowed down in 2025 as consumers are pressured by high insurance premiums. They have increasingly tied auto and home insurance together, reducing customer churn and hence lowering advertising spend per policyholder.

Policies-in-force are still growing at 11% YOY (Nov 2025), although this is more than half as slow in 2024. Pricing measured by premiums per policy is also largely flat YOY. Perhaps this was why the stock has fell by -17% in the past year.

Over the long term, float has grown at 16% for the past decade and PGR’s market cap has compounded 21%. We don’t think the economics have changed and added to this position.