CSU.TO: Constellation Software (4)

The 854 Businesses

Attached file is our database of all the businesses (as of Jan 2026) under CSU that’s identifiable on their website. In [data] tab, you can find:

Year of acquisition

Business Group

Name of company

Type of vertical market

Interesting info about them

We can’t vouch for the accuracy of the total 854 businesses, but we’re quite aligned with online sources quoting 800+ businesses.

Low Growth, Low TAM

There were 1,115 number of acquisitions since 2006, but we have only 854 businesses now. If we factor in attrition, the cumulative acquisitions is 1,071. We attribute the difference of 217 to consolidation over the years, since CSU only sold one company before.

We suspect consolidation because there are actually sub-divisions under the 7 main Business Groups. For example, Jonas Software has CORA, Vertus, Vesta each with different verticals under it.

The reason is probably due to the small addressable markets these companies have, it makes sense that when a company has run out of customers the employees can be combined with another division. For example, OMNITERM used to serve Singapore’s Cathay Cineplex until the cinema went bankrupt.

There’s no doubt that the growth is driven by acquisitions and the biggest risk is that one day the pipeline will dry up. This is not a new discovery, Leonard wrote about it as early as 2015, but the universe of VMS is very large, and since then CSU has acquired 892 businesses!

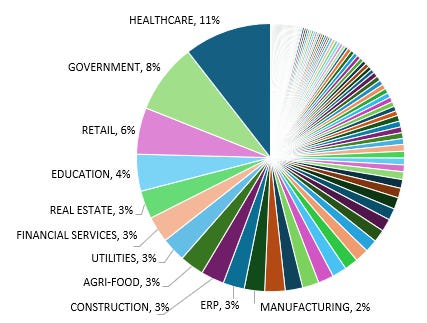

Types of Verticals

The businesses are very diversified across 109 different verticals. But Healthcare and Government make up almost 20%:

Actually, Government should be the largest pie because in some verticals (eg. Healthcare, Utilities, Justice) there are companies that are ambiguous in terms of category. For example, DATAMED (categorized as Healthcare) is part of national healthcare in Switzerland. Or, DELTA LOGIC (categorized as Justice) is for law enforcement, courts and public authorities in Switzerland.

Anyway, these types of clients give high recurring revenues due to the software's mission-critical nature in their operations, while costing a small portion of total expenses.

On the other hand, Retail can be quite generic with point-of-sales and e-commerce software solutions. The differentiating factor tends to be location specific. Examples:

SYMPAC: Australia timber and hardware industry.

FDT: Sweden retailers.

HACMEISTER+PARTNER: Germany fashion, footwear, sports consulting.

Very Unique

We spotted some really interesting and unique VMS that seems very difficult to break into:

TRANCITE LOGIC SYSTEMS: Car crash scene diagramming tool.

SIGNATURE RAIL: Railway scheduling with clients like Amtrak, Metro North rail (NY-Connecticut), ScotRail (Scotland).

TRAPEZE: Transportation mapping, used by Transport for London and Singapore LTA.

INFOCOUNCIL: For Australia and New Zealand local government meeting process.

RENAL INSIGHTS: For end stage renal disease and transplant in Canada.

BUYPASS: Norwegian’s digital security solutions.

MACOS: Pension sector in Switzerland.

ALTUROS: Has one of the largest skier communities “skiline.cc”.

CORE TECH: Ireland’s largest farmers’ co-op uses this.

The list goes on…

This is exactly why it’s not easy to just pick up the phone and call potential customers. Because even if you have the money, where are you going to find targets?

The ROIC Problem

We will make 2 predictions:

Number of acquisitions in the near-term will be low, because current market valuations are high and AI startups will ask for high prices. CSU is not interested in such games. If the cost of AI implementation causes IRR to sink below their hurdle rates, CSU will reject spending the money and be okay with collecting cash flows even if it means the VMS will eventually die off.

ROIC on future acquisitions will be lower because of size.

Combining this 2 points, we must then model out what kind of scenario is implicit in today’s share price.

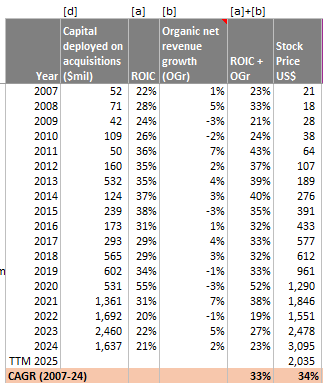

But first, let’s revisit the metric that Leonard used until he changed it in 2019: ROIC+OGr (organic growth).

Why he chose ROIC+OGr as a proxy for intrinsic value growth:

VMS is capital-light. So any organic growth from pricing will flow through to intrinsic value.

ROIC from new acquisitions is calculated as the cash returns on invested capital. Since CSU was able to reinvest 100% of free cashflows, this logically translates into intrinsic value growth.

If we compare ROIC+OGr to the long-run share price, it seems to proxy the +34% CAGR.

But we know that share price growth can actually be broken into underlying business performance and changes in price multiples. The former is the real intrinsic growth, while the latter is a price tag that the market assigns.

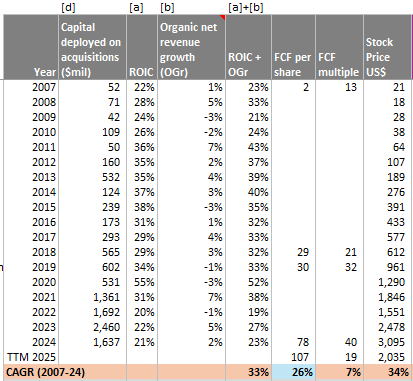

Suppose that FCF per share is a good measure for intrinsic value growth, then we can see that the stock price +34% CAGR was actually due to FCF/share +26% and FCF multiples +7%.

The ROIC+OGr metric had over-estimated intrinsic value, and this was why Leonard replaced it with FCF/share after 2018; he recognized the reinvestment rate is no longer 100%.

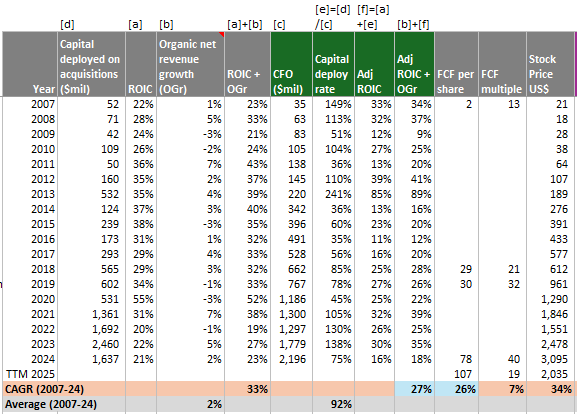

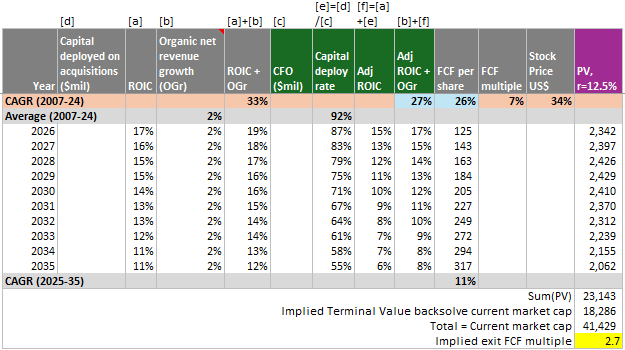

Now, what if we adjusted the ROIC+OGr metric to cater for a lower reinvestment rate? We know the cashflows from operations (CFO) and capital deployed to acquisitions, so dividing them we get the reinvestment rate. Turns out the average was 92%:

After adjusting, we see that the “Adj ROIC+OGr” actually explains FCF/share growth quite well (blue cells). Hence, we will use this for projecting future FCF.

These are our assumptions:

OGr maintains at 2%, contributed by inflation pricing.

ROIC decreases each year from 17% to 11%.

Reinvestment rate decreases each year from 87% to 55%.

Discount rate 12.5%.

Shares outstanding unchanged at 21.15 million.

Grow FCF by the “Adj ROIC+OGr” and find the sum of PV = $23b.

Back-solve for current market cap of $41b, terminal value = $18b. Implied exit multiple is only 2.7x FCF ($6.7b) in 2035!

We think such a scenario has very low probability of happening (refer to previous posts for reasons). That’s why we think this investment is of compelling value.

I’ve really been enjoying this series on Constellation!

What would you look for as a sign that Constellation’s businesses are under threat from AI competition? One of the challenges I’ve always found is the diversity of businesses makes it hard to know what’s going on in any of them individually.

When I was thinking had a look at Roper as a comparison for their future. Any chance that they’ll be able to get back to 100% reinvestment given there do appear to be lots of large VMS businesses in the market to buy each year?

Nice post and interesting way of approaching csu’s valuation. Thanks