CSU.TO: Constellation Software (3)

Click here for all other topics on CSU.

Software Stack

We have been thinking about the impact of AI on vertical market software (VMS). As the cost of coding decreases, the question of how AI can disrupt and/or benefit CSU is a popular one.

Like all good business analysis, we have to step back and examine where does value accrue in software, and the reasons why some companies capture the biggest value pie.

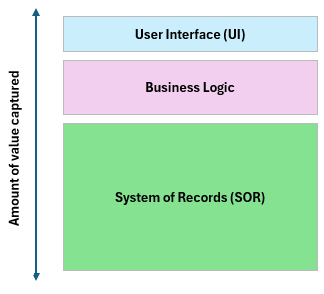

Let’s go back to the fundamental software stack. It has 3 layers:

Bottom Layer: System of Records (SOR)

This is where the company’s database sits. It’s the retrieval system serving as the source of truth.

Middle Layer: Business Logic

This layer interacts with SOR and pulls data, implements business rules, processes and workflows. This determines how data can be created, stored and changed.

Top Layer: User Interface (UI)

The top layer interacts with the end-user. We can think of this as an application (or UI) layer. The end-user can be a human or a computer.

This 3-layer architecture works because businesses need a reliable data source but employees generate data in fragmented ways. Think about how sales and expenses are generated in your own organization, chances are it’s coming from many different sources. In the end, all these data have to be reconciled into a single place.

That’s why if we go back into the 1990s, the software winners were those that dominated the SOR layer. Companies like SAP and Oracle focused on important areas like human resource management (HRM), customer relationship management (CRM), and enterprise resource management (ERP). These are acronyms that we’re familiar today, but in the early 1990s they were a very critical first step in software effectiveness.

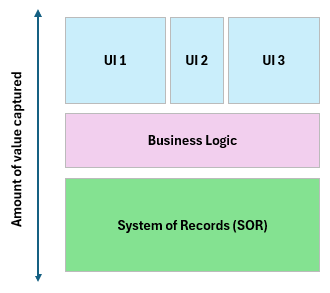

The value graph looked like this; the larger the box, the more value captured:

Moving forward into the 2000s, after the proliferation of the internet, software-as-a-service (SaaS) became a lucrative place to create value. As software became cheaper to distribute, we saw that the UI layer can be broken down in many specialized apps.

Companies like Docusign, Salesforce, Smartsheet popped up to create value by making the UI user-friendly. In the SaaS era that we’re in now, these business models took proportionally more value due to the low marginal cost of onboarding the marginal user.

The value graph looks like this now:

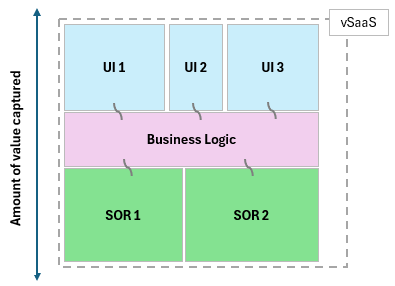

If we apply this thinking to vertical SaaS (vSaaS), it’s just packaging all 3 layers together as a single unit. However, this combined unit can only serve a narrow group of users. It’s obvious because all 3 layers will be different for all sorts of businesses. This also means that vSaaS cannot have a wide total addressable market compared to, for example, Salesforce which is a horizontal market CRM software.

These vSaaS businesses therefore capture the whole value range:

Examples of vSaaS companies are like Clio, Data Basics, Toast… We can see the customer stickiness when it comes to vSaaS.

Lawyers who use Clio are not leaving the platform because it’s built exactly for lawyers, and integrates with all other modules that Clio makes. It keeps every case and client connected, provides data security, automated billings etc.

Data Basics provides software solution for construction management. In construction, work doesn’t start until someone gets paid, and the payment rules can be very complex. There’s a lot of specific things like overtime pay, frequency of wages, clauses in contracts, union minimum wages, timesheet tracking etc.

Toast provides point-of-sales systems to help restaurants. The payment aspects in a restaurant is totally different from retail shops or a hospital. Fintechs like Square can be flexible across the horizontal market, but Toast is very specific and when it works, the switching cost is very high.

There’s one common theme: vSaaS customers are very sticky because the main operating expenses for them is labour, not software!

That’s why vSaaS (or VMS in general) have high recurring revenues and require little capital to grow.

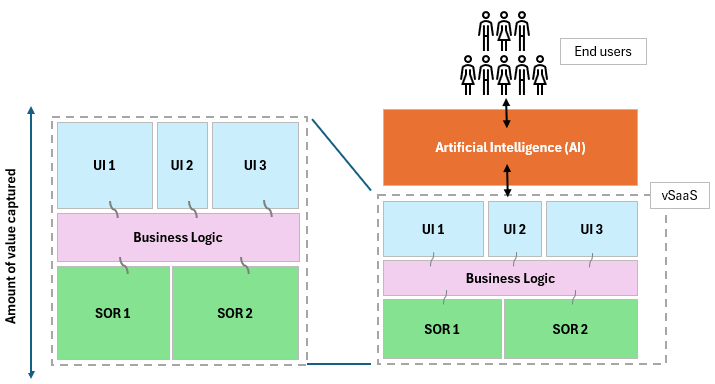

Enter Vertical AI (vAI)

AI is a transformative tech by essentially “commoditizing intelligence”. Although we don’t think intelligence in its true sense is going to be replaced, but we can already see huge productivity gains in coding. If we stretch our imagination further, there can be a situation where AI agents offer a “do it for me” value proposition.

This idea is not new, Jensen Huang has said that AI will be the layer sitting on top of the software stack.

Could we imagine vAI taking a larger share of value, as a result shrinking vSaaS?

No, we will argue this outcome is unlikely.

Imagine two software companies in the roofing industry:

RoofOld is a vSaaS that has all the software a roofing contractor needs. CRM, scheduling, project management, inventories, payroll, accounting etc.

RoofGPT is a vAI who wants to disrupt.

But how is RoofGPT going to disrupt without first owning the system of records (SOR) layer?

Let’s say RoofGPT tries to attack the weak spots of roofing companies like offering smart and polite AI agents who can pick up every customers’ call. The problem is no matter how intelligent these systems are, they are disconnected from the core business. For example, if someone calls to reschedule his roof inspection, to answer this question RoofGPT needs to integrate into the employee schedule sitting inside the SOR layer.

Who owns the SOR?

Well, it’s RoofOld in the first place! The beneficiary of AI implementation is RoofOld rather than an outsider.

There’s actually a scenario that can be made in favour of RoofGPT. If all the roofing companies used fragmented software for each function (eg. HR related from Oracle, inventory management from Glide…), then RoofGPT can build API across all of them.

However, that’s not the case in reality for many vSaaS these functions are already consolidated. This presents an interesting business dilemma for RoofGPT, they can do 2 things:

Be vertical. Integrate with RoofOld software and become a “super-friendly & intelligent UI”.

Be horizontal. Don’t integrate and don’t have access to the SOR, but provide low-cost super-intelligent services that roofing companies don’t have budget to hire people for.

For #1, RoofGPT will be beholden to RoofOld, which means additional value will likely accrue to RoofOld.

For #2, without access to the vertical, RoofGPT will risk commoditization from increasingly capable horizontal AI tools.

That’s why we think vSaaS will continue to prosper and benefit from AI, instead of being hurt by it.

The horizontal software business is a “wrapper”. SaaS companies wrap around cloud providers, which wrap around hardware manufacturers, which wrap around semiconductors… AI could probably wrap SaaS up.

But VMS is different, we have argued that it is quite resilient to wrapping. That’s why we are convinced that CSU who owns high-quality VMS companies, and hence all 3 software layers and the talent pool, have a long runway to continue to compound.

Thanks for this write up, I think a very good way to depict the value chain in a simple and concise way. A quesion I had was around the assumption that these vSaaS are already integrated, don't you think that the AI layer can come just on top of the business logic and UI layer making both those obsolete? I understand it cannot do it now but wouldn't that be an outlook we need to consider five ten years from now? How do you think CSU could protect itself from that moat.

Completely get the SOR part but I feel the other two layers are not really protected. Would love to get your take.

great stuff, thank you! regarding the example of RoofOld and RoofGPT - i agree on the statement when it comes to existing customers, but what about new potential customers down the line? any different thought process there?