CSU: Constellation Software (5)

Intro

This post will be a CSU related one, we will discuss the Q1 2026 results of Topicus and Lumine, both spin-offs from the CSU family.

Without going into the history of these two companies, it’s important to know that CSU economic interest is 48% in Topicus, and 61% in Lumine. CSU also has super-voting shares, so effectively it has control over them.

Obviously the operating results of Topicus & Lumine will affect CSU and because both spin-offs operate the same business model as CSU, their results and management commentaries contain interesting lessons we can learn.

Both firms are serial acquirers in the VMS (vertical market software) market. Topicus focuses in Europe, while Lumine is in the telecomm industry.

Topicus Q1 2026

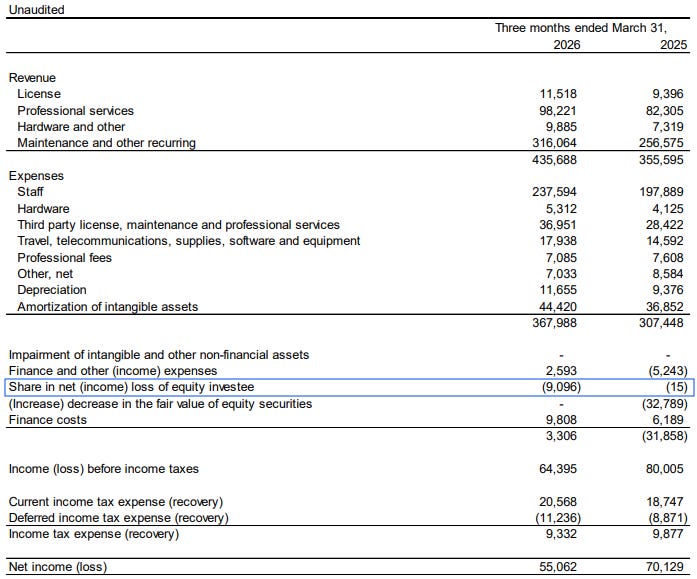

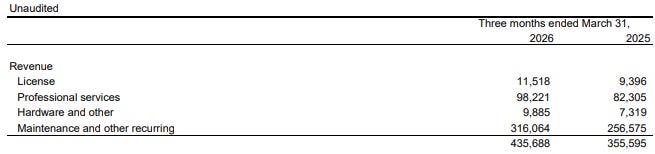

First let’s look at the key YOY metrics:

Revenues grew +23% from €356m to €436m.

Total organic growth +5%, last year +4%.

Net income fell -21% from €70m to €55m.

Operating cashflow +3% from €271m to €280m. Free cashflow (FCF) +2% from €162m to €165m.

Only €22.5m deployed for acquisitions. Paid off €245m in revolving credit facility.

Net Income

It’s strange at first glance, why did revenues grow +23% but net income fell -21%?

Surely we know that using the P&L to value serial acquirers is often a big mistake. The P&L is an accountant’s opinion and for Topicus it’s full of accounting noise.

Last year Q1 2025, Topicus acquired 8.3 million Asseco Poland shares (9.99% stake) on the public market. Since it’s an equity investment, the P&L recorded a €32.8m fair value gain.

Then, on October 2025, they bought another 12.3 million shares, bringing the total stake to 24.84%.

Because Topicus now has significant influence over Asseco Poland, the accounting treatment became equity accounting method. Now, there’s no more fair value movement, for comparison purposes we remove the €32.8m gain last year, then net income would be €37.2m.

We also remove €9.1m from the proportional share of Asseco’s net income this year.

Therefore, Q1 2026 net income €45.9m is actually higher by +23% on a comparable basis (Asseco’s stock price more than doubled in 2025).

In equity accounting method, the Asseco investment is recorded on Topicus balance sheet at cost and subsequently adjusted for their share of profit/loss. The proportional share of Asseco’s net income shows up in Topicus P&L:

This is a non-cash entry and doesn’t affect cash flows. Only dividends paid by Asseco would affect cash flows, but none were paid during Q1.

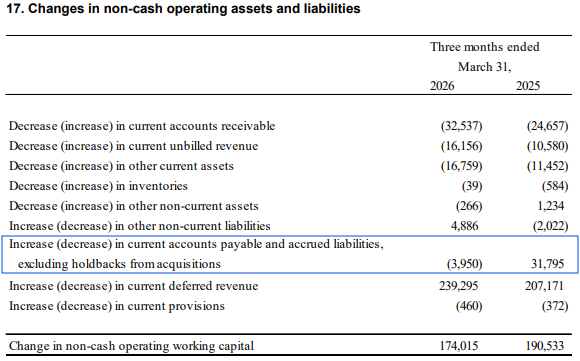

Operating cashflow (OCF)

After explaining the P&L movement, you might go to the cashflow statement and think that OCF should increase substantially. But it only increased by +3%. Considering the fact that most customers pay their software fees in Q1, we should see a huge surge in cash consistent with revenues.

So what happened?

Go to note 17. Last year, Topicus delayed payments and had increase of €31.8m in payables. This year, there was no such delay. The negative swing of €36m is timing difference. If we remove this, OCF would increase by +15% YOY, which explains the FCF variance too.

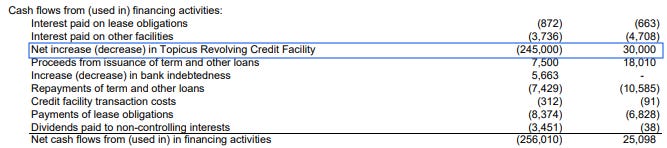

Debt

Topicus used a €200m loan to partly finance the purchase of Asseco. At end of 2025, their current loan liabilities was €345m. In Q1 2026, it went down to €96m. Topicus paid down €245m of loans:

The net debt is currently at €117.5m, while Q1 FCF of €165m is more than enough to cover. The balance sheet has improved massively in just one quarter.

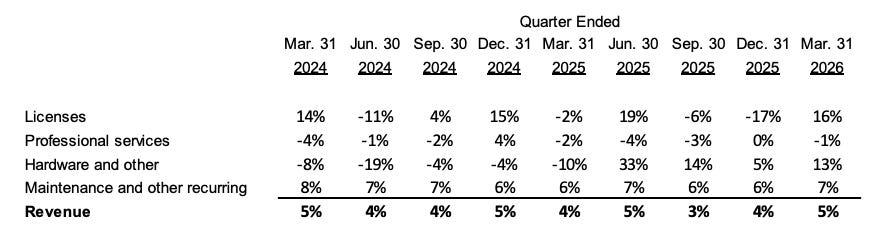

Organic Growth

This is where we find no signs of AI disruption in the VMS space. Organic revenue growth is still +5%, well above inflation. More importantly, the “maintenance and other recurring” line grew +7%.

Maintenance revenues are the lifeline of Topicus business. These are fees paid for software updates, improvements and renewals. It’s very predictable due to its recurring nature, and it carries high margins.

The AI disruption narrative, if true, should negatively impact maintenance revenues. But we don’t find evidence of that yet.

Acquisitions

Another area that investors look at is acquisitions. Because a huge part of the revenue growth comes inorganically. There’s a concern that customers would start using AI to make their own software and the pool of VMS businesses will shrink.

In Q1 2026, only €22.5m was used for 3 acquisitions, none of them were deemed to be individually significant. They included software companies catering to automotive, planning, government, chemicals, healthcare, legal, gaming and education verticals. All of which are similar to existing businesses operated by Topicus.

An amazing statistic: In 2021 when Topicus was spun out, it had 77 VMS companies. Today, just 4 years later, it runs 169 companies!

Yes, Q1 2026 reported low activity, but the historical growth should tell us what Topicus can do when prices are good. Purchase price discipline is still the cornerstone of value creation.

Software valuations have cratered in public markets, but it’s different for private markets. Owners of private businesses can only sell once, in such an arrangement you will not get irrational prices.

If private VMS companies are still not cheap, it means that they still think that their businesses are not threatened by AI.

Mark Miller (CEO of Constellation Software) commented on this subject:

We haven’t really seen on the private side any change in pricing so far, and competition for those businesses is still very strong. Nothing’s changed there. There’s just been a little bit of change in pricing for publicly traded companies, as you well know.

Dutch Tax Dispute

The Dutch Tax Authorities are challenging the deductibility of Topicus employee bonus program for years 2016 through 2018 onwards. The potential liability currently is at €8.4m.

Lumine Q1 2026

First let’s look at the key YOY metrics:

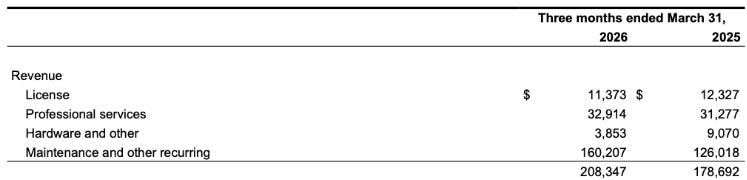

Revenues grew +17% from €179m to €208m.

Total organic growth fell -2%.

Net income fell -9% from €21m to €19m.

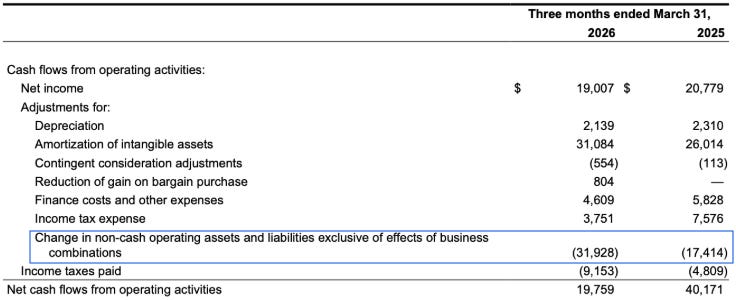

Operating cashflow -51% from €40.2m to €19.8m. Free cashflow (FCF) -56% from €35m to €15.3m.

€309m spent for 100% stake in public company Synchronoss Technologies, financed partly by €160m loans.

Revenues

Lumine didn’t fare as well as Topicus in terms of core business improvements. Organic growth fell -2% attributable to licenses and hardware, but maintenance and other recurring revenues grew +3%.

This is actually good news. Look at the revenue mix, similar to Topicus, maintenance revenue (77% of total) is the most important:

Hardware and licenses require more capital to generate growth and are generally low-margin items. Quality over quantity!

Furthermore, Lumine operates in the telecomm software space. This is not a market where budgets are high, yet Lumine was able to grow organic maintenance revenues at inflation rate. To be able to pass on inflation through price increases tells us that these VMS are mission-critical.

Nobody is changing their mission-critical software to save a few points in margins.

Free cashflow (FCF)

Why did FCF fall by -56% YOY?

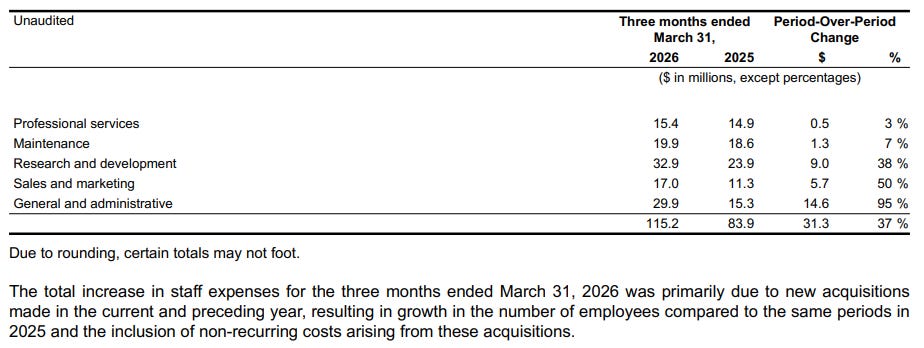

This has to do with the acquisition of Synchronoss. After buying the whole company, Lumine effectively inherited their cost structure. This bloated cost structure needs to be cut, and Lumine must show that they can operate Synchronoss in a much more efficient way.

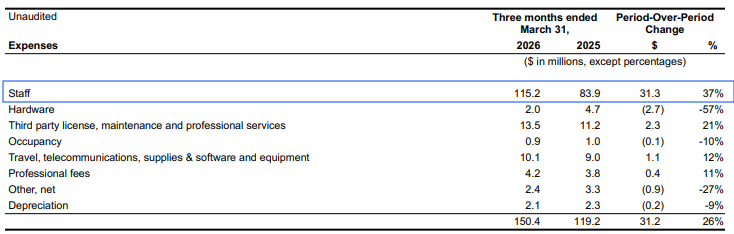

In expenses, the increase was driven by higher staff cost arising from acquisition:

We think that this cost base is not permanent. If we believe that Lumine, being a spin-off from CSU, is a disciplined acquiror. Then it implies that they must have a plan to reduce the cost base, a potential for margin expansion.

Of course, success is not guaranteed, we have to monitor this situation. This is the largest cost optimization project that Lumine has taken. If done poorly, customers could churn, employees could leave. We should highlight this risk.

Working capital was also affected by inheriting Synchronoss receivables, the negative impact was -$32m. This will convert into cash over time.

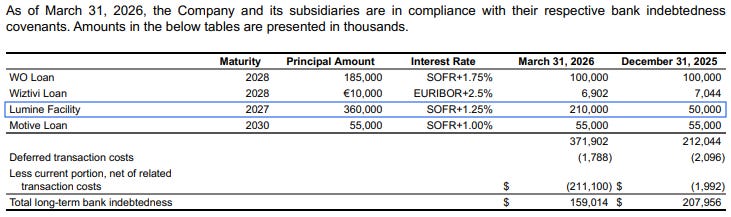

Synchronoss Term Loan and Facility

On 1 May 2026, Synchronoss entered into a financing agreement for a term loan in the amount of $110m and a revolving credit facility amounting to $10m million. The term loan is 5% per year, maturing in 2030. The loans are collateralized by substantially all of the assets of Synchronoss.

This is subsidiary debt, ring-fenced from Lumine — classic CSU playbook. In fact, this is true for all their subsidiaries (WideOrbit, Wiztivi, Motive).

Lumine’s own corporate revolver extended to June 2029 with $360m capacity plus cash of $248m.

Conclusion

So after going through some mental pain looking at the details, we hope you see that the CSU-related businesses are still healthy and prospering. This applies to CSU as a whole, we remain optimistic about the durability of VMS and the effectiveness of CSU capital allocation.

Headlines are often misleading and the gems are in the details. With stock prices falling, the only place to gain clarity is to reason through the details.

Great analysis! The underline summarizes well this whole thing. Headlines might mislead judgement. In case of of Topicus, such a break down analyais is very much required to understand that the company can createe value for investors rather than the opposite.