CPRT: Copart (8)

Intro

It’s well-known that CPRT owns 90% of their land and this is one of their strongest competitive advantages against IAA. In the salvage auction industry, when a car is deemed totaled it has to be parked somewhere and it sits on special permit land for up to 3 months before titles are being processed and eventually auctioned off.

Intuitively, we know that land is a cornered resource, but we have not explained what would CPRT look like if it had leased its land instead. The motivation of this exercise is to explain why CPRT is able to produce exceptional operating margins above 30% every year and boasts an average of 36% for the past 10 years.

Why can an industrial-like company produce such high margins?

This article will try to put the qualitative moat into numbers.

Quantify the Land Moat

Firstly, leasing land requires you to pay rent and thus reduces operating profits. But if you own the land, there’s no rent, instead you capitalize the land on the balance sheet. Since land doesn’t depreciate in value, there’s no depreciation & amortization (D&A) associated with owning it. The only D&A is from buildings and equipment on your land, but not the land itself.

Secondly, land improvement accounting treatment is different under leases. IAA uses long-term (10 to 15 years) leases with 5-year renewal options. Whenever IAA wants to do improvements on that land, like build better facilities, they can depreciate that expense over 10 to 15 years.

CPRT is different; for those lands that they fully own, land improvement projects would be capitalized as an asset on their balance sheet under Property, Plant & Equipment. This depreciation schedule can be 15 years to 39 years depending on the facility built.

These two differences would mean CPRT’s depreciation and lease expenses are much lower than IAA. This is a simple explanation of why CPRT’s operating margins are so good. However, we must ask what is the true margins of the underlying salvage auction business?

Because if we don’t strip out the benefits of land ownership, then we might be blinded by the accounting treatment and fail to identify when the core business is suffering.

On CPRT balance sheet, the value of land is recorded at historical cost. So those land purchased decades ago are grossly understated. Even since 2020, industrial outdoor storage real estate have increased by 123%, so it’s safe to say that land purchased long ago would be worth much more than what’s stated on the balance sheet.

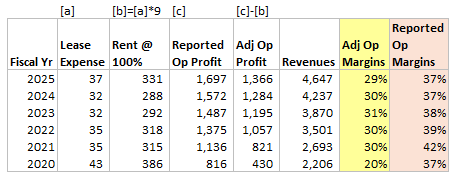

We could try to estimate the actual value of those land and apply a cap rate to estimate rental expenses. But there’s an easier way, since we know ~10% of land is leased, we can just work out what the rent would look like if CPRT leased 100% of land:

The adjusted op margins (yellow column) represents the core operating auction business. It is surely lower than reported figures, but still quite impressive at 28% average. In other words, the huge margin difference of 1000bps is attributable to the strategy of owning land.

Despite this adjustment, IAA is still inferior to CPRT. Their 5-year op margin average was 22%.

More importantly, the 1000bps margin spread represents the return on CPRT land ownership strategy. This is a quantification of their competitive moat. Put another way, CPRT has cornered a scarce resource while, at the same time, hedged against rental inflation. The rental expense actually turned into retained earnings for CPRT, while IAA has to pay their landlord to be in business.

Cash Flows

You might disagree and say that the P&L is just an accountant’s opinion, there is still real cash outflow regardless if you pay rent or buy land.

Yes, cash has flowed out in both scenarios but the quality of the outflow matters.

What do we mean?

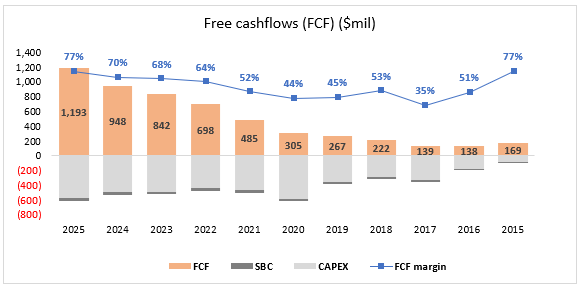

First of all, to correctly think about these 2 scenarios we have to use free cashflows (FCF).

The crucial metric is FCF margins; how much of net income is converted to FCF:

In the last few years, FCF margins have improved substantially compared to a miserable 15% FCF margins for IAA in 2022 (their last year before going private to RBA).

This is what we meant by the quality of cashflows: Spending $1 on land CAPEX is superior to $1 on rental. There are two forces at work here:

Rent buys only temporary occupancy. The cash spent disappears after the rental period.

Cash is constantly losing value due to inflation, while land (especially special permit junkyards) appreciate in value.

Therefore, when CPRT buys land outright, they are essentially trading depreciating cash for appreciating land!

Point #2 above is important. The ownership of land creates a natural inflation hedge, when inflation hit rent prices, IAA has no choice but to bear the consequences. There’s no alternative, since no land means no business.

In contrast, CPRT cash cost is fixed at the moment they bought land. Think about the “inflation cost savings” from land purchased 20 years ago!

Point #1 also implies that IAA as a lessee has no control over their rent payments. When a contract says they have to pay for the next 5 years, it doesn’t matter if business is bad; IAA must pay up.

CPRT has discretion to spend on land whenever they see opportunities. For example, if land prices are unreasonable, they can stop buying land and FCF will immediately improve.

Conclusion

The foresight that Willis Johnson had to own land is a testament to his brilliant business acumen. This resulted in CPRT having a cornered resource while hedging itself against inflation. Rather than spending inflated dollars on leases, CPRT business model converted them into retained earnings for shareholders.

Every year that passes, the economic moat widens against their competitors.

That said, as investors we should be aware that looking at margins on a total level is mixing up the benefits of land ownership with the core operations. To figure out how the core business is doing, we need to find reasonable ways to strip out the effects of land ownership.

Never looked at the company, thanks for introducing something new to me. Looks great in a lot of areas.