CPRT: Copart (7)

Operations: From Junk to Gold

The business of CPRT starts with a wrecked car in an accident. We follow this chain of events that would lead to CPRT making profits:

1. A wrecked insured vehicle can be a result of car accidents or natural disasters (hurricanes, flood).

2. Vehicle is towed to nearby holding yard (can be an auto shop).

3. Insurance adjuster comes to inspect the car. If this inequality is true, the car gets totaled:

cost of repair + salvage value > pre-accident value

4. Suppose that the car is totaled, the insurer will pay the claims and the driver signs the title of his vehicle over to the insurer.

5. The insurer now holds a wrecked car in a place which charges storage fees, so they need it to be gone as soon as possible.

6. CPRT sends a tow truck to move the car into one of its nearest 200+ junkyards scattered across nearly all US states. This tow fee will be reimbursed by the insurance company after the car is sold.

7. CPRT logs the car registration number and cleans the car up. They work with the DMV (Department of Motor Vehicles) to change the title to “salvage vehicle”. This adds immense value by handling the administrative burden. CPRT ability to navigate the varying regulations of 50 US states and dozens of international jurisdictions constitutes a significant service moat.

8. CPRT takes photos and videos of the car and puts it on their auction platform. This is the only thing the buyer will see when committing to purchase. In the past, these types of vehicle auctions were performed in-person and came with all the inconveniences, restrictions, and inefficiencies. No one is going to fly to the US or drive across the country to auction on a salvage vehicle. Today, this is all done online via Copart’s website/app.

9. The final buyer pays the winning bid plus buyer fee (based on selling price), gate fee (to move car out of yard), internet bid fee.

10. CPRT pays insurance company the winning bid less towing fee, titling fee, sales fee.

Finally, we reach the end of converting junk to gold: CPRT pockets all the fees from buyers and insurers.

This chain of events is a win-win value proposition for all parties involved:

Buyer gets a cheap car good enough for use.

Insurers reduced their claims losses.

Tow and facilities workers get paid for work.

CPRT profits from operating the ecosystem.

The incredible economics is that CPRT doesn’t own the inventory. They are acting as an auction platform, providing administrative services and storage facilities. This is an asset-light model although land is the main physical asset CPRT needs. Because CPRT owns more than 90% of their land, this actually becomes a competitive advantage.

Furthermore, land only appreciates over time, meaning that the property values recorded on the balance sheet are at cost, which significantly understates the actual land value.

Competitors going against CPRT need a lot of land, and it is increasingly difficult to get permits; there are many regulatory hurdles due to toxic waste treatment. No one likes junkyards in their town, and so most of the good locations (near high-population areas) are already owned by CPRT.

In short, CPRT is a capital-light business (auction platform) built on irreplaceable and hard to obtain physical assets (special permit land).

Agency Model

The primary buyers on CPRT auctions are vehicle dismantlers, rebuilders, repair licensees, used vehicle dealers, exporters, and the general public.

Vehicle dismantlers, which are the largest group of vehicle buyers, based on volume of vehicles purchased, either dismantle a salvage vehicle and sell parts individually or sell the entire vehicle to others.

Vehicle rebuilders and vehicle repair licensees generally purchase salvage vehicles to repair and resell.

Used vehicle dealers generally purchase recovered stolen or slightly damaged vehicles for resale.

By region, 60% of buyers are from America, of which 70% are from a different state. 40% are international buyers.

Therefore, the types and location of buyers are very diversified, which is a competitive advantage where a global fragmented buyer base will attract more suppliers to CPRT auction network.

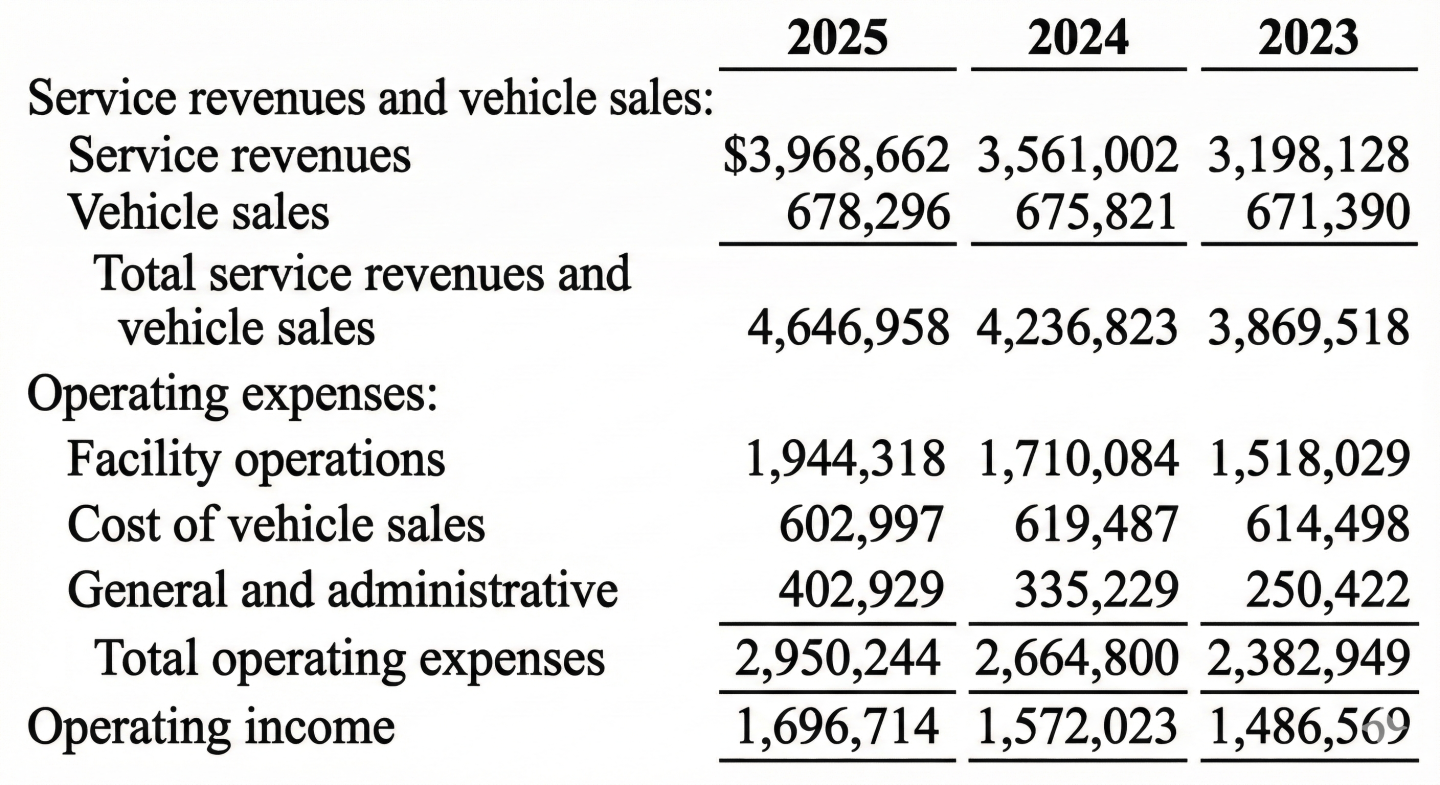

This is called an agency model where CPRT doesn’t own the inventory but simply possesses it. They are only responsible for facilitating the sales. This is catergorized as service revenues on the P&L.

Principal Model

Theres a smaller portion of revenues that come from CPRT actually buying and reselling salvaged vehicles.

This is primarily done in Europe (UK, Germany, Spain) as they expand overseas. The cost of those vehicle sales is booked as cost of vehicle sales.

The strategic goal is to minimize principal model and maximize agency model, for the obvious reasons that profit margins are much better:

The vehicle sales segment has thin 11% margins, while service revenues enjoy fatter margins at 42%.

Furthermore, the land depreciation charges associated with service revenues are very small (2025: $191m). Considering the land will last for a long time, appreciates in value, and doesn’t require much upkeeep, we think its essentially the best kind of hard asset.

So why does CPRT bother to still operate a principal model?

There’s 2 main reasons:

As long as it’s profitable, these cars increase the supply in auction. More cars attracts more buyers. It widens CPRT two-sided network moat.

Historically, UK and German insurance companies did not operate on agency model. They used to sell salvage vehicles to a scrapyard and get their cash immediately, but the price discovery is obviously bad. As early as 2012, CPRT has used the principal model (buying the cars themselves) primarily a means of gaining trust and market share. After years of hardwork, CPRT has slowly proven that the agency model benefits both parties and converted them.

It’s helpful to know that transiting from principal to agency model reduces revenues but improves margins. Because CPRT no longer records the full price of a vehicle sale (lower revenues), but at the same time they don’t incur cost of vehicle sales (higher margins).

Increasing Supply

A critical ingredient of a successful network moat is the high quantity and quality of supply.

Examples of how CPRT increases the supply and diversity of salvage vehicles:

1. In 2024, CPRT acquired a controlling interest in Purple Wave (online auctioneer of construction and agricultural equipment). This move diversified the asset mix away from passenger vehicles and tapped into the infrastructure and farming sectors.

2. In 2008, CPRT acquired parts recyclers in the UK (branded as “U-Pull-It”). This allowed capture of some value from end-of-life vehicles by selling individual parts before scrapping.

3. In 2017, the acquisition and integration of National Powersport Auctions (NPA) allowed CPRT to enter the market on pre-owned powersports vehicles.

Capital Allocation

The thought process of capital allocation is straightforward, although operationalizing it is not easy.

The US market is quite saturated by the duopoly of CPRT and IAA. The way CPRT expands overseas is through:

Acquire salvage/auction related companies.

Acquire land.

Develop land.

Operationalize their business model.

First, CPRT buy the dominant auction house/reseller in the region. In the UK, they bought Universal Salvage to instantly get contracts with UK insurers.

In Germany, it was Wreck Online Market (WOM), a software platform used by insurers to value wrecks.

In Brazil, they bought Central de Leilões, a local auctioneer in São Paulo.

In Spain, the target was Autoresiduos, a valuation platform.

After getting the contracts, CPRT starts to acquire land. They try to wholly own land as much as possible, otherwise they will lease.

CPRT doesn’t pay dividends and shares repurchases have been rare (3 times since 2011) as the stock is usually expensive. Operational expansion made the most sense, this has proven to be true with historical ROIC averaging 27% since 2015.

Recent insurance premiums inflation have caused volumes to slow down as more people go uninsured. Despite this, FY2025 ROE was 20%, a very high figure for such a predictable business with zero debt leverage. Even better, they have $5.2b of cash, which means ROE would be higher if this cash were to be reinvested.

The balance sheet is very strong with total liabilities at only $962m, none of it comprises of long term debt.

Competitor: IAA

The most recent industry news was that RB Global (the entity which now owns IAA) reported rising volumes. The decline of CPRT’s US insurance-related volumes was made more ugly by IAA growth.

The duopoly dynamic is such that insurers don’t want to allow a monopoly marketplace, since they will be hostage to pricing. Even though CPRT is operationally superior to IAA, especially in terms of land ownership and auction depth, insurance companies like Progressive (PGR) still prefer to supply IAA (GEICO uses Copart).

By leasing most of their land, IAA made a structurally weaker choice. Because they will always be hostage to land developers who will prefer commercial/residential real estates over junkyards, this pressure is even more real when these plots of land are near populated areas. Over time, landlords will have bargaining power over IAA. When there’s no land, the business falls apart.

IAA tackles this problem by focusing on moving vehicles off the yard much faster, increasing the amount of volume they can handle. The less time vehicles need to spend in the yard, the less that land matters from a day-to-day operational perspective.

However, CPRT land ownership strategy makes them the lowest cost producer of this industry. If they wanted to, they could slash their seller fees, reduce net margins by half, and drive IAA out of business (IAA net margins ~14%).

Fortunately, CPRT management is not interested in price wars, instead focusing on operational efficiencies. For example, Q1 2026 reported 9% decrease in time taken to process a vehicle from assignment to sale. We love to invest in industries with rational pricing.

To summarize, this recent shift of volumes to IAA is a natural flux on the part of insurers. We can’t tell whether it’s done on purpose or just because PGR gained market share in recent years, but we know that insurers prefer competition (duopoly is better than monopoly). The push to speed up cycle times at IAA paid off so far. That said, the outright ownership of the land represents three decades of strategic positioning by CPRT. This structural advantage cannot be replicated and should win out in the end.

Conclusion

CPRT at $37.2b market cap is trading at TTM PE 24x and FCF yield 3.2%, keeping in mind cash of $5.2b (13% market cap).

The valuation is obviously fair given a IRR 10%, ROIC 27%, the implied growth is 7%. Not a difficult hurdle to pass.

CPRT is a business with strong structural advantages that can’t be disrupted, and supply/demand tailwinds that promises predictable, sustainable growth for a long time.

The deal is sweetened with a fortress balance sheet with zero debt, and operations that produce more operating cashflows than net income.

Lastly, we get CEO Jeffrey Liaw who is exceptional at capital allocation. The board also has ownership stakes with founder Willis Johnson 5.75% and Jay Adair 3.14% (previous CEO, son-in-law). Jeffrey Liaw holds 3.3 million shares worth ~$127m against his $900k salary which was unchanged for 3 years.