CPRT: Copart (5)

Recap & FY2025 Update

Since the last post at end of May, CPRT stock continued to fall by -13% and it’s trading at $43.7b market cap now.

As of FY2025 (fiscal year ended July), CPRT has $4.8b of cash and US Treasuries (<12 months maturity). This is 11% of the market cap.

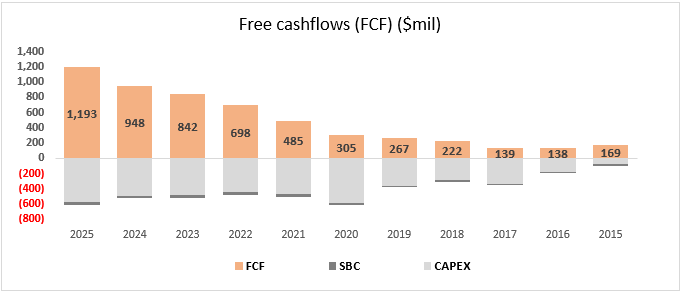

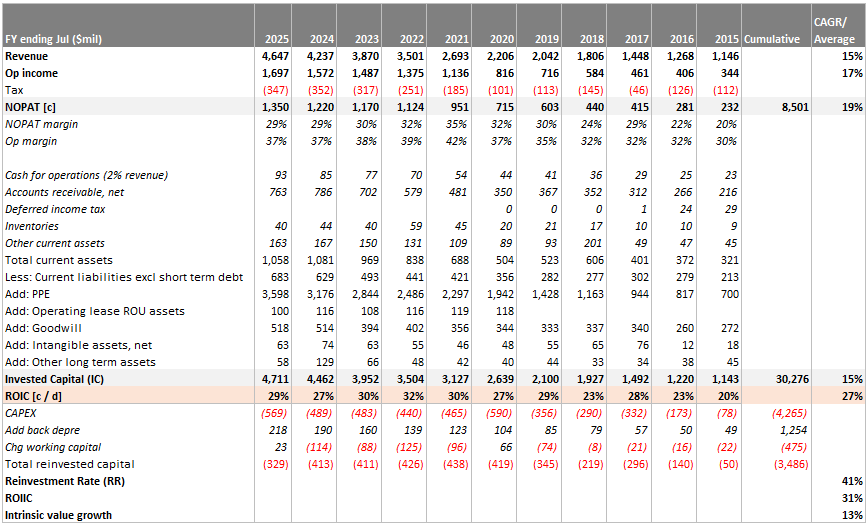

The cash build-up was simply due to operating and growing the business. Free cashflows (FCF) are at record highs at $1.2b:

CPRT has no debt obligations. Total lease expenses for FY2025 was $36.8m, which are easily covered by interest income from the $2b invested in US Treasuries. Net interest income was $179m. This is the good result of CPRT owning 90% of their land.

On the P&L, revenues grew +9.5% while operating income grew +8.3% YOY. Operating margins were slightly lower due to softer volumes and a mild hurricane season. Usually, bad hurricane seasons bring a lot of salvage volumes, CPRT incurs expenses to acquire land in anticipation of adverse hurricane events, but when they don’t occur it can temporarily depress margins.

The market sell-off seems to be hinged on the concerns of CPRT losing market share to IAA, resulting from reports of declining unit volumes.

We think this is a mistake that casual investors run into when taking market share reporting at face value.

We will explain why unit volumes have decreased and how these are not reflective of a declining business.

Uninsured Motorists

Fee units, which represent the vast majority of CPRT unit volumes in the US, include vehicles consigned by insurance companies to CPRT. Recent trends indicate weaker performance in the US.

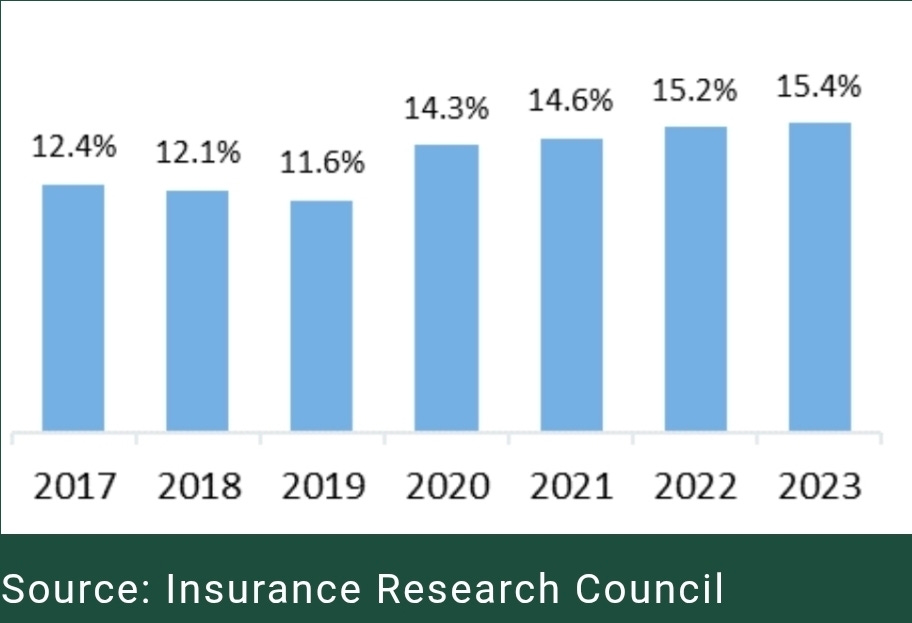

A significant factor is due to the increase in uninsured motorists, driven by higher insurance premiums in recent years. This is caused by insurers passing through inflation costs down to consumers.

Therefore, we see an increase in people who can’t keep up with prices and decide to go uninsured, although it’s illegal to drive without insurance.

Below is the trend of uninsured motorists in the US:

These people simply fall out of the traditional total loss equation and would not contribute to CPRT volumes.

We think this is not a structural issue but a temporary one. Before 2020, we actually see a lower stable rate of uninsured before the recent inflation impact.

It is reasonable to expect a stable or slightly declining uninsured rate as people become more affluent, and the costs of uninsured driving outweigh the benefits of being insured. Especially when it’s illegal to drive without insurance!

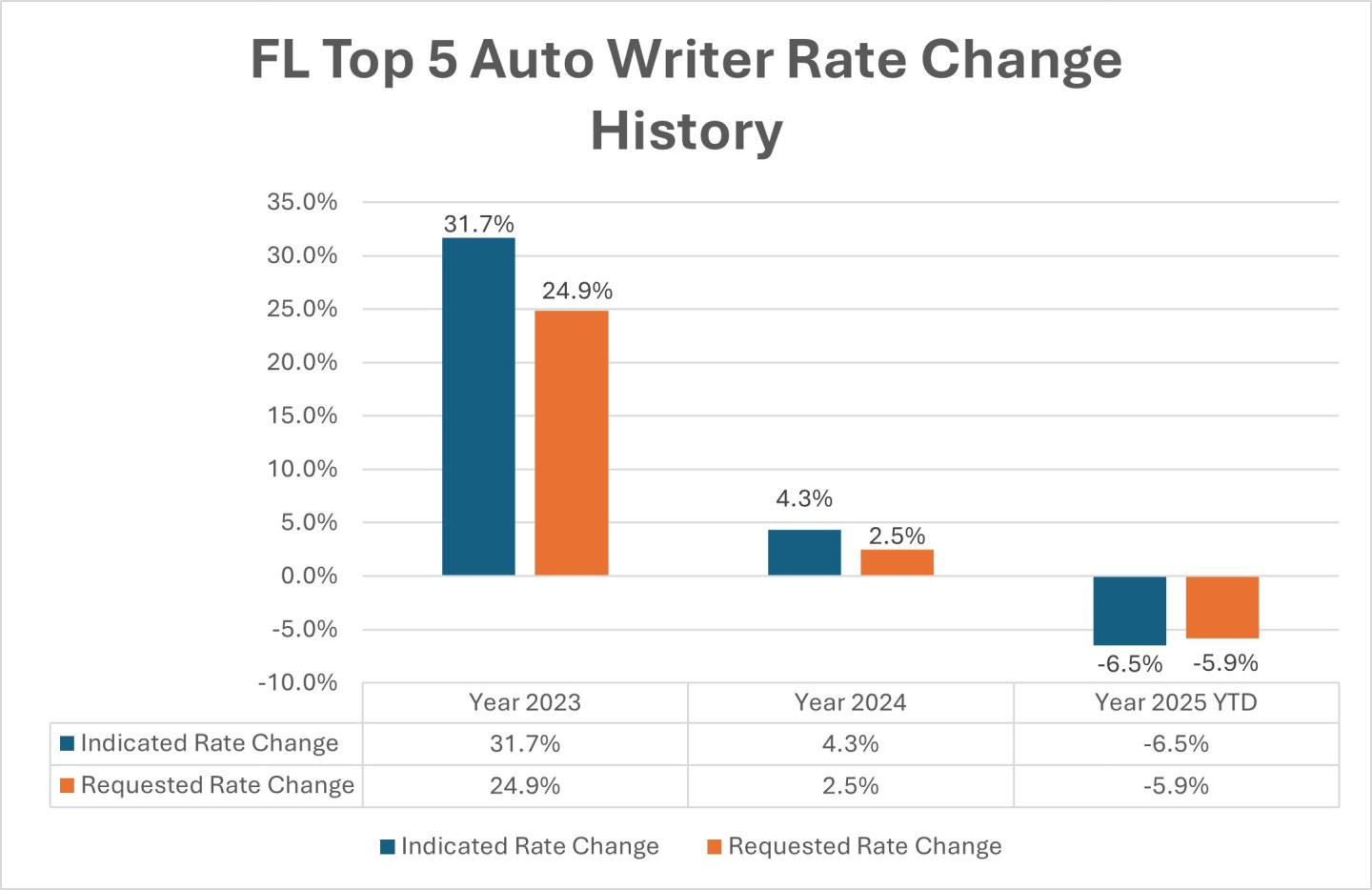

We are seeing state insurer commissioners trying to make insurance premiums more affordable. For example, in the state of Florida:

Less Focus on Low Value Units

CPRT also recently reduced its focus on certain low-value fee units. For example, early this year, it was mentioned that units from charities and municipalities decreased by -4% in Q1.

They also moved many of their low value non-insurance units to the direct buy channel. The reason for this was to allow CPRT to efficiently market lower priced vehicles by directly connecting sellers and buyers and avoiding the unnecessary costs associated with transportation and storage.

Reported headlines like this look daunting when we don’t look for details:

Global insurance volumes sold decreased by -1.9% in Q4, with US volumes declining by -2.1%.

Q4 unit sales in the US declined by -1.8%, with purchase units dropping significantly by -16.7%.

We think this is also not a structural weakness but a strategic shift to higher margin segments. This will cause IAA market share to increase, but they are taking low-priced units.

Last quarter, the US average selling price (ASP) of CPRT grew +2% while IAA fell -3%.

In the most recent quarter, ASP of CPRT grew +5.7% while IAA grew +1.1%.

European Markets

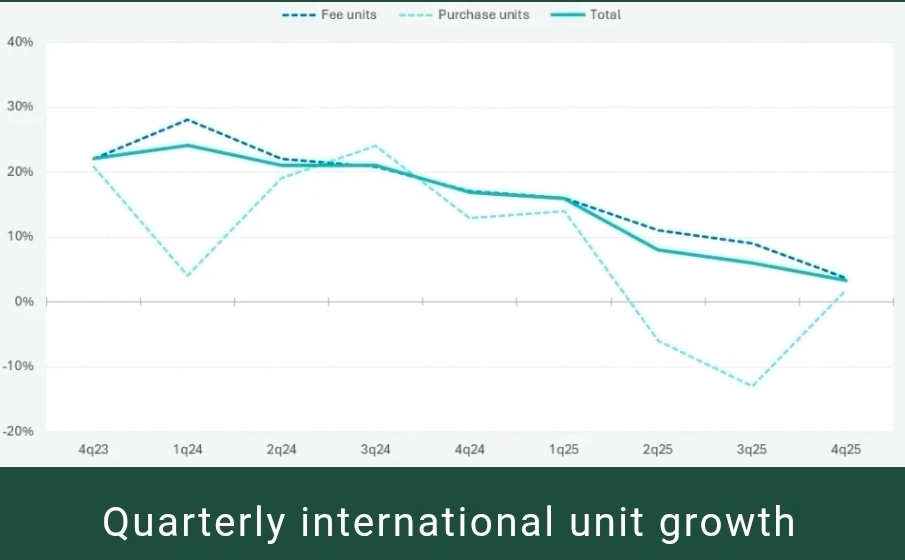

The transition to a consignment model in Europe seems to be accelerating. We see the evidence in two places:

1. Growth in fee units sold continues to be greater than growth in purchase units sold.

2. Significant increases in operating margins for International region over the last several quarters.

With respect to the International segment, purchased units declined over the last several quarters were largely due to the shift of insurance units transitioning from purchase contracts to consignment (mostly in Germany). This move impacts reported revenues, shifting it from gross vehicle sales to service fees.

While this reduces purchased units revenues and volumes, it benefits fee unit growth and aligns CPRT interests with insurers. Instead of buying salvage vehicles from insurers, it’s more efficient for them to go with the consignment model.

This is a long-term strategic goal, and it’s how the US domestic operations are run. CEO Jeff Liaw noted this progression is gradual but is the desired direction for the business.

For context, CPRT entered Germany in 2012 and has slowly and persistently attempted to persuade insurers to shift to a more profitable way of dealing with damaged vehicles. Historically, policyholders in Germany have retained the damaged vehicle after an accident rather than the insurance company. Changing an old way of doing business can be a slow but fruitful process; the policyholder is much happier as he doesn’t need to deal with a wrecked car.

Compare this to insurers in the US, who retain the salvage vehicle after the accident, this enables more efficient decisions on whether a car is a total loss. CPRT primarily operates as an agent for these insurers, selling vehicles on consignment for fees rather than purchasing them outright. This model significantly reduces inventory risk and aligns CPRT financial incentives with those of its sellers (insurers) because CPRT earns a percentage off the sale price.

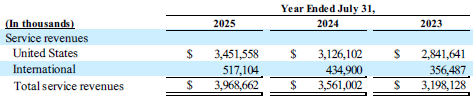

Look at the difference in Service Revenue as % of total by region:

Given the shift in Europe towards the US model, operating margins for the International region have increased to a record high of 27% (FY2025) from 18.6% (FY2024) and 17.4% (FY2023). There’s still room for improvement from 38% margins for the US region.

Conclusion

There is nothing to suggest from the past 2 quarters any permanent shift in the quality of CPRT business. Since its founding, it has experienced growth in all sorts of economic and regulatory environments.

Although the frequency of auto accidents has declined over time, the growth in severity of accidents and cost of repair has more than offsetted those declines, resulting in a steady climb in frequency of total loss. Essentially, throughout the entire history of CPRT, the total loss frequency had a monotonic upward trend (Q2 record high: 22.2%).

Lower unit volume figures are likely not a reflection of a market downturn or CPRT losing quality business to IAA. Instead, it is tied to inflation in premium rates, causing an increased number of uninsured motorists. This trend will eventually revert over time, either due to improvements in macroeconomic factors or a more robust economy.

In addition, the International region is improving margins not due to one-off favorable events, but from more than a decade of good execution in Europe. Strategic investments in its global network, technology and land will continue to fuel their long-term growth by providing unmatched auction liquidity and superior returns for sellers.

CPRT runs a solid balance sheet with zero debt and cash balance making up 11% of its market cap (if Treasuries are excess cash, it makes up 5% of market cap).

The management team also has an excellent record of shares buyback. They first reinvest into the business and only repurchase shares when undervalued. There were only 2 major repurchases:

2011: 29% of shares outstanding

2016: 12% of shares outstanding

In the recent Q2 2019, they repurchased ~3% of shares outstanding (7.6 million shares costing $365m) at PE of 20x.

The total current shares buyback authorization is 784 million shares, so far 458 million shares were repurchased.

The valuation looks simply attractive to us, despite the PE of 28x: if we assume CPRT to maintain ~27% ROIC, with discount rate 10%, the implied growth is 6-7%. We think CPRT can easily outperform this hurdle.

In other words, if CPRT can reinvest at ~40% back into the business that earns 27% ROIC, then intrinsic growth of ~10% is achievable. The historical reinvestment rate is 41%.

Putting all these factors together, we believe the market has misunderstood the fundamentals and we’ll add to our CPRT position at current prices.