CPRT: Copart (4)

Update Fiscal Year Q3 2025

On YTD basis, gross profits grew +9.4% while expenses increased +14.4%, mainly caused by facility operation expenses as CPRT continues to build out their land and facility footprint ahead of expected capacity needs (hurricane season starts June). Overall, net income grew +10.9%, but if we remove the interest income they get from investing cash at higher rates, the growth is +9.5%.

On the quarter, nothing remarkable happened other than competitor IAA (operating under RBA) gained market share. This may not be bad news as CPRT has been shifting away from lower value units, the US units average selling price (ASP) went up +2% this quarter, while IAA fell -3%.

Some indication that IAA is catering to a lower end market in their earnings call: “… we saw some buyer hesitancy in the first quarter due to the threat of tariffs.” Compared to CPRT comments: “… we have not observed any hesitation from our buyers, which we would attribute to proposed or enacted tariffs.”

There are headwinds to insurance volumes as the number of non-insured drivers has been increasing over the past 4 years:

The trends we are observing in our inventory levels reflect the cyclical impacts associated with an increasing share of non-insured motorists and varying growth trajectories amongst insurance carriers. We continue to believe that the secular trends in favor of rising total loss frequency will drive our long-term growth.

CFO Leah Stearns, Q3 2025 earnings call

CPRT continues to reinvest into the business, mentioning that they are taking more functions like titling over from insurance companies.

For the non-insurance segment, BluCar which services banks, rental and fleet partners, continued its strong trend with +14% YOY growth.

YTD operating margins decreased YOY from 38% to 36%.

Debt continues to be zero, and their cash & short-term securities pile increased from $3.4b (Jul 2024) to $4.4b (Apr 2025). This is against the fact that CPRT has been regularly purchasing rather than renting valuable land for future salvage yards.

Market Reaction

CPRT share price fell -11% immediately after this set of results. While market participants compare actual and expected numbers on a quarterly basis, we take a long-term view and remain convinced that the important value driver is how CPRT is allocating capital.

Consider that TTM free cashflows reported all time highs at $1b and CPRT has $4.4b of liquidity with zero debt against the market cap of $49.7b. We think that CPRT is operating on greater resilience and financial flexibility.

As we know this industry is in a duopoly, with IAA being the main competitor. IAA is part of a larger enterprise with net debt of $3.8b against $1.2b of EBITDA, while CPRT has no debt, $4.4b of cash and $1.3b available in their revolving credit. If you are an insurer, which company will you partner with?

Clearly, CPRT is more likely to spend what is needed when customers call for help during hurricane season. It is also more likely that CPRT survives multiple natural disasters.

Another advantage is that CPRT has a record of making large and rational share repurchases when the shares are trading below intrinsic value. The last time this happened was in 2019, 2016 and 2015. We don’t think it’s likely that management will repurchase at current prices as there are more useful places to deploy capital internally. Capital returned to shareholders doesn’t contribute to compounding intrinsic value, only capital reinvested into the business will produce value.

This large cash position relative to the market cap can be viewed as an optionality that should be valuable for shareholders if opportunities arise.

Hurricane Season

The US experiences hurricane season every year between June and November. This impacts CPRT expenses which typically ramps up in FY Q4 and may significantly increase in Q1 depending on the severity of hurricanes.

So the cash balance is crucial to ensure that CPRT can deliver its services in an extremely bad season. Although natural disasters are unpredictable from year to year, it is inevitable that they will happen some time in the future. This means that it is certain that CPRT needs land for many thousands of damaged vehicles.

In Jan 2025, CPRT purchased 835 acres in Charlotte County for $13.3m from a previous ranch landowner. In the latest earnings call, management said that the company has the physical land to handle a storm more than 3x the size of the largest Florida storms on record in CPRT’s history.

Capital Allocation

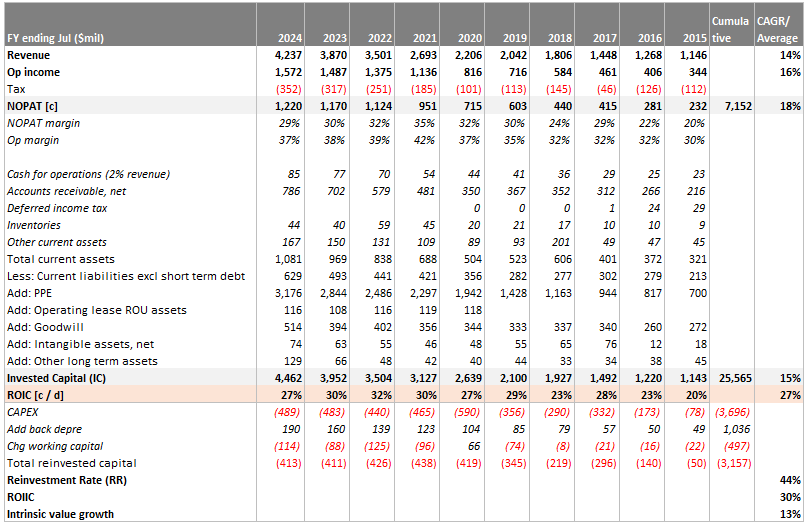

We estimate that for the past 10 years, CPRT has compounded intrinsic value at 13%.

A few things to note:

The largest portion of capital used is for buying land and equipment. This is fundamental to the business operations. CPRT owns ~90% of land, the remainder is leased. This contrasts with IAA leasing strategy which on paper produces higher ROCE, but they are beholden to landowners when renewing contracts.

Share repurchases are infrequent but when they occur it is quite large. Debt has been fully repaid. These activities took up 38% of capital deployed, effectively returning to debt/equity holders and doesn’t contribute to intrinsic value.

M&A is sparse. 2017: National Powersport Auctions (US), 2022: Hills Motors (UK). Given CPRT dominant share in the US and its preference to organic growth, we expect little M&A activity going forward.

We don’t see any impairment to the business quality or management’s ability to allocate capital in the future.

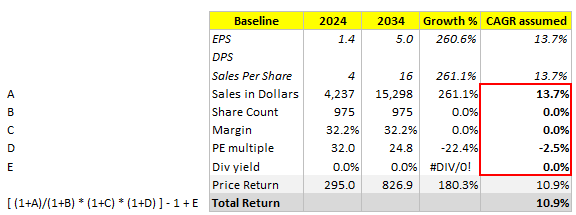

If we have these parameters, we can find the implied growth:

IRR hurdle rate = 12.5%

PE = 34

ROIC = 27%

The implied growth = 11%. We can then breakdown the source of returns by factors:

For next 10 years, if we cater for PE compression to 25 and keeping all else constant, we will need ~14% sales growth to match the implied growth of 11%. The past 5 and 10 years sales CAGR at 14%.

In short, if we buy at today’s price we are assuming the business will perform equally well for the next decade versus the prior decade.

Pay Up for Quality

We already have an existing position at cost price $52.8/share. The only thing stopping us from allocating more toward CPRT is the lack of margin of safety in the price. But we also know that the error of omission is costly especially when we have a good understanding of the business economics. In other words, we have to pay up for quality.

We will continue to allocate more into this position at a conservative pace.

Hi nice to see you on Substack. I gather you’re still migrating your articles across. I recall there being more recent updates on CPRT. At current price, I think CPRT is undervalued and remains well placed to navigate headwinds of under insurance.