COST: Costco (3)

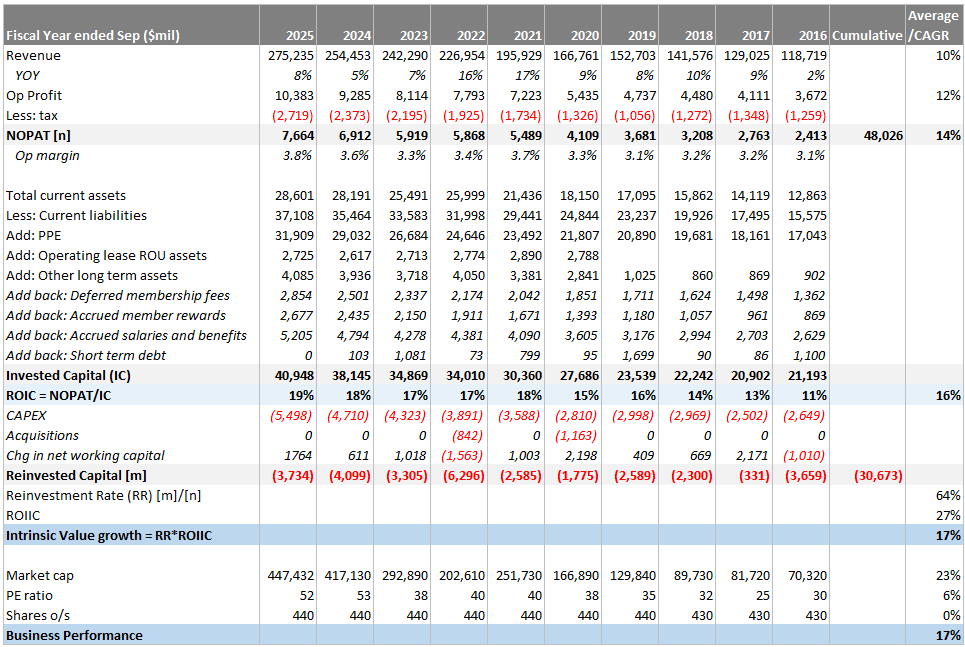

ROIC Increasing Trend

We have wrote about COST in the past:

COST is a company we have admired for years from afar but couldn’t get past the expensive valuation. Recently, there was a data point that we noticed, and realized that this probably was the reason why the market puts a premium on this retailer.

Take a look at the increasing trend of ROIC from 2017 onwards:

From 2016—2025 the market value compounded at +23%, helped by a significant PE multiple expansion of +6% CAGR. Shares outstanding didn’t change much, so the underlying business performance was +17% CAGR.

Ignoring the effects of multiples expansion, the core business managed to improve ROIC despite being a well-understood matured retailer.

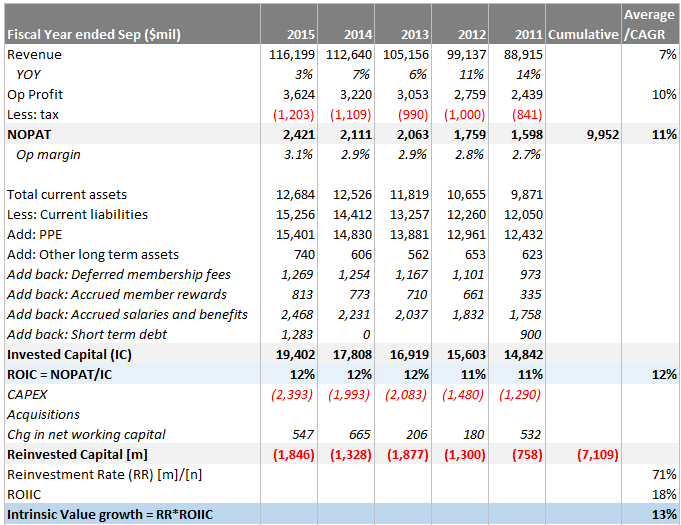

If we go back 5 more years, the ROIC has indeed deviated from a stable 12% to 19% in 2025.

What Happened in 2017

COST started their e-commerce operations in 2017, they were late to the e-commerce party as their focus has always been in-store experience. There’s 2 reasons why e-commerce is not particularly suitable for COST model:

COST only has 634 stores in the US. Compared to Walmart’s ~5200 stores (including Sam’s Club) and Target’s more than 2000 stores. Delivery speed and inventory management would be a challenge.

COST sells in bulk and holds only ~4000 SKUs. Many of COST products are part of their own private label (Kirkland) which was introduced in 1995 to replace the diverse private labels that COST had developed up to that point. On the contrary, e-commerce is traditionally a sales channel that boasts variety and the ability to buy in small packages.

It might not seem at first glance like there’s much to COST distribution network, as they give the appearance that they offer their membership direct access to it through their wholesale warehouses. And indeed, in some cases suppliers send their goods directly to their warehouses, eliminating the intermediaries that are typically part of a retailer’s supply chain.

However, digging deeper into the logistics, we realize that it’s incredibly efficient. And if you go to costco.com, the products available for e-commerce are mostly big ticket items (TV, laptops, treadmills, massage chairs, coffee machine, furniture, sofa…). Singular items like jackets are available, but they entice you with savings if you mix & match qualifying items, turning it into a bulk purchase.

COST offers 2-day delivery for non-perishable items and same-day delivery for groceries. To save more, you can order online and pick-up at a Costco warehouse.

To further explain how efficiency gains translate into higher ROIC, we need to examine Costco Logistics.

Costco Logistics

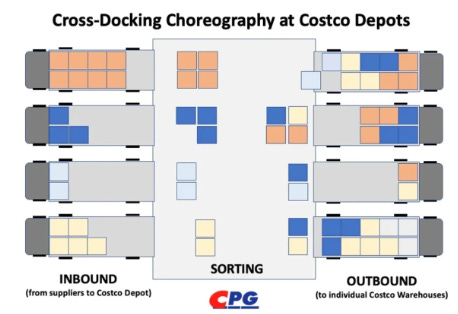

Regional Depots

COST maintains a network of 24 Regional Depots which are pure cross-docking facilities. Full pallets are offloaded, sorted, and sent to warehouses.

The receiving and processing of goods primarily goes through the depots before arriving at warehouses. Kirkland private label works with alot of manufacturers and this centralized distribution network is advantageous.

These depots can be either “dry” for non-perishables or “chill” for perishables. COST operates 12 chill depots in the US, so the split is 50:50 between dry and chill.

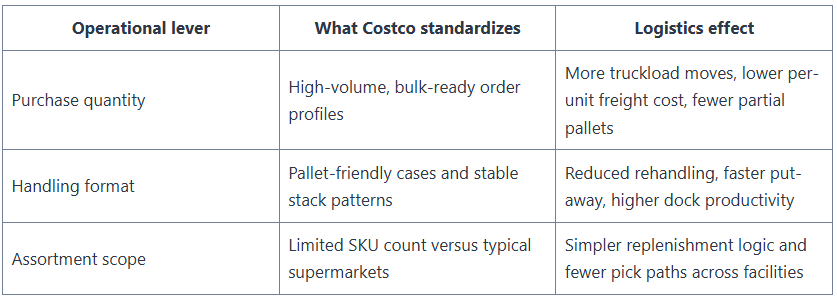

For brands, access to COST’s members traffic can deliver rapid turnover, but it comes with tighter inbound discipline. The COST supply chain relies on on-time appointments, compliant labels, and bulk-ready quantities that flow cleanly across docks. Missed requirements can trigger delays that ripple into availability at the warehouse level.

Many suppliers use third-party providers to meet these standards at scale. This includes pallet builds, carton markings, and routing guide compliance before freight reaches the network.

“No Touch” Policy

“No Touch” means products remain on pallets throughout their time on the floor. Instead of breaking down loads into small packs, employees sort and move full pallets. This approach reduces handling steps, minimizes repacking, and decreases congestion in active aisles.

This policy also enhances receiving standards in Costco Logistics. Pallet integrity, consistent labels, and stable stacking are critical because the pallet is the work unit. When loads arrive ready for quick placement, the warehouse avoids slow case-by-case stocking.

Retail & Distribution Points

Many sites serve as both selling floors and high-velocity storage areas. This reduces the need for large backrooms and separate retail staging areas. The sales floor displays inventory in plain sight, shortening restock travel distances.

This layout supports faster replenishment cycles within Costco Logistics. Products can move from receiving to racking or directly to the floor without extra transfers. Less internal movement helps control labour costs and keeps docks available for the next appointment.

Vertical Integration

COST only entered into e-commerce space in October 2017 when they launched CostcoGrocery. They partnered with Instacart and Uber for same-day deliveries.

Then in March 2020, COST acquired Innovel Solutions for $1b to improve last-mile capacity. COST has been a customer of Innovel since 2015.

Innovel has for decades provided Sears and, more recently, third parties with “final mile” delivery, complete installation and white glove capabilities for “big and bulky” products across the US and Puerto Rico. They employ over 1500 people and operate 11 distribution/fulfillment centers and over 100 final-mile cross-dock centers, with over 15 million sqft of warehouse space.

Products served through Innovel include major appliances, furniture, mattresses, televisions, grills, patio, fitness equipment and wine cellars.

The rationale for vertically integrating the “big and bulky” stack is simple:

“Big and bulky” items pose unique challenges different from in-store replenishment. These items require special handling and equipment like lifts, more crew members, and scheduled appointments.

Cost per stop and risk of service issues are higher. Reverse logistics also becomes more complex with heavy items. Carriers must manage pickup timing, packaging condition, and safe loading. For COST, this means more touchpoints, claims risk, and stricter tracking discipline.

As a result of this acquisition, COST is now delivering ~85% of its LTL (less-than-truckload) shipment for US e-commerce through its own Costco Logistics. LTL is cost effective since COST already palletized their inventory. In fiscal year Q1 2025, Costco Logistics completed almost 1 million deliveries! They have also shortened their delivery time from 2 weeks to 4 days.

All the above strategies combine to result in high inventory turnover (2017: 11.5x, 2025: 13.2x). It’s a combination of structural choices that drive volume through a streamlined system. This model is born out of necessity because COST manages its inventory with a narrow range of SKU, hence high inventory turnover is a must. This is the reason why COST has much higher ROIC than competitors.

With the introduction of e-commerce, the model has evolved through the Innovel acquisition, allowing for large orders and shorter delivery time. The whole system is a delicate balance between in-store demand and e-commerce needs.

Advertising

You might argue that e-commerce is not really capital-light, it requires trucks and labour which scale with more volume, and last-mile delivery is notoriously expensive. This can’t be the sole contributor of better ROIC?

Yes, you’re right. So, guess what is often paired with e-commerce platforms?

Answer: advertising revenues.

COST once again is the late comer, but does the correct thing by focusing on merchants, instead of monetization.

Ads generates high margins, that’s why it is attractive. But it creates a dangerous temptation to chase advertising profit at the expense of merchant outcomes.

COST top priority is sales velocity, although it already has the highest inventory turnover in the industry, but merchants will always wish it to be faster. So every technology choice has to serve sales velocity, or merchants won't support it.

On 10 Jan 2026, there was a retail media network conference in New York. Mark Williamson, AVP of Costco retail media, gave a presentation of their approach.

He did what most retailers feared… revealing their entire retail media tech stack.

This sent a clear signal: COST is transparent about their tech stack because they want merchants to benefit from it. Ads are in service to accelerate turnover!

COST understood that merchants who control supplier relationships need proof that advertising accelerates their goals, and advertisers need to understand how the system works well enough to trust it.

COST advertising infrastructure divides into 4 layers, each designed around a specific function in service of sales velocity:

Unified Data Foundation

Runs on a private Google Cloud, consolidating all member-identified transaction data.

MetaRouter and LiveRamp handle identity resolution.

Transcend manages privacy.

GrowthLoop uses AI to segment members and propose customer journeys.

Everything flows from membership data because without members there's no one to sell anything to.

Activation Channels

Onsite: Uses a new ad server (not yet announced) partnered with Criteo, supporting self-serve and automated bidding for native, display, and product ads on website and app.

Offsite: Connects first-party data to DSP (Demand-Side Platform) like The Trade Desk, Google, Yahoo! DSP, Epsilon, and StackAdapt extending audience targeting across the internet and social platforms.

In Real Life: Includes a pilot for fuel ads at gas pumps, warehouse TV, digital out-of-home (dynamic digital screen media in public spaces), and traditional print (Costco Connection magazine).

Measurement Layer

Ad campaigns data analysis by Habu data clean room (run by Google) connects digital ad exposure to both online and in-store transaction data.

Operations

Workflows are designed to be self-serve and automated.

…the idea here is that whatever we generate in terms of revenue is in service to the core model.

It's not a bottom line profitability play.

It is a means of reinvesting back in member value […] we take the money that we make, give it back to the merchants, and the merchants go do what they do best which is lower prices.

Mark Williamson, AVP Retail Media

No Vertical Integration

COST prioritizes speed to market over proprietary tech, that's why it chose to partner with vendors.

In contrast, Amazon and Walmart built their advertising ecosystems in-house. They’re very successful, taking ~89% of retail media spend with their vertically integrated platforms.

They need vertical integration because their marketplace supports a huge number of SKUs and 3P sellers. When buying media on these networks, everything is seamless, they are full package: front-end, ads server, and reporting system.

COST operates a very different model with low SKUs and merchants, we don’t think there’s a huge benefit with vertical integration (perhaps COST could be less beholden to vendor pricing).

The dependence on vendors could be a safeguard against the rise of AI-shopping, where people ask AI to shop and directly buy from the retailer. If this situation is widespread, then customer's behaviour is not captured within the retail media model. This means ads become less effective, and retailers lose this segment. If disrupted, those who vertically integrated might hold redundant assets, whereas those who partnered with vendors can just walk away.

Of course, this is difficult to predict. Disruption might not happen? Retailers might be able to pivot?

Financials

Let’s see how these developments translate into their financials.

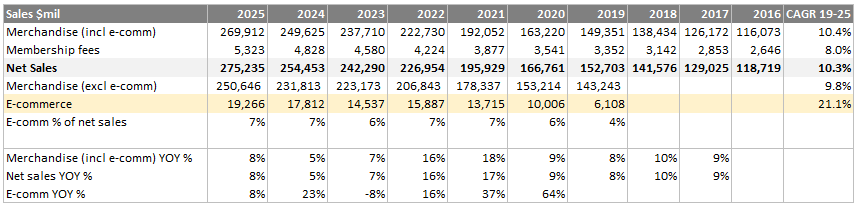

COST doesn’t explicitly report e-commerce revenues or margins, but we can infer the revenues since they mention the proportion:

Surprise! E-commerce grew very quickly since 2019 (+21% CAGR). If we look at the cumulative dollar sales growth, e-commerce contributed 11%, very significant considering it’s less than 10 years old:

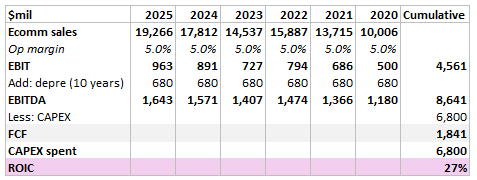

The amazing thing is e-commerce growth actually did not require much incremental investments. Consider 2020 to 2025:

Increase in PPE +$10b.

Store count increased +128 (from 795 to 923) worldwide.

Assuming a new store incurs $25m CAPEX, then the remaining $6.8b was allocated to logistics/e-commerce.

If we give e-commerce 5% operating margins, the ROIC is turns out to be quite healthy:

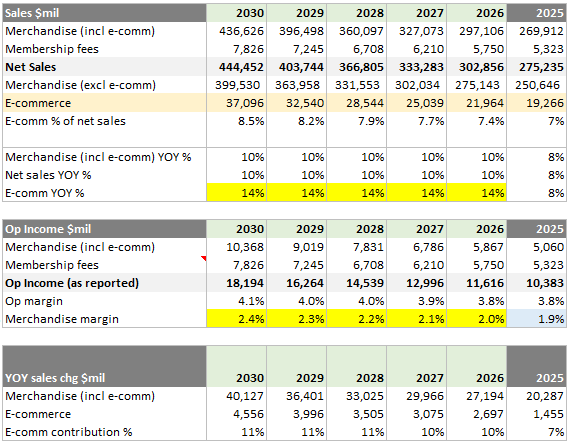

Logically, it’s leveraging on Costco Logistics which already is very efficient. As a result, the merchandise segment’s operating margins doubled from 0.9% (2016) to 1.9% (2025):

Valuation

All the above developments are likely reasons why COST trades at a premium of 44x free cashflows.

Let’s model out the next 5 years:

Higher margin e-commerce grows at +14%.

E-commerce contributes 11% of sales dollar growth.

Merchandise op margins improve gradually to 2.4%.

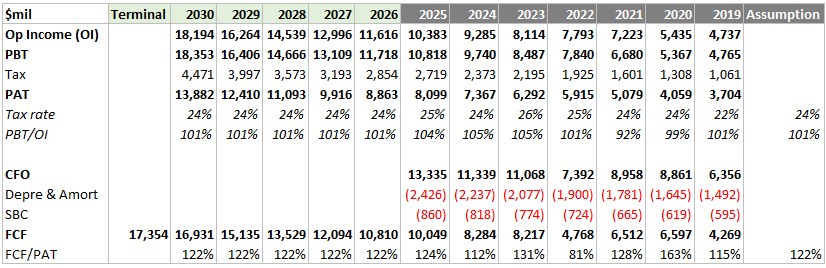

We can estimate the FCF with terminal growth +2.5%:

Do a reverse DCF to solve for current $447b market cap, we need the discount rate to be 7% (implied FCF exit multiple = 22x).

Conclusion

We don’t think this insight is new, since the market had recognized it years ahead of us. It’s a boat that we missed. This exercise revealed some valuable lessons on the economics of COST.

At a hurdle rate of 7%, this is not attractive enough considering other opportunities like CPRT, CSU, and PGR.