COST: Costco (2)

Expounding the Virtues of Costco

We wrote extensively about the history of COST in a previous article. So this second article will serve to further expound the wonderful business characteristics of COST, after our visit to a COST warehouse in Japan.

Introduction

COST operates membership warehouses in North America, the United Kingdom, Mexico, Japan, Australia, Spain, Taiwan and Korea.

It operates 861 warehouses with a huge average size of 147,000 square feet. They operate on a seven-day, 70-hour week.

591 (68%) stores are in the US, 107 in Canada and 163 in the rest of the world. Japan has 33 stores. In terms of ownership, 677 of the stores are owned by the company while 184 are leased.

They have a relatively small range of goods about 4,000 SKUs versus ~140,000 at Walmart, and generally sell items in bulk.

A large part of their profit (70%) is made from their membership income which, by definition, is almost 100% gross margin – this ensures excellent revenue predictability and enables them to cut prices on their core offering to generate more membership income.

Traditional retailing is a game of thin margins and high fixed costs.

Fun fact: The shopping day that follows the Thanksgiving Holiday in November in the US is called Black Friday. This is because every year, retailers do not break into the black until around that day. Up to that point, they are paying fixed costs and making losses. After that, they hope for a good Christmas season, where they will make the bulk of their profits (if any) for that year.

COST is different, as its membership fee ensures that it is profitable on day one. COST can accurately predict the total number of members for the coming year and therefore, the resulting total membership income.

The membership income has almost 100% gross margin. The operating cost is tiny compared to revenues at scale. COST offers the highest quality goods at low margins to attract more of the profitable membership fees.

Offering members low prices on a limited selection of nationally-branded and private-label products in a wide range of categories will produce high sales volumes and rapid inventory turnover. When combined with the operating efficiencies achieved by volume purchasing, efficient distribution and reduced handling of merchandise in no-frills, self-service warehouse facilities, these volumes and turnover enable COST to operate profitably at significantly lower gross margins than most other retailers.

COST often sells inventory before they are required to pay for it, even while taking advantage of early payment discounts. Their depots receive large shipments from suppliers and they quickly ship these goods to warehouses. This process creates freight volume and handling efficiencies, lowering costs associated with traditional distribution channels.

Floor plans are designed for cheap and efficient use of selling space, the handling of merchandise, and the control of inventory. Because shoppers are attracted principally by the quality of merchandise and low prices, COST warehouses are not fancy.

By strictly controlling the entrances and exits and using a membership format, COST manages to achieve low 0.1% to 0.2% inventory losses, while typical retailers have ~1.6%. (source: CFO Galanti 3Q 2023 earnings call)

Virtue #1: Cheap but Quality Products in Warehouse Format

COST sells petrol by the side of their warehouse at a very competitive price. It was JPY162 per litre in April when we visited, compared to other common gas stations (ENEOS, Cosmo) they were selling at JPY170. By the way, in 2023, petrol sales accounted for 13% of total.

At the entrance is large desk where new members can sign up. We walk in through a narrow entrance where they check membership, after picking up one of the giant trollies from outside.

The first area is full of large televisions. This is followed by casual clothings which are piled up and there are no assistants or fitting rooms.

There is a freezer room for fruits and vegetables and special sections for meat and fish.

All kinds of other bulky items are stacked on pallets to the very high roof. In every category, the choice is much more limited than a rival supermarket (eg. AEON) but the prices are very attractive. In some categories, the only offering is the in-house Kirkland brand.

There’s no selling 1 bottle of ketchup or 1 box of green tea. They are sold in cases of 6 or 12. The whole idea is to buy in bulk to reap savings.

Once we fill the trolley, we lined up to pay at the cashiers, which are spread out sufficiently to allow customers to navigate the wide trolley through.

Behind the cashiers is a food court that offers cheap fast food, including the famous $1.50 hotdog pepsi combo and large pizza:

At the cashier, our membership card is checked. After payment, we walked along a narrow corridor where they advertise large bulky items such as windows, doors, garden sheds etc. A few items we saw on our last visit was no longer there, but there are always new items. This makes the shopping experience something of a treasure hunt.

At the narrow exit, a staff checks our shopping against the receipt. They check for theft, including the possibility that a cashier may know the customer and not scan all items.

Virtue #2: The Membership Program

The most important aspect of COST business model is the membership program. An active annual membership is required to shop at COST warehouses. Members can bring up to two non-members as guests, but only the member is allowed to purchase merchandise.

The membership format is an integral part of the business and has a significant effect on profitability. This format is designed to reinforce member loyalty and provide continuing fee revenue. Profitability is materially influenced by the extent to which COST achieves growth in their membership base, increase the penetration of their Executive members, and sustain high renewal rates.

COST provides a money-back guarantee for all memberships but does not provide day passes, trial periods, or other promotions. There is a perception of exclusivity. Membership is not hard to obtain but excludes the casual shopper who just wants a few items and perhaps does not own a car.

Memberships also filter away potential shoplifters. A customer who is willing to pay $60 or $120 for a membership is unlikely to steal. COST customer base is skewed toward higher income customers who have discretionary income sufficient to buy in bulk. Customers facing cashflow problems are unlikely to be willing to pay $60 for a membership or to have enough income to purchase in bulk.

Psychologically, a member is likely to feel driven to justify the membership fee and will be more likely to choose to shop at COST rather than other retailers. Renewal rates are very high and stable, in 2023 the renewal rate was 92.7% in North America and slightly less at 90.4% in other countries.

COST exercises restraint when it comes to increasing membership fees. The last increase was in 2017 when the basic membership rose from $55 to $60 in the US. In the past, it increased by $5 in 2006 and 2012. So far in 2024, fees have not increased yet.

COST has strict rules in place when it comes to sharing a membership. However, one free household card is available to any other person over the age of 18 who lives at the same address as the paying member.

Members are allowed to bring up to two guests during visits to a warehouse. When non-members are exposed to COST, there is a good chance some of them will eventually become paying members.

The membership is very good value: it would take ~$500 worth of shopping to save the cost of the $60 membership fee. If we take COST net sales of $242b and divide by 75m paying members, the average member spent $3,200. Members are clearly enjoying a compelling value proposition in exchange for the membership fee.

Virtue #3: Shopping Frequency

Having cheap petrol, food, and products encourages customers to visit often. People who drove to a warehouse to fill up petrol might as well do some shopping. The “treasure hunt” atmosphere also encourages frequent visits.

One of the most exciting things about shopping in COST warehouses is that you never know the kind of incredible deals you’ll find from one visit to the next. Members will visit often to get exclusive deals. And because COST rotates out and introduces new merchandise all the time, it encourages members to purchase items that interest them sooner rather than later to avoid missing out.

Virtue #4: Inventory Management

COST offers a limited number of SKUs compared with other large retailers. This simplifies the process of sourcing, distributing, and managing inventory. Products are offered in bulk quantities, which provides efficiencies in terms of packaging and warehouse inventory management, plus it reduces the risk of shoplifting.

Cash conversion cycle for COST is 3 days, half of Walmart’s 6 days. The quick turnover of inventory explains why COST has a higher ROE even though gross margin is lower.

COST rapid inventory turnover means less inventory relative to sales volume, requiring less working capital to support the business. COST payment terms with suppliers and rapid inventory turnover combined to ensure it sells merchandise before suppliers must be paid. Suppliers rather than shareholders finance a large portion of the working capital requirements!

Virtue #5: Economies of Scale

The limited selection within each product category makes it possible to acquire large amounts of each SKU, increasing COST’s negotiating leverage with suppliers. This brings down prices and leads to attractive payment terms. COST turns its inventory over 12 times per year and suppliers are effectively financing COST’s inventory with payables typically exceeding the value of inventory. For example, at the end of May 2024, payables were $18.8b versus inventories of $17.4b.

Virtue #6: High Productivity

Warehouses have few amenities and have simple fixtures. Inventories can be moved directly from trucks to the selling floor. These factors allow COST to achieve high employee productivity despite paying above-average wages and retaining employees for the long term.

Virtue #7: Paying Employees Well

COST’s management believes in paying higher than average wages and generous benefits in exchange for hard work. This is in sharp contrast with many retailers that tend to pay low wages. The higher labour costs are more than offset by better productivity that is driven by low levels of employee turnover.

COST has a long-standing policy of promoting employees from within the company and offering not just a job but a career path. They limit part-time employees to less than 50%. It has estimated that turnover is typically very low (5%) for employees who have been on the job for at least a year.

The new CEO, Ron Vachris, has been working for COST for 40 continuous years, starting out as a forklift operator.

At the end of 2023, COST employed 316,000 employees worldwide. Their progressive HR policies and higher remuneration results in a higher than average retention rate: 90% of employees have been working for at least one year.

Virtue #8: Scaled Economies Shared

Due to scale and buying power, COST could have extracted a higher margin. Rather than doing this, COST shares a large part of it with customers, promising that the mark-up will not be more than 14% (for Kirkland label 15%). Typical retail mark-up is literally 100%. This drives trust and loyalty among members, which results in high membership renewal rates.

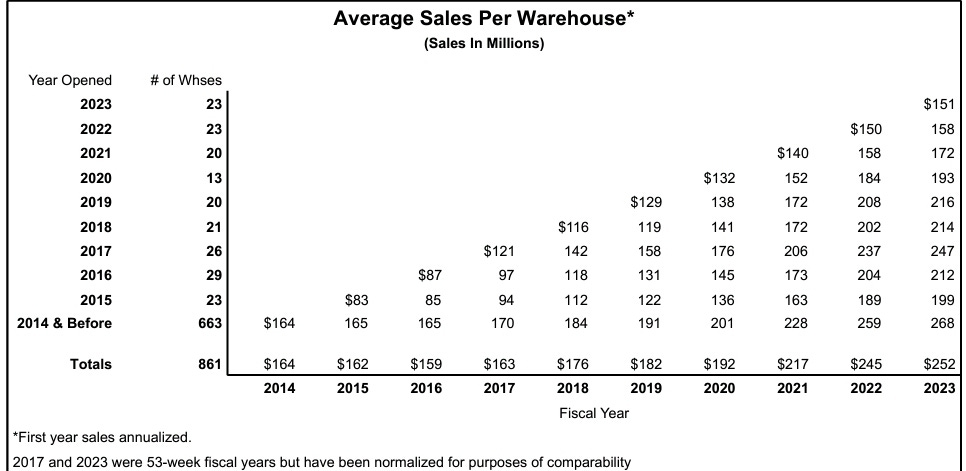

Virtue #9: Strong Same Store Sales Growth

In 2023, same store sales growth was 4.9%. Every cohort of stores in each year recorded growth, even those built before year 2014 had 3.5% growth.

This means that building a new store has historically yielded lucrative long-term benefits, since the large one-time CAPEX is usually in the first year.

Valuation

COST culture demands that management act as a fiduciary for members and drive down prices as far as possible, consistent with earning a reasonable return. Growth is made possible not through gross margin expansion but through operating efficiencies and new warehouses.

We run a reverse DCF with the following assumptions to justify today’s market cap of $376b:

10% free cashflow growth for next 10 years.

2.5% terminal growth.

Discount rate 6%.

Analysts’ consensus expectations for EPS in 2024, 2025 and 2026 are at $16.1, $17.7 and $19.4 respectively. This means at the current share price of $848, the forward PE ratios are 48x (2025) and 44x (2026).

Although 3 years ago, COST was trading at a forward PE of 40x, it still more than doubled in returns. However, at current prices we will only be implicitly demanding a 6% return under the reverse DCF assumptions; we don’t feel this is a sufficient return on capital.