BN: Brookfield Corporation

History

The origin of BN traces back to São Paulo Tramway, Light and Power Company Limited, founded in Brazil in 1899.

During those times, streetcars would stop by dusk because there was no infrastructure to power the city up with electricity.

William Mackenzie, a Canadian railway entrepreneur, partnered with Frederick Stark Pearson, an American electrical engineer. They saw the problem in São Paulo as an opportunity.

São Paulo Tramway, Light and Power was then created and operated the transportation system of Brazil’s economic miracle. By May 1900, their first electric streetcar glided down São Paulo’s streets, with the state president himself ceremonially starting the dynamo.

São Paulo’s population had exploded from 65,000 to 250,000 in a single decade. Coffee exports were minting millionaires faster than the city could build mansions for them. Every factory needed power. Every street needed light. Every neighborhood needed transit.

By 1912, reorganised as Brazilian Traction, Light and Power Company (BTLP), they became something unprecedented: a foreign corporation so essential to Brazil that it employed 50,000 people and generated two-thirds of the nation’s electricity. Back in Canada, only the Canadian Pacific Railway was bigger. The most important corporate culture within modern BN was built; patient capital building essential services, not quick profits but generational wealth through things people cannot live without.

The business grew comfortably for nearly 50 years.

Then in 1959, enter brothers Edward and Peter Bronfman. Their Montreal cousins had pushed them out of the family’s Seagram liquor empire, leaving them with CAD$15m. Many people saw BTLP as a boring utility facing nationalisation threats, but the Bronfman brothers smelled opportunity.

BTLP continued to operate in Brazil following the establishment of a military dictatorship in 1964. In 1966, it changed its name to the Brazilian Light and Power Company Limited, and in 1969, changed name again to Brascan.

In 1979, the company was forced by the dictatorship to sell its main asset, Light S.A., to the country’s national utility, Eletrobras. Consequently, Brascan became mostly devoid of assets but had an abundance of cash.

In 1978, the Bronfman brothers bought in an accountant, Jack Cockwell, and started buying shares of Brascan for control.

Through pyramidal ownership, they discovered they could command many companies with minimal cash. They issued different classes of shares, super-voting for insiders, regular for the public, and used the public’s own money to maintain control. By the 1980s, they had built an empire of 500 companies worth CAD$100b.

At the peak, their empire employed 100,000 Canadians and represented 15% of the Toronto Stock Exchange total market value!

But corporate pyramids are inherently unstable.

The structure demanded that cash flow upward, each subsidiary paying dividends to its parent, all the way to the Bronfmans at the top. It worked brilliantly when times were good. The 1990s recession revealed the flaw: when subsidiaries can’t pay, the whole thing collapses.

By 1993, Edper Investments, the Bronfman’s master company, had lost 90% of its value. Bramalea, their property arm, filed for bankruptcy with CAD$3.8b of debt.

The complex financial engineering that stood for 30 years fell quickly. The Bronfman family exited with nothing.

But the company didn’t die. Jack Cockwell, the architect of the pyramid, stayed behind to dismantle what he had built. For 5 years, he unwound cross-ownerships, sold non-core assets and negotiated with creditors.

This was when the current CEO, Bruce Flatt, entered the picture.

Flatt had joined in 1990 as a young accountant, watching the empire crumble from the inside. However, he saw valuable assets buried under all that financial engineering.

For example, when Olympia & York properties collapsed, Flatt bought their crown jewels for pennies on the dollar.

Bruce Flatt became the CEO in 2002 and renamed the company Brookfield Asset Management (BAM) in 2005, transforming the colonial utility to a global infrastructure manager.

In 2022, BAM was spun off and structured to be a non-taxable event for original BAM shareholders. Original BAM was renamed as BN, and shareholders continued to hold their original number of shares as new BN shares. In addition, they received 1 share of the new BAM for each 4 shares of the original BAM. Now, BN owns 73% of BAM.

Today, BN is an alternative asset manager with over $1t AUM, solving a problem that pension funds, sovereign wealth funds, insurance companies have: they need steady returns for decades to match liabilities.

Business Model

Through the ownership and operations of datacenters, renewable energy, shipping ports, real estate… BN makes money by being an infrastructure middleman.

Management fees

Investors pay BN 1.5% to 2% annually just to oversee their money, whether investments perform well or poorly.

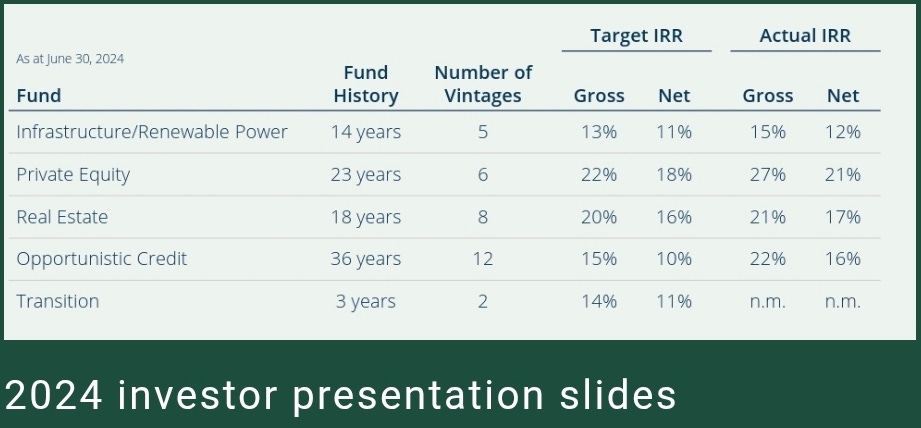

Their funds actually perform quite well:

Carried interest

Performance bonus, typically 20% of any profits above an 8% annual return.

Principal investments

Cashflows from owning assets using their own money and client’s money.

Typical private equity have 5 to 10-year lifespans, but since BN has their own capital, they can compound assets for longer.

Wealth solutions

Insurance companies need to invest conservatively to meet regulatory requirements. But “conservative” doesn’t mean “low return”.

Most insurers buy government bonds paying 4%. As an alternative, BN invests insurance premiums into their own infrastructure deals yielding 8%. It is still conservative because it’s a regulated utility but twice as profitable.

The Flywheel

The economic flywheel happens when these revenue streams interact.

The management fee business funds the infrastructure to find and execute deals. Successful principal investments prove the model, attracting more client capital. The insurance float provides permanent funding for longer-term opportunities.

Each piece makes the others stronger.

Operational Expertise

This is akin to private equity (PE) firms. BN expertise is in transforming risky assets into stable ones.

They’d buy a struggling company, fix the operations and make it a better business. A few years later, that same business produces a more stable cashflow and commands a higher multiple.

But BN has a further advantage…

BN has operating expertise in many assets like airports, shipping ports, utilities, data infrastructure, and residential construction.

It has spent 30 years building these capabilities. Not just the technical knowledge, but the relationships with regulators (control pricing), labour unions, governments (control concessions), and manufacturers (control supply).

We can think about the flow this way:

1. Pension funds have capital and time but no expertise.

2. Governments have expertise and assets but need capital.

3. PE firms have capital and expertise but short investment time frames.

BN has all three elements: capital, expertise, and time horizon. They then charge clients for access to their complete package.

Opportunistic Buyer

Our goal is to invest capital for our clients in opportunities which have reasonable returns in a downside scenario (6% to 8% on equity), have the potential to generate good returns under most scenarios (12% to 15%), and in the upside cases will generate excellent returns (20% plus). These latter scenarios usually require us to be able to buy right, execute well, and reallocate capital wisely over time.

Bruce Flatt, CEO

Bruce Flatt has long emphasized a disciplined counter-cyclical approach. When markets panic, BN steps in often buying high-quality assets at a discount.

Example 1: One Liberty Plaza

BN bought it from a bankrupt developer in 2001 for $432m. By 2017, when it sold half the building to Blackstone, the property was valued at $1.5b (more than triple the original price). Then came the recent interest rate hikes, causing the property value to fall. Rather than retreat, BN bought back Blackstone’s stake in 2023 at a heavily discounted $1b valuation.

Example 2: Privatizing Brookfield Property Partners

In 2021, when COVID caused commercial real estate to fall, BN offered $5.9b to buy out the portion that they don’t own.

Example 3: Brookfield Place

This is actually the shopping mall linked to the World Trade Center in Manhattan. Post 9/11 terrorist attack, BN undertook extensive renovations, and the complex was rebuilt and reopened with new retail and dining spaces.

New York’s Grand Winter Garden Atrium reopened on September 12, 2002 in a grand ceremony attended by President George Bush at the time. It was a major step in the rebuilding of the World Trade Center area and a proud moment in American history.

Critical Infrastructure

Example 1: Brazil

BN owns assets are integral to Brazil’s energy and water supply, and their scale, long-term contracts, and strategic importance make them challenging for competitors to replicate.

These include 3,900km of natural gas pipelines, which are part of its regulated transmission business. BN also owns 2,900km of operational transmission lines in Brazil, further solidifying its presence in the region’s energy infrastructure.

BN has a significant water and wastewater operation in Brazil, with concession agreements that have an average remaining term of 22 years. These agreements involve water treatment services, maintenance, and improvements to distribution systems, making them critical infrastructure.

Example 2: Colonial Enterprises

BN acquired Colonial Enterprises, the holding company of the 5,500-mile FERC-regulated refined-product pipeline system in the US.

Example 3: Clean Energy

It has a huge portfolio of renewable energy assets with a 200GW global development pipeline, including solar, wind, and hydroelectric power. Approximately 40% of this pipeline is in North America, 24% in Europe, and 12% in Australia, with the remainder in Asia Pacific and South America.

Example 4: Oaktree Capital

Yes, this is the credit investment firm co-founded by Howard Marks. BN acquired a majority stake in Oaktree back in 2019, creating a powerful partnership between two highly respected names in asset management.

Oaktree’s strength in credit, particularly distressed debt and high-yield bonds, perfectly complements BN expertise in infrastructure, real estate, renewables, and private equity. The result is a broader, more resilient platform with even greater appeal to institutional investors.

The Oaktree merger strengthens BN competitive position against other major alternative asset managers like Blackstone, KKR, and particularly Apollo which has always been heavily credit focused.

Brookfield Asset Management

BN owns a controlling stake in Brookfield Asset Management (BAM), one of the world’s most successful alternative investment managers. This business has grown from managing just $3b in the early 2000s to over $1t in fee-bearing capital (FBC) today.

BN spun out a 25% minority interest in BAM at the end of 2022, listing it on both the TSX and NASDAQ. This separation gave investors two distinct choices: own BAM directly for a pure-play exposure to asset management, or hold onto BN for a piece of BAM plus a much broader mix of assets.

Since asset managers don’t need much PPE or working capital to do business, BAM can pay out ~90% of its annual earnings in dividends.

While BAM earns steady management fees, BN’s balance sheet houses equity investments across its infrastructure, real estate, and PE businesses, generating strong long-term contracted cash flows and inflation indexation.

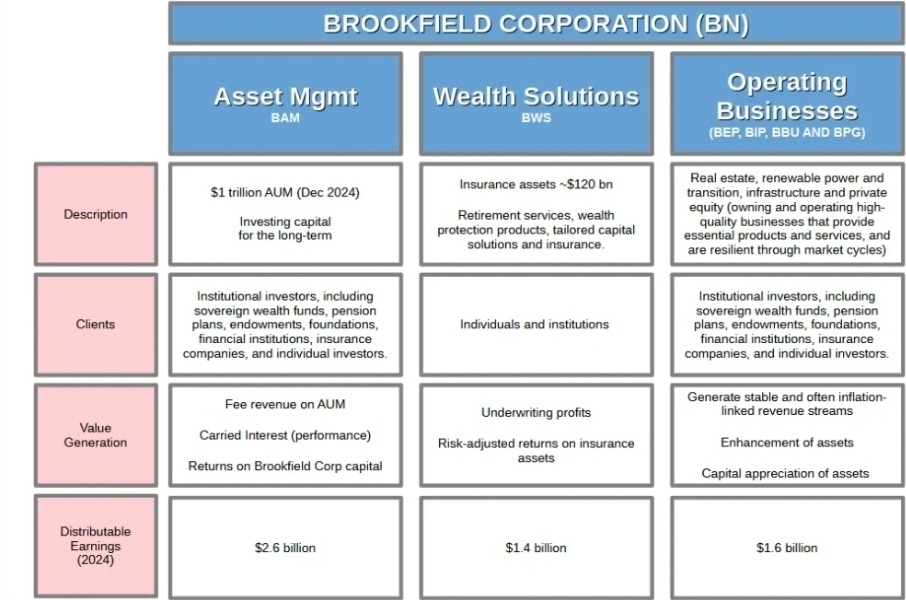

Business Segments

BN financials can be split into:

Ownership stake of BAM.

Carried interest.

Brookfield Business Partners (BBU): PE arm.

Brookfield Infrastructure Partners (BIP): Transport, midstream, data infrastructure.

Brookfield Renewable Partners (BEP): Clean energy projects.

Brookfield Property Group (BPG): Real estate.

Brookfield Wealth Solutions (BWS): Long-dated annuities and retirement solutions.

Table summary:

Unrealized Carried Interest

Currently, BN market value is $99.8b and BAM is $94.2b.

BN 73% ownership of BAM is $68.8b, meaning that only $31b is attributable to non-BAM segments.

That feels remarkably low when we consider that BAM (Asset Management) generated just 36% of Distributable Earnings Before Realization (DEBR) in FY2024:

Direct Investments (19% DEBR) is the sum of the cash distributions it receives from its General Partner’s (GP) interest in its private funds. Think of this as dividends received by its ownership stake in the funds. This metric likely understates the value of these positions as it does not capture the compounding of the value of the GP interests, nor the full amount of earnings that are supporting these distributions.

Moreover, forecast growth over the next five years is heavily weighted toward other segments, not Asset Management:

Either BAM overvalued, or BN is very cheap?

One area where this disconnect is particularly striking is in the carried interest (bonus when funds do well).

BN retained 100% of the carry from legacy funds and earns a large share from new funds. In fact, through its ownership of BAM and legacy rights, BN benefits from ~82% of all carried interest earned. As AUM increases (last 5 years 15% CAGR), the carried interest also increases. The longer it has the capital working, the more the returns compound, resulting in higher carried interest potential. To be clear, carried interest is only triggered with realized cash transactions; the valuations used prior to sale have no impact on carried interest.

Carried interest doesn’t show up in GAAP/IFRS earnings right away. It accrues gradually as investments grow in value but only get recognized once the assets are sold and clients have received their original capital back.

This means there’s a significant amount of unrealized carry sitting on BN books. As of Q2 2025, there’s $6.7b of unrealized carry (net of costs), and management expects to realize significant amounts of this into the P&L. Between the 6 months from YE2024 to Q2 2025, $0.3b of net interest carry was realized.

Management thinks that the interest carry is worth $30b, which is a big portion of BN $99b market cap.

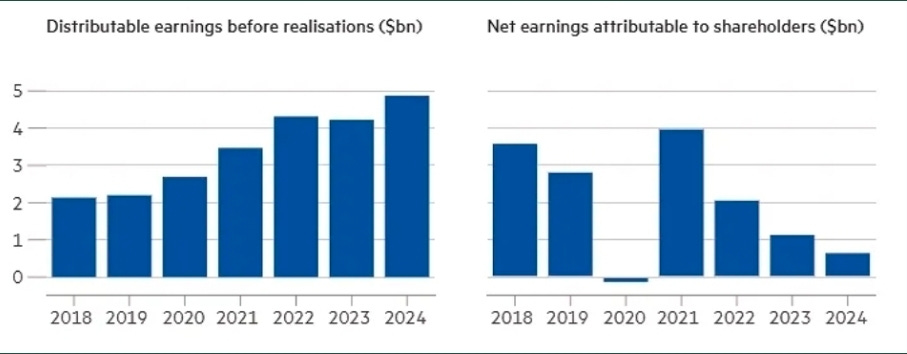

DEBR vs Net Earnings

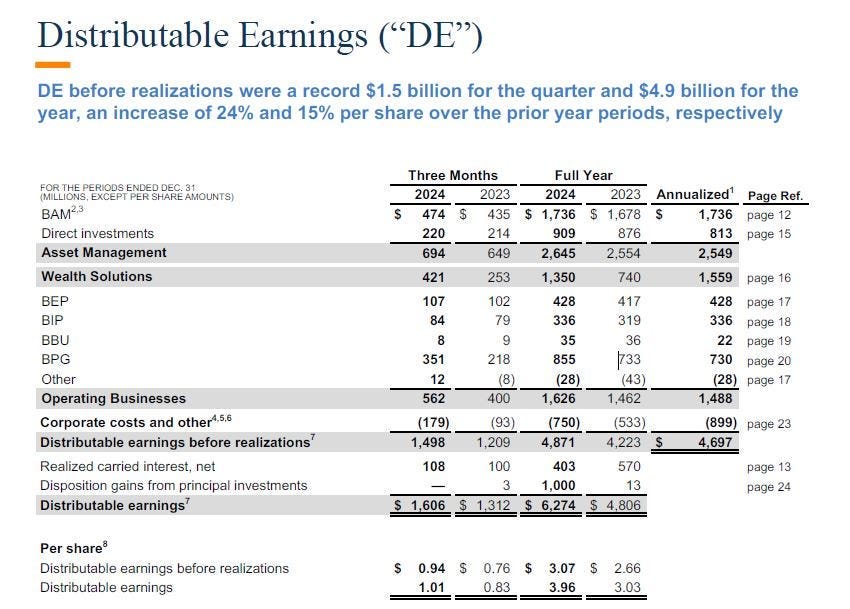

BN uses Distributable Earnings Before Realizations (DEBR) to give investors a clearer view of its true earnings power. DEBR essentially strips out the noise and focuses on cash the business can actually use.

This is the reason BN stock doesn’t screen very well, look at the IFRS net earnings versus DEBR:

In 2024, BN reported $4.9b in DEBR, and it’s targeting $13.5b by 2029. Note: 2024 DE (After Realization) was $6.3b.

“Before Realization” means carried interest is excluded, regardless if it’s realized or unrealized. Therefore, DEBR is a conservative baseline.

This is significant to keep in mind. For example, BPG owns a large number of development assets (~$6b) which generate little in terms of cash flow, so these assets make no contribution to earnings numbers or to DEBR. However, these assets will be sold when the time is right. Over the past 2 years alone, BN sold 192 properties for a combined $27b, at a premium of ~3% to their carrying value. It finances most of its real estate using non-recourse debt, meaning each property stands on its own with minimal risk of contagion across the portfolio.

This “hidden value” will materialize as carried interest in due course. For this reason, an investment in BN must be viewed from a long-term lens.

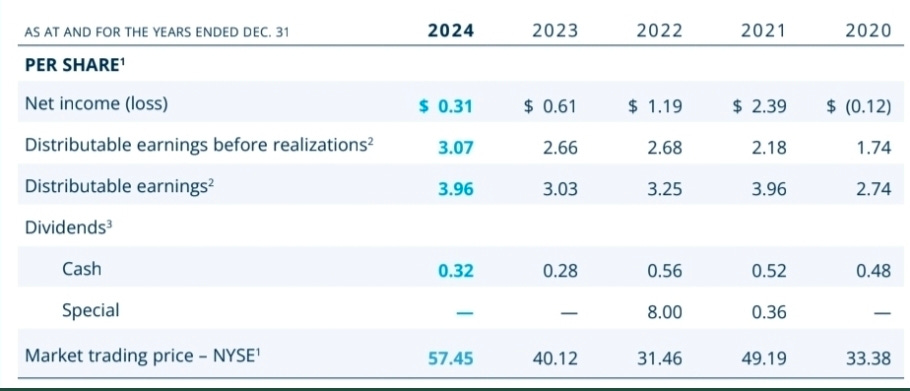

Below is the per share DE for last 5 years:

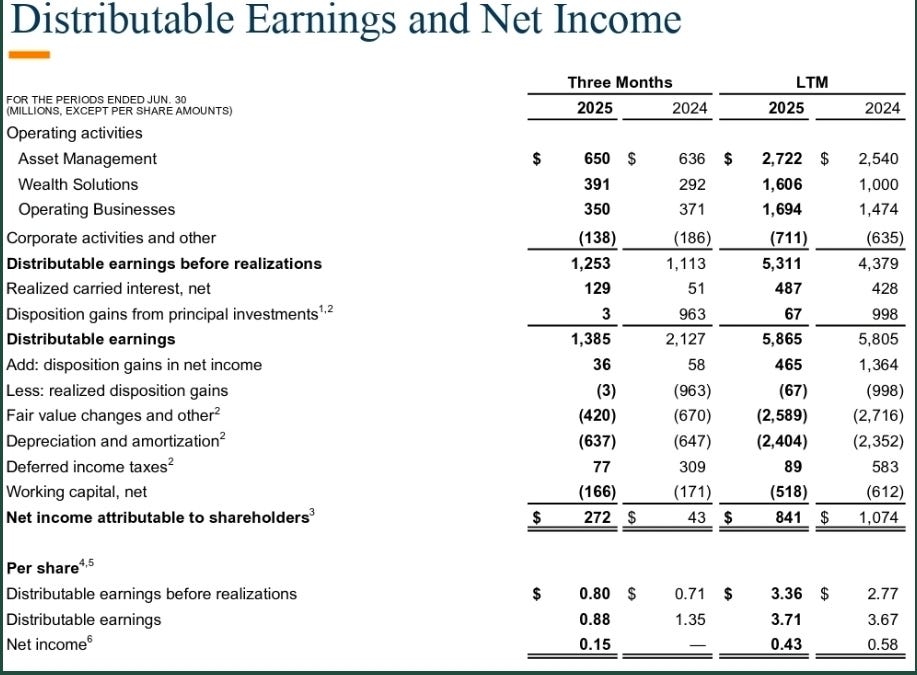

Q2 2025:

Insurance Playbook

BN is following the playbook that Apollo pioneered by investing insurance float into private, investment-grade credit rather than low-yield government bonds.

But BN has an advantage since it already owns a lot of assets that are perfect for insurance portfolios: long-dated, cash-yielding, and often indexed to inflation. Then, they use the float to invest in their own private assets which yield higher returns. It’s a playbook similar to Berkshire, which itself drew inspiration from Teledyne.

Since BN already has lots of capital, it can invest in the existing portfolio of long-term, cash-generating real assets (infrastructure, renewables, and real estate). And because it focuses on life insurance and annuity products that stretch over decades, the investments match the liabilities duration.

This is the growth model with Brookfield Wealth Solutions (BWS). Just 4 years ago, the business managed around $4b in float. Today, that figure has ballooned to $120b, due to acquisitions like American National, Argo, and American Equity Investment Life.

The results were fantastic, from generating almost nothing a few years ago, the insurance arm now contributes around $1.4b in earnings. By 2029, BN aims to triple the float to $300b, potentially generating $5b in annual earnings. Key growth markets include expansion into the UK, Europe, and Japan.

There is also synergy with BAM when BAM invests the insurance float on behalf of BWS. In effect, BN earns returns above the cost of insurance liabilities, while BAM generates a steady stream of high-margin management fees that doesn’t require incremental capital expenses. It’s a flywheel of value creation that compounds over time.

Future Outlook

Today, the $135b insurance float consists of largely long-duration fixed rate annuities savings products sold to individuals, whereby BN promises to pay an annual coupon of ~5% and repay the principal at the end of a 7 to 15 year term. These policies are very low risk in nature, and they can use this float to invest in assets within the parameters set out by insurance regulators.

They intend to allocate further equity capital to the annuity business, and over time the equity base backing these policies could increase to $75b to $100b, allowing BN to grow the annuity book to $500b to $750b.

Today, a small portion of the business, $3.5b of equity and $8b of assets, backs insurance written for the Property & Casualty (P&C) market. Over time, the equity could grow to $30b to $50b, which in turn should underpin a book of $100b to $150b of P&C insurance.

BN only underwrites risk that they know well. Currently, they write policies for real estate construction in New York. Because they have immense real estate knowledge and understand construction risks intimately.

They intend to expand this business across the US and internationally.

In another example, BN writes insurance for industrial warehouses, renewable power facilities, and industrial plants. All of these they understand very well, having operated them for decades.

BN goal is to dominate some specific lines of business over time by focusing on the asset classes that they know best.

They will continue to fund the insurance operations from their own balance sheet. This gives great comfort to our regulators that BN’s own money backs the policies they insure.

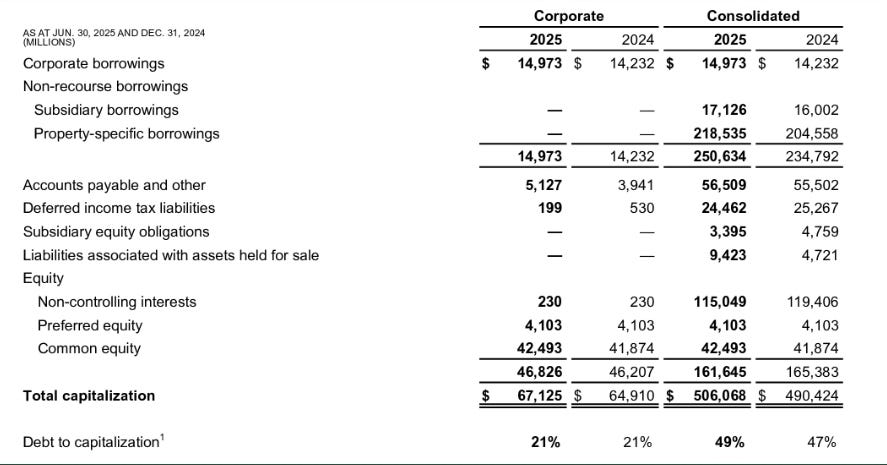

Non-recourse Debt

Virtually all of the debt within BN business is issued by entities or assets within the funds that they manage and is non-recourse to BN.

Only 6% of total consolidated debt has recourse to BN. As of Q2 2025, total corporate capitalization was $67b, with a debt to capitalization level of 21% at the corporate level based on book values, which excludes virtually all of the value of their asset management business.

Below is the maturity profile for recourse debt:

Insider Ownership

At 84, Jack Cockwell still attends board meetings, the last ghost of the pyramid schemes that built and destroyed the Bronfman empire.

Bruce Flatt’s (age 60) holds 15.9 million Class A shares worth over $1b (his annual salary was $375k). The Partners as a group own 20% of BN.

Class A shares are traded publicly.

Class B shares are all privately held and controlled by one entity (Brookfield Business Partners) which allows Class B to assert voting rights to nominate directors.

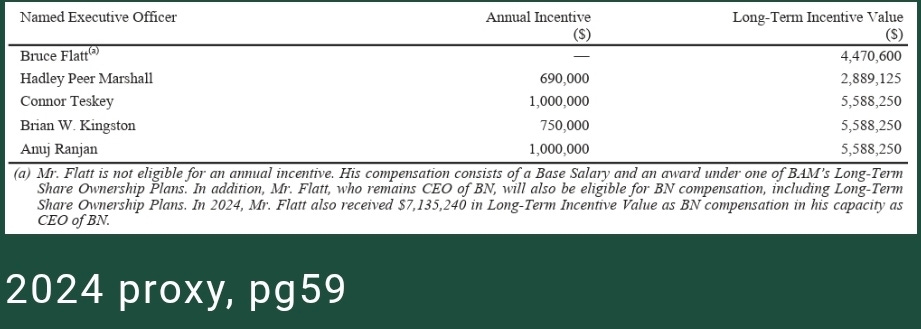

Incentives Structure

The determination of annual incentive awards and long-term ownership awards is not formulaic but instead is entirely based on the Board’s assessment of the specific actions taken during the year by the team to implement BAM’s strategic plans in the context of long-term value creation.

The 2024 targets quoted from proxy:

1. Increased Assets Under Management to over $1t and Fee-Bearing Capital to $539b.

2. Raised $137b of capital for the full year.

3. Deployed $48b of capital over the year, most notably within credit (over $26b), real estate ($6.1b), and private equity ($5.9b). Additionally, sold assets and businesses valued at nearly $40b, representing $30b of equity capital.

4. Asset management business recorded strong financial results, generating $2.5b of Fee-Related Earnings in the year, +10% from the prior year, and $2.4b of Distributable Earnings, +5% from the prior year.

5. Increased quarterly dividend by +15% to $1.75 per share on an annual basis.

For those achievements, below are the rewards:

Recent Deals

2019

Oaktree Capital

BN acquired a 61.2% stake for $5.2b, significantly boosting its presence in credit markets. This pushed total AUM over $500b.

Indian Telecom Infrastructure

Through Brookfield Infrastructure Partners, they took full ownership of a telecom tower business in India from Reliance Industrial Investments for $3.7b.

Canadian Mortgage Insurance

Brookfield Business Partners acquired a majority stake in Genworth MI Canada for CAD$2.4b, tapping into the residential mortgage insurance market.

2020

BrandSafway

Acquired as part of BN private equity strategy, this is an industrial and commercial services company.

Renewable Energy in Europe

BN invested in solar assets across Europe, strengthening its renewable power segment.

Simply Self Storage

For $1.2b, BN acquired a portfolio of 8 million sqft of self-storage facilities across America.

2021

American National Group

Insurance firm acquired with $25b worth of in-force policies at a price at 70% book value. Sachin Shah joined BN in 2020 to create their insurance arm from basically nothing.

Asia-Pacific Infrastructure

BN completed the acquisition of a data distribution business in New Zealand and took a 45% interest in a global infrastructure services company.

2022

SBB EduCo

49% stake in this Swedish social infrastructure platform for SEK9.2b, with potential for further payouts. The investment supports public education facilities.

Transition Fund & Real Estate

Deployed $7b through its Transition Fund and acquired 3 real estate companies totaling $9b in assets, purchased at significant discounts to replacement cost.

Semiconductors with Intel

BN entered into a $30b partnership with Intel to develop a leading-edge semiconductor facility in Arizona.

Deutsche Telekom Towers

Majority stake in Deutsche Telekom’s German tower business for €17.5b.

2023

India Real Estate

BN acquired a significant stake in several marquee commercial properties previously owned by Bharti Realty, a subsidiary of Bharti Enterprises. This partnership is in the form of a JV, with a more recent transaction where Brookfield India REIT acquired a 50% stake in four Grade A assets from Bharti Enterprises for ₹6,000 crore, making Bharti the second-largest unitholder in the REIT.

Record Fund Closures

BN raised $12b for its largest-ever PE fund and $6b for its third global infrastructure debt fund.

2024

American Equity Life

Acquired this life insurance firm and began streamlining operations. Exiting non-core product lines, improving capital efficiency, and driving annuity growth.

Neoen

BN acquired a 42% stake in Neoen, a French renewable energy firm. Later increased to 97.7% in 2025. The company has an 8,000MW portfolio of highly contracted operating or under construction assets and a large, advanced stage 20,000MW pipeline.

Q2 2025 Monetization

Markets are now in good times and we can see this benefitting BN through the various sales. We quote some examples that management has given IRR numbers in Q2 2025:

In Australia, BN completed the sale of a senior living platform for A$3.85b, generating a 19% IRR and a 2.3x multiple of capital.

Closed the sale of a 25% stake in Shepherds Flat, one of the largest wind farms in the US, and sold a minority interest in a portfolio of stable, operating hydro assets. They also completed the partial sale of a South American hydro platform, fully exiting the fund’s stake in the investment. Since their initial investment in 2016, the business has consistently delivered strong performance, and its outlook remains strong. To date this year, BN energy monetizations achieved an aggregate 17% IRR.

Sold 60% of PD Ports, one of the UK largest port operations for ~$1.3b of proceeds, achieving a 19% IRR and a 7.5x multiple of capital.

In Australia, BN disposed of part of their container terminal operation for $2b, generating a 17% IRR and nearly a 4x multiple of capital.

Comments on Competitors

BN competes with major alternative asset managers: Blackrock, KKR, Apollo, Macquarie.

Blackstone is probably the largest rival. With $1.1t AUM, they’re 19% larger and growing faster. In real estate specifically, Blackstone commands $315b versus BN $200b. Blackstone cornered datacenters, over $80b invested, creating network effects that BN can’t match.

However, BN employs 250,000 people actually operating assets. Blackstone employs 4,500 mostly financiers. When infrastructure breaks, Blackstone hires consultants. BN sends their own people. It’s a fundamentally different business model.

But eventually, the competition’s evolution reveals a convergence threat.

Blackstone hires operators.

KKR builds credit platforms.

Apollo buys insurance companies.

Everyone copies and converges. Does BN operational heritage remain distinctive, or does it erode?

Valuation

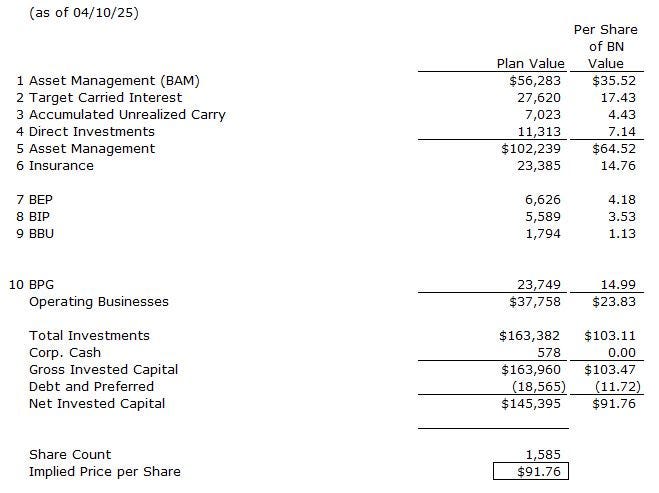

BN management actually provides a sum-of-parts valuation that they call Plan Value. They claim the intrinsic value of BN is ~$145b versus ~$100b today:

Publicly Traded Entities (#1,7,8,9)

These are publicly traded: BAM, BIP, BEP, and BBU.

Carried Interest (#2,3)

#3 is carry that has been accumulated but unrealized. That figure should be good money.

#2 is a PV estimate of what they expect to earn from their current funds in the future. We can apply sensitivity tests on this value.

Direct Investments (#4)

General partnership contribution to the funds that BN raises. This is probably good money.

Insurance (#6)

This is the value of BN annuity/insurance business. It is valued at 15x DE, which seems reasonable.

Brookfield Property Group (#10)

This is another controversial issue. This $24b represents the equity value of the real estate that BN owns on balance sheet from their privatization of Brookfield Property Partners.

We don’t know how good is this figure, but we know it’s worth more than zero. We’ll do sensitivity tests on this.

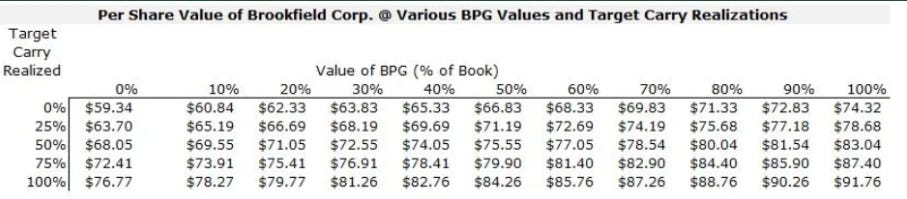

Sensitivity Test

Now we have 2 variables that we are unsure of: projected carried interest and BPG book value.

The current market share price of $67 implies that both variables are worth less than 50% of their full estimates.

If you believe management’s calculation, then BN shares are quite undervalued.

In 2022, Plan Value was $69/share and BN shares traded at only $31. Now 2.5 years later, Plan Value is $92/share, while BN shares rose +113% to $66. The gap is still significant but has narrowed.

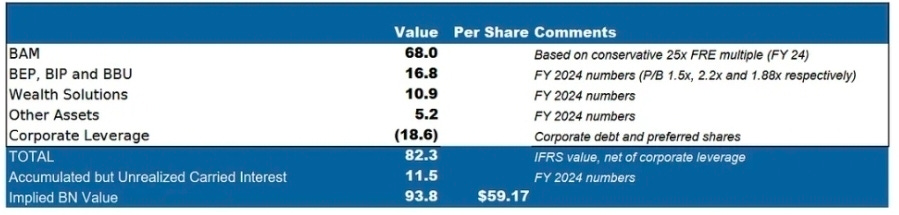

Our Sum-of-Parts

If we build the valuation with these assumptions:

BAM at 25x fee-related earnings ($2.5b). Sanity check: (25*$2.5b)/0.73 = $93b at 100%, current market cap $92b.

BEP, BIP, BBU at 1.5x, 2.2x, 1.9x book value respectively.

Wealth solutions (insurance segment) at 1x book value.

Other assets at 1x book value.

Based on FY2024 numbers, we get a much smaller intrinsic value of ~$94b. The difference from BN’s valuation is mainly:

1. Premium given to BWS as it’s growing fast.

2. Capitalizing the future expected unrealized interest carry.

Does the management team believe their own valuation?

Apparently, they do. By spending $982m in 2024 and $856m in YTD Q2 2025 on shares repurchases, they seem to signal the belief that BN shares are undervalued.

Misc Notes on Real Estate

Inflation and interest rates are risk factors to real estate valuation. People discount the net operating income (NOI) to arrive at a valuation, so a higher interest rate will drive down prices.

The first line of defense for any real estate investor is to own quality assets; buildings with unique locations, and desirable characteristics for customers.

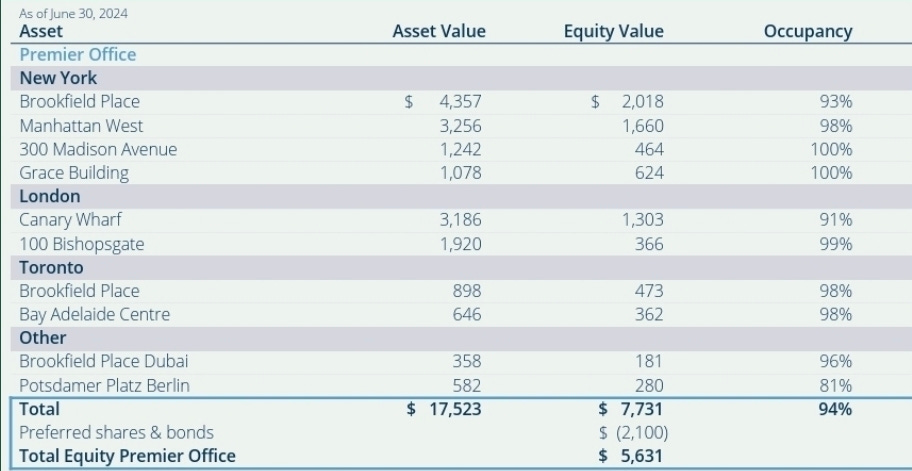

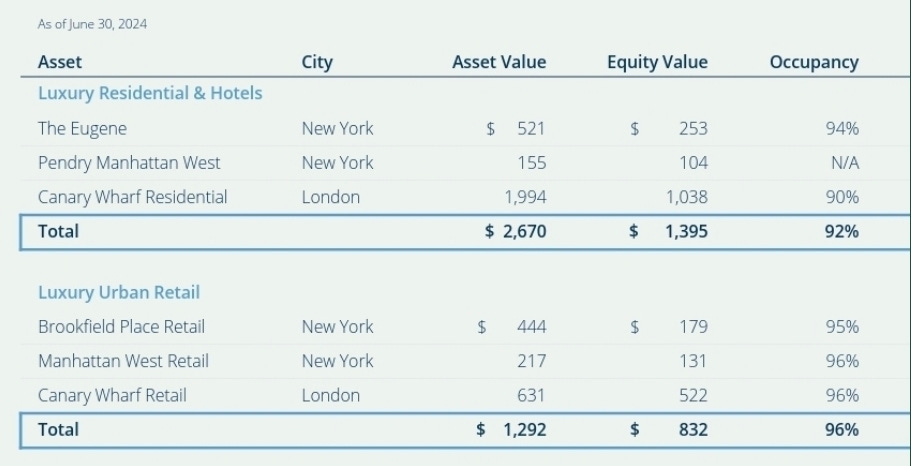

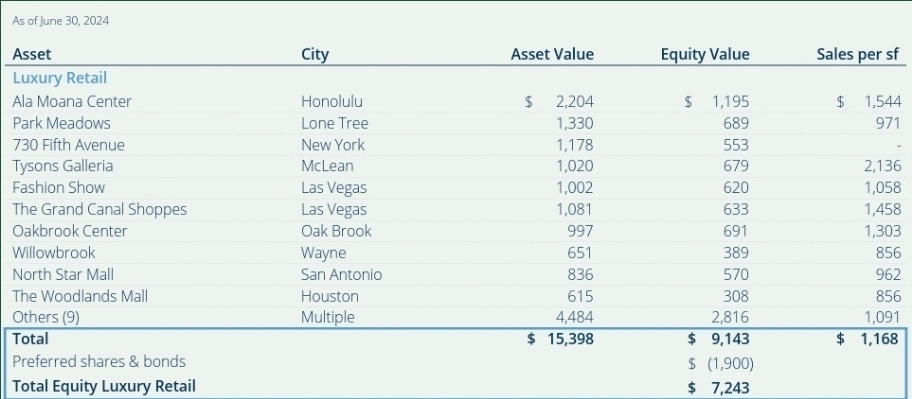

Take a look at the iconic assets that BN manages…

Offices

Mixed Use Complexes

Retail Malls

The second defense is to limit exposure to refinancing debt risk. Bruce Flatt, in all of his shareholders’ letters, reiterates the use of fixed rated debt. He is really obsessed with maintaining this debt exposure no matter the cost in the short term. For example, on the 2014 letter, he mentioned that the annual cash cost of using fixed rather than variable rates was a whopping $400m!

As mentioned above, 94% of all borrowings are asset specific non-recourse debt. This limits the losses to BN by just surrendering the asset. The maximum equity exposure is usually 50% of the purchase price.

Having a strong defense position allows BN to benefit from an inflationary environment. During periods of higher inflation and interest rates, the replacement costs (incurred to develop a similar property) tend to increase. This is because access to credit tightens as rates increase, lending periods are shorter, financial covenants are stricter, and building costs increase.

This brings 3 important consequences:

1. The pipeline for new buildings becomes limited. This means that existing buildings become more valuable due to less competition.

2. Returns and rents need to increase to net off the impact of higher costs. With higher rents in the area, existing buildings can increase rental without much effort.

3. Opportunities to acquire some properties at a deep discount from owners who have weak capital structures. This opens the door to companies such as BN to make cheap acquisitions.