AZO: Autozone (4)

Forward Returns Not Attractive

AZO has done well since we bought it in May 2024 at average price of $2,981. Currently, the stock is trading at $3,954 and the PE multiple has expanded to a 10-year high of 27x.

The company is well understood and operates in a predictable market, so why did the multiple expand to double of its historical average of 18x?

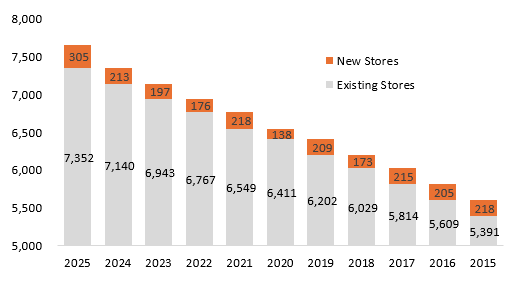

We think most of the enthusiasm comes from the new CEO, Philip Daniele, who guided towards adding 500 new stores in year 2028. He became CEO in 2024 and implemented his expansion plans. In 2025, they managed to open 305 new stores. It was a record high, ending the year with 7,657 total stores:

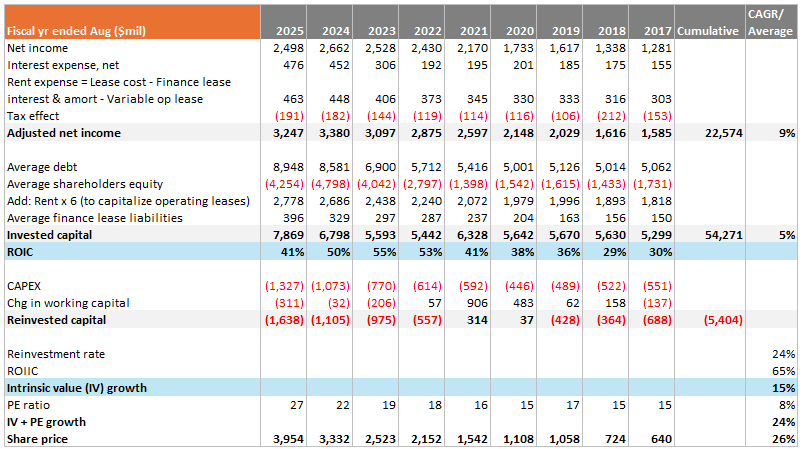

The ROIC at total company level is still producing good results, suggesting that the unit economics from opening the marginal store is still intact. This could be why the market believes that AZO can indeed achieve its goals without hurting ROIC:

Over the past 9 years, AZO stock price compounded at +26% with PE expansion contributing +8% and shares reduced by -6%. This means the underlying business compounded at +12%. This is a very impressive outcome especially when the business is selling auto repair parts/services.

Unfortunately, we think there’s not much forward returns left for investors going in at such elevated earnings multiples. Because the business model of AZO is to use all their free cashflows (FCF) to repurchase shares, and high price multiples will reduce the amount of shares they can retire.

The consensus is for 325 to 350 new stores in 2026. If that is correct, we think 500 new stores by 2028 is a stretched target. In our model, we push the timeline out to 2030.

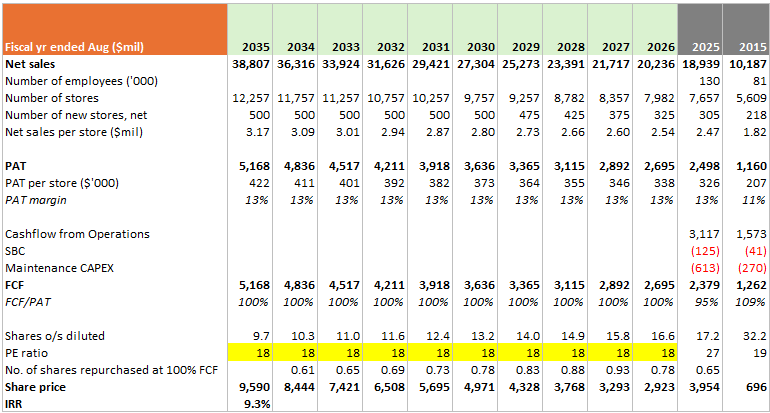

A decade ago, AZO operated 5,609 stores with each store generating $207k of profit after tax (PAT) on average. The stores sent this money back to headquarters for allocation, which were used for buying back shares. During then, there were ~32.2 million fully diluted outstanding shares, meaning that if you owned 5,741 shares, effectively you could think of yourself as a happy owner of 1 AZO store.

Fast forward to 2025, shares outstanding has shrunk to ~17.2 million, if you had held on to your 5,741 shares then your economic ownership has almost doubled without you putting in any effort. You now have economic claims on 2 AZO stores without investing a dollar!

This only works wonderfully if AZO shares are persistently cheap such that shares repurchased produce a good yield. The average PE ratio was 18x, that’s a 5.6% earnings yield without factoring in growth. Over 10 years, that’s a tailwind of +6% CAGR.

Let’s model a good scenario where the PE averages 18x for years 2026 to 2034:

Assumptions:

500 new stores achieved in 2030. Thereafter, same addition of 500 stores each year.

Net sales per store grow at inflation +2.5%.

PAT margins per store constant at 13%.

100% conversion from PAT to FCF, all of it used to repurchase shares.

Exit and average PE both at 18x.

We can then model the number of shares repurchased and find the resulting share price. In this case, return is CAGR +9.3% until 2035. All else equal, if the PE ratio is higher during 2026 to 2034, then we will get a lower return because lesser shares can be repurchased.

This outcome doesn’t look appealing, so we will hold on to our position and wouldn’t recommend buying.

Don’t be Promotional

Most CEOs rise to their position by being elite operators or salesmen, very few are truly great capital allocators. Once they become CEOs, they face new responsibilities. They now must make capital allocation decisions, a critical job that they may have never tackled and that is not easily mastered.

Capital allocation is no small matter: After ten years on the job, a CEO whose company annually retains earnings equal to 10% of net worth will have been responsible for the deployment of more than 60% of all the capital at work in the business.

This situation is an example of why we prefer management teams that don’t give guidance, even better to not engage in quarterly earning calls. It’s much better to communicate through thoughtful letters and annual meetings.

AZO has genuinely great plans to expand their business, CEO Philip Daniele understands the hub-and-spoke distribution model, he was the Executive VP of Merchandising, Marketing and Supply Chain from 2021 to 2023 and Senior VP of Commercial from 2015 to 2021. However, they don’t have to promote it because this will likely cause the stock to be re-rated with higher multiples, which is counter-productive when repurchasing shares.

If you go back to read the earning calls of previous CEO William Rhodes, you could hardly find instances where he gets promotional. In his 20+ years of leadership the stock’s PE ratio never went above 21x, that provided an yield advantage as he eventually repurchased all of AZO shares outstanding since IPO.

Strangely, the market should assign higher multiples to AZO for its earlier years when their stores footprint was less saturated. But due to the clever restraint of self-promotion, they managed to keep market expectations under a lid.