AZO: Autozone (3)

Impact of EV

This post addresses the idea that the transition from ICE to EV will be detrimental to AZO business.

We argue that it is unlikely that the earning power of the large auto maintenance retailers (AZO, ORLY) will be impaired.

Consider the following statistics:

1. Light vehicle fleet in the US: 280 million vehicles.

2. Annual scrappage: 13 million vehicles.

3. Normalized annual new light vehicle sales: 16.5 million.

4. The average age of the active fleet has been increasing at ~0.2 years annually, and the current average age is 12.2 years.

5. Natural growth in cars: 4 to 5 million.

This means that EV penetration likely needs to be 30% of 16.5 million to cause flat growth in ICE vehicles. More than 30% will cause ICE sales to decline.

Our guess is that 30% penetration is going to be at least 5-7 years away. We think there are some limitations such as affordability, EV technology, and constraints on EV production.

For AZO core market of vehicles aged 6-15 years, the decline of active ICE fleet is likely at least 11 years away.

In that interim period, AZO will continue to grow its business and take market share away from fragmented small players, leveraging on the scale advantages that it has.

Do-it-for-me (DIFM) Segment

AZO is expanding its store base by 2.5% per year. Historically, it focused almost exclusively on retail DIY customers, but has invested in building the infrastructure and practices to sell into commercial repair shops. The commercial DIFM business is now 32% of sales and growing fast.

AZO has 18% market share in DIYM distribution, and as long as AZO keeps executing, there is no reason why this segment can’t grow at a healthy pace.

Reducing Transaction Count

One of the less well understood factors about auto parts retail is that it is a slightly negative unit growth industry. As technology gets better and cars become more durable, the number of parts requiring maintenance decreases. The offset is that these parts cost much more to repair/replace.

For example, copper spark plugs used to last 30,000 miles. Now cars use iridium spark plugs and they last 100,000 miles. The old copper ones used to cost $0.59. But the iridium ones are often times over $10.

So there’s an upward pressure on price per piece and a downward pressure on units.

This economics follows through into EV as well. Better quality leads to lesser transactions but higher prices.

This is what LKQ Corp management said:

When you look at hybrid electric vehicles and EV, technical service parts command anywhere from a 2x to 6x premium relative to their comparable ICE counterparts.

The technical complexity, not just with batteries, but also with the electrification of components previously belt-driven such as air conditioning, compressors, and water pumps. For example, a 2013 Prius with an electric water pump, that water pump sells for 3x the value of a 2013 Corolla that has a belt-driven water pump.

In the UK, for example, a 2017 Golf ICE water pump sells for about £77. The Lexus hybrid EV water pump is £278. And so the EV parts are much more expensive. We think that’s going to continue to be the case for a long time.

However, is this a structural feature or will prices come down as EV manufacturers scale up?

We can actually refer to historical examples… In one particularly salient moment from 2009, ORLY’s management described what a step change there was in vehicle quality from the 1980s to 1990s as both technology improved and the entry of Japanese cars massively raised the quality levels of the entire industry.

You might think the superior quality will lead to lesser repairs and is a headwind for the industry.

But the opposite happened. In reality, as cars become better, people maintained them regularly and kept them for longer. This was actually a tailwind for auto maintenance businesses!

This is what ORLY management had to say:

I think that the American consumer is going to find out that the vehicles that were built in the 1990s and early 2000s, that those vehicles can be driven at very high mileages safely and without trouble if they’re maintained correctly.

Most of us have realized that vehicles these days just don’t have as many problems as they used to from a drivability standpoint.

They still take maintenance, brakes, belts and hoses, stuff like that, but you don’t have problems with the cold starts when carburetors didn’t work when the chokes didn’t operate correctly.

Every single part and system of a car today requires less maintenance than it did many years ago.

Every part fails less often than it used to.

However, these factors did not reduce business opportunities.

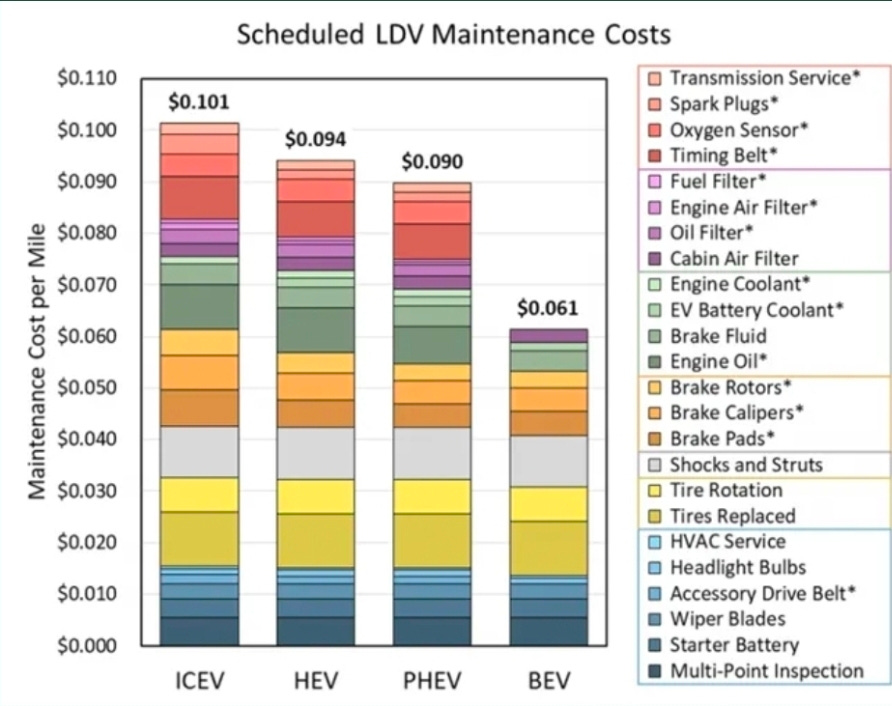

Undoubtedly, there will be a significant fall-off in transaction counts when a customer switches from an ICE to an EV, but it won’t go to zero. According to researchers funded by the Argonne National Laboratory, hybrids and EVs will generate a much lower but still non-trivial amount of aftermarket repair and service work:

Outside the US

AZO also has business in Brazil, Mexico and Puerto Rico, these countries have even lower and slower EV penetration.

A survey by Sindipeças reveals that the circulating fleet of cars, light commercial vehicles, trucks and buses in 2024 in Brazil reached 48 million units, up 2% in 2023.

In the case of cars and trucks, the average age rose YOY to just over 12 years old.

Brazil registered around 177,000 electric vehicles in 2024, an impressive increase from ~41,000 units in 2019. BYD cars are the most popular imports. However, this is a tiny 0.5% penetration rate currently.

Conclusion

To put it altogether, we think AZO will grow predictably for the next decade and the business model will not be impaired even after EV replaces ICE cars.