AZO: Autozone (2)

Preface

We wrote about AZO in May 2024 here, it includes a long company history and its business model. During then, market cap was $51.9b and our estimate of fair value was $55.8b. We still have the position in AZO at +7.7% gain, currently the market cap happens to be equal to our initial fair value estimate. Over the last year EPS has grown by +13.6% but free cashflow per share fell by -5.3%.

In this post, we update our fair value estimate and explain why AZO has a great business model.

Business Factors Results in Success

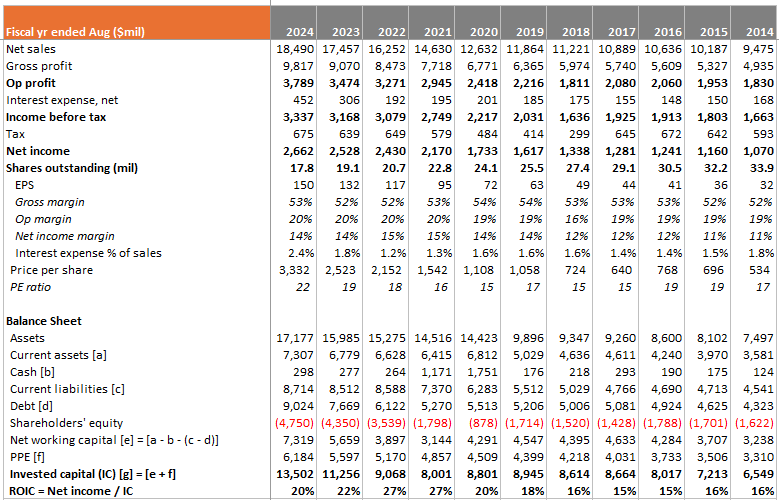

The long run share price of any business is a measure of how well the company performed. Since IPO in 1991 to 2024, AZO total shareholder return was an impressive CAGR of 20.4% (it doesn’t pay dividends). Sales grew from $800m to $18.5b and earnings-per-share (EPS) grew from $0.33 to $149.6 (CAGR 20.4%). This is evidence that fundamentally, in the long run, business value grows in tandem with earnings.

In 1996, AZO operated 1,423 domestic US stores, today they have 6,432 domestic and 921 overseas stores. Shares outstanding were 145,940,000 in 1992, today it has shrunk by 88% to 17,803,000.

At first glance, AZO success might seem like a simple financial story, propelled by aggressive share buybacks and a focus on shareholder returns. But there is a deeper narrative driving the ability to enrich shareholders. AZO capital allocation strategy is not just about buybacks; it starts with operational excellence. Every part of the daily operations feeds directly into its financial engine, enabling the foundation of generating free cashflow and, ultimately, its ability to reward shareholders.

Inventory

AZO inventory turnover ratio is low at 1.5x compared to other retailers who often have turnover ratios of 10x. However, this is not a sign of inefficiency, it is a deliberate move to facilitate customer satisfaction, which is the most important thing for AZO in the long run.

AZO operates a highly structured supply chain system designed to efficiently meet customer demand. This system is organized around “Mega Hubs” and “Feeder Stores”, these 2 concepts optimize inventory management and enables fast distribution.

Mega Hubs are large distribution centers that keep stock of an extensive range of products, often carrying over 100,000 SKUs. These hubs serve as central nodes in the supply chain, capable of replenishing inventory for a wide network of nearby Feeder Stores. They play a critical role in ensuring the availability of less commonly requested or specialty parts, which might not be stocked in smaller stores. Mega Hubs are capable of fulfilling orders for nearby stores within 24 hours.

Feeder Stores are standard retail outlets that maintain a focused inventory tailored to local demand. These stores rely on Mega Hubs for frequent restocking, allowing them to serve customers quickly while avoiding overstocking at individual locations. The Feeder Stores act as the primary point of contact for retail and commercial customers, providing parts and services directly.

This setup ensures that even the most obscure car parts are available. Although at a company level the inventory turnover is low, but at the individual store level inventory is actually much more efficient because the Mega Hubs act as a safety net keeping customers happy and loyal. In the auto-parts aftermarket if a customer doesn’t find what he needs when his car breaks down, usually he is not going to come back a second time.

Negative Working Capital

Note: working capital defined as current assets less current liabilities.

AZO takes payments from customers upfront at point of sales but have historically negotiated extended payment terms with suppliers. These payment terms are non-predatory; AZO has arrangements with third-party financial institutions for invoice balances owed to certain suppliers. These arrangements allow suppliers, at their discretion, to enter into agreements directly with these financial institutions to finance AZO’s obligations.

This timing gap produces negative working capital where suppliers are effectively financing AZO growth. It also means that AZO operates on a leaner balance sheet and can produce high returns on invested capital (ROIC).

The ability to negotiate for better payment terms does not fall from the sky; it has to be earned. It is the result of decades of good reputation, earning the trust of suppliers who are willing to accept these terms voluntarily.

Management Incentives Structure

Management is incentivized on basically 2 things:

Earnings per share (consequently, free cashflow per share)

ROIC

It has not changed for 33 years, and we believe it will not change in the future.

Many businesses fall into the trap of empire-building; chasing size, adding assets through acquisitions and leveraging up to create the illusion of success. The obsession with “size” is a familiar theme in corporate history. Management teams are often driven to grow their companies due to a lack of core competencies or poorly designed incentives. This typically leads to unjustified acquisitions, leveraged expansion or revenue chasing, all for the sake of growing “size”.

During good times, these can look great. But during downturns, debt becomes difficult to finance and poor acquisitions fail to generate returns. All these activities distract management from what really matters: generating ROIC for shareholders.

Now, imagine that AZO had taken the common route of empire-building. It would have aggressively acquired smaller competitors, grew the store count without optimizing for ROIC, or took on debt to finance unprofitable growth. In the short run, it might impress with flashy reported earnings, but in the long run the fragility of such an approach will show up during economic cycles.

AZO has intelligently structured their incentives to avoid empire-building. Efficient capital allocation and operational discipline are the main incentives, which are also the drivers to value creation.

Management also views these metrics over a 10-year horizon:

We believe these metrics, when viewed over a ten-year horizon, provide a strong indication of whether our compensation program embodies not only a pay-for-performance incentive structure, but also a pay-for-long-term-performance incentive structure.

2023 proxy statement

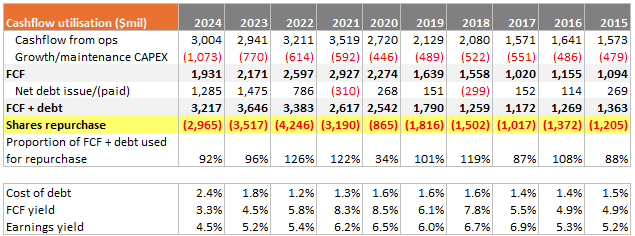

Shares Repurchase

Since 1998, the Board has approved to repurchase shares up to a total of $39.2b, so far management has repurchased $37b worth of shares. This reduced shares outstanding by 88%, which translates to 830% shareholders return. Put in another way: shares repurchase alone contributed 8.5%, out of total 20.4% CAGR since 1998 (26 years).

We can do a rough estimate that the repurchase yield was 6.3% (PE ratio averaged 16x). In the last 10 years, the PE of AZO has been higher and average repurchase yield fell to 5.8%. This is still better than their cost of debt:

Retail Blueprint

When looking at the growth and success of AZO, it’s important to remember that this is not an e-commerce business in a time where more people are shopping online. This is a retail-first business. AZO does have an online platform with delivery options, but the focus is very much on the physical locations.

Like most major retailers, stores follow a blueprint for how they are designed and where they should be located. These are the requirements:

AZO will consider land purchases, freestanding and in-line spaces, ground leases, and co-development opportunities.

Lease spaces must include an abundance of uncongested, customer-friendly parking spaces.

Stores typically range from 6,500 to 8,000 square feet.

Land parcels for new construction must accommodate between 25 to 50 parking spaces.

Mega Hubs range from 33,000 to 35,000 square feet with 75 to 100 parking spaces.

Upfront, high-impact locations with excellent visibility and access from adjacent streets.

Points #2 and #6 are perhaps the most important blueprint for creating customer satisfaction: lots of parking spaces and easy road access. We can look to Costco for a perfect example of how the shopping experience should be built.

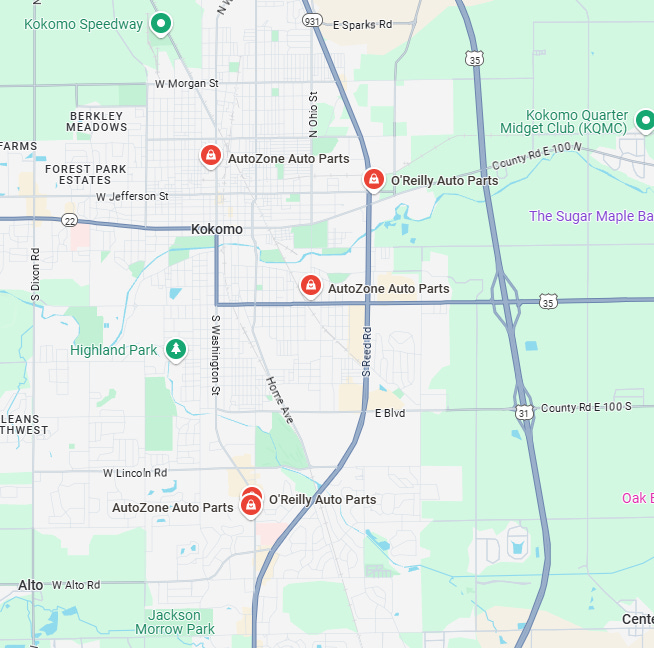

Easy road access is a crucial benefit for AZO as it puts the stores closer to the potential customer. When your brake lights need to be replaced, you will more likely choose the shorter and easier drive. Convenience is important and AZO knows this, it is not afraid to open several stores in a single town. For example, in Kokomo, Indiana, a city of 60,000 people, there are 3 separate AZO stores from north to south all within 6 minutes drive:

The blueprint also highlights uniformity as a factor for retail success. While not all stores will carry the same inventory, they will be designed in an identical way across the country. This creates cost savings for construction planning and it becomes significant at scale when AZO opens nearly 200 new stores yearly.

Culture of Customer Obsession

Founder Pitt Hyde said this in 2013:

Our objective was to build a culture around superior customer service, and to have every day low prices in good-looking stores… In 1991, we went public, and the competition saw how well we were doing. They started copying our store layout and pricing. But none of them could copy our culture.

Loan-a-Tool (launched in 1986)

The Loan-a-Tool program shoes how AutoZone alleviates common pain points for its customers. Many vehicle repairs require specialized tools that can be expensive for individuals who only need them for a single project.

Rather than a customer being forced to buy, AZO allows them to borrow tools at no cost. This service works through a refundable deposit system, where the customer pays the retail price of the tool upfront but receives a full refund upon return.

Lifetime Warranty

AZO also offers a surprisingly generous lifetime warranty on products. The warranty applies to specific items (brake pads, alternators, starters) ensuring customers are protected against defects for as long as they own the vehicle on which the part is installed. If a part fails during normal use, customers can return it to any AZO store and receive a replacement at no additional cost.

These practices of customer obsession creates economic goodwill that translates into repeat business. This culture is important especially in a competitive market.

ALLDATA (acquired in 1996)

ALLDATA was founded in 1986 to meet market demand for Original Equipment Manufacturer (OEM) repair information. As computer technology advanced, ALLDATA began compiling the largest single source of OEM information available and converted it into a digital format.

Today, the database covers 95% of vehicles on the road and is used by over 400,000 professional technicians worldwide.

It has a few modules:

ALLDATA Repair ($199/month)

ALLDATA Collision ($239/month)

ALLDATA Repair Planner ($129/month)

ALLDATA Mobile ($39/month)

Commercial Programs (DIFM) and DIY

In 2024, 92% of all AZO locations have a commercial program to serve professional mechanics, repair shops and fleet operators.

The infrastructure AZO built enables the fulfillment of commercial orders, often providing same-day or next-day delivery. In recent years this commercial segment is getting more attention as it presents growth opportunities. In 2024, commercial programs are in 5,898 locations and management estimates that this is just 5% of total addressable market.

AZO categorizes commercial programs as Do-It-For-Me (DIFM) and it generated $4.9b sales in 2024 (26% of total sales). In Q1 2025, DIFM has increased to 30% of total sales, reflecting higher growth profile than DIY (Do-It-Yourself, retail individual segment).

The reason for DIY having low growth is a headwind that cannot be reversed. Cars are becoming increasingly complex and fixing a car yourself is difficult. Most people will choose to go directly to professionals.

Economic Factors for Growth

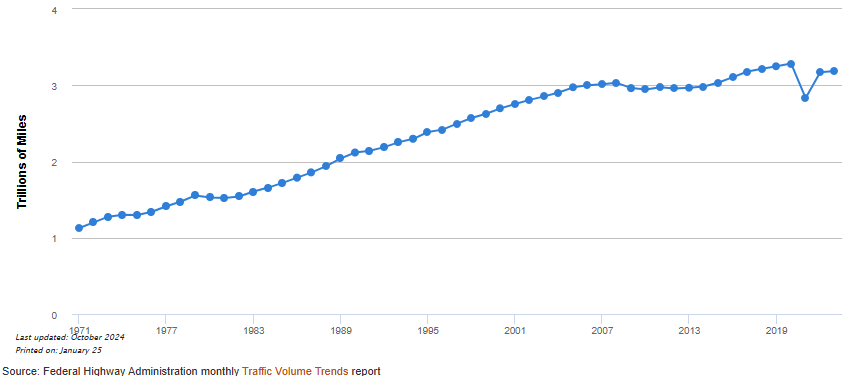

Distance Driven

The trend for distance driven has been increasing:

As cars travel further, we can expect the need for maintenance to increase as well.

Vehicles Older than 7-years

As the number of 7-years or older vehicles increases, we expect an increase in demand for the products AZO sells. The aging vehicle population will continue to increase as people keep their cars longer.

According to the latest data provided by S&P Global Mobility, the average age of light vehicles on the road was 12.6 years and these vehicles account for approximately 38% of US vehicles.

According to the US Federal Highway Administration, vehicles travel an average of 11,000 miles each year. In 7 years, the average distance driven will be 77,000 miles, which at this point most vehicles are not covered by warranties and maintenance dollars goes to after-market.

Adapting to Electric Vehicles (EV)

EVs do not require oil changes, spark plugs, or exhaust systems. But they require components like batteries, cooling systems, braking mechanisms and software. AZO has expanding its inventories to include:

Replacement parts such as cabin air filters, brakes, cooling systems for battery thermal management.

EV repair tools and equipment.

Electric charging accessories cables and adaptors.

Competitors

There are 2 main competitors: O’Reilly (ORLY) and Advanced Auto Parts (AAP).

AZO and ORLY are known to be the major players with AZO having slightly more market share. AAP is no longer competitive as the company is in financial restructuring, closing up stores, and shrinking headcount.

The auto parts after-market is still fragmented with many smaller players. AZO has a larger presence in terms of store count, both domestic and overseas.

The industry structure is favorable. AZO and ORLY lead a rational oligopoly, with the leaders rarely engaging in heated price competition, while small and fragmented base of disadvantaged auto parts stores continue to lose market share.

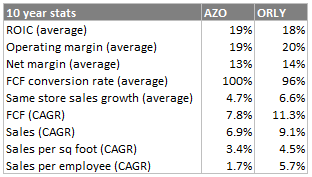

Below is the 10-year stats for AZO and ORLY:

Valuation Update

Phil Daniele is the new CEO who took over in June 2023 from William Rhodes (2005 – 2024). He’s an insider and has worked for the company for 31 years and is the fifth CEO in AZO’s rich history. William Rhodes is the Chairman of the Board now.

In 2024, AZO grew EBIT by +5.3% but free cashflow (FCF) fell by -11% (this is without accounting for share count reduction). This resulted in a lower than historical cash conversion due to an increase in CAPEX spending.

Phil Daniele started his role with an investment in the supply chain, which they named “Supply Chain 2030”. The investment is supposed to improve AZO supply chain network to support stores growth until year 2030.

On the technology side, they invested more in proprietary systems that support the Commercial DIFM segment.

He also made a large commitment to open 500 stores annually by fiscal year 2028, targeting 300 domestic and 200 overseas stores. Considering that AZO historically opened ~200 new stores yearly, this is indeed a high target. In our valuation, we don’t expect AZO to achieve this goal.

There was also investments made to Mega Hubs and ALLDATA.

Due to all these investments, CAPEX grew to $1,073m from prior year $770m. It is expected that CAPEX continues to be at $1b range in 2025.

DCF model

Therefore, the main changes to our valuation model:

Assume a lower cash conversion rate (73%) in coming years and slowly improving to historical averages (103%) in 2034.

Assume number of new stores to increase from 2025 to 2028, but only achieving net increase of 300 stores in 2028.

The DCF with discount rate 10% and terminal growth 2.5% gives intrinsic value of $59b (5% discount to current market cap $56b).

ROIC model

Suppose that we believe management’s commitment of $1b CAPEX investments, that is 30% of current cashflow from operations.

If we expect average ROIC to maintain at 19% with a reinvestment rate of 30%, then intrinsic value should grow at ~6%. Assume that share repurchases is half of historical rate at 3%, we can expect ~9% of total shareholder return. We think this is a conservative estimate with upsides:

DIFM margins are higher. ROIC could improve.

International expansion into Brazil and Mexico higher growth markets.

As a sanity check, will we get 10% required rate of return at current PE of 22x? Assuming ROIC 19% and IRR 10%, the implied earnings growth rate is ~7%. In the last 10 years, AZO managed to grow earnings by 9.7%.

We think current market cap of $56b remains undervalued and will add to our existing position.