AZO: Autozone (1)

History

AZO was founded by J. R. “Pitt” Hyde III in 1979. Hyde developed AZO as a division of Malone & Hyde, Inc., a Memphis-based wholesale grocery firm founded by his grandfather, J. R. Hyde, and Taylor Malone in 1907.

Hyde was president of Malone & Hyde when he began to diversify the wholesale grocery business with the auto parts stores. He started running the company at the age of 26, when his father became ill in 1968. Hyde was very successful with the wholesale grocer business and tripled its volume after taking Malone & Hyde to the New York Stock Exchange and using the stock to buy other food distributors. In the 1970s, the Federal Trade Commission blocked several acquisitions and Hyde began to look for new businesses to diversify his company. In 1979, he opened his corporation’s first auto parts store in Forrest City, Arkansas.

The auto parts stores began under the name of Auto Shack with an aim to sell an assortment of auto parts and accessories. The goal of the company was to provide a store that provided more self-service than the traditional auto parts shop, with wide aisles, bright lighting, and uniformed workers. To better meet the needs of the customer, the company began to tailor each store’s merchandise based on vehicle statistics in the store’s neighborhood.

In 1987, as a result of an infringement suit by Radio Shack, Auto Shack changed its name to AutoZone. After taking Malone & Hyde private, Hyde sold the company in 1988 to Fleming Companies, based in Oklahoma City. Hyde kept the thriving auto retail store chain that he had spun off prior to selling Malone & Hyde and continued to make improvements in the business. He adopted technologies early in 1989, such as software systems for store management, to keep the stores stocked with needed parts.

In 1991, AZO went public. Further adoption of technology came when AZO began to register customer warranties in a computer database, and in 1994, it started using a satellite system to broadcast information from store to store. The system helped customers search for parts availability in stores. These improvements helped AZO to expand even more; in 1995, AZO opened its 1000ᵗʰ store and introduced new best-selling batteries Duralast.

As the internet arrived in the 1990s, AZO introduced their website and started new commercial programs. It also acquired ALLDATA, a software company providing automotive diagnostic and repair information.

In 1998, AZO acquired 800 stores from other auto parts retailers and later converted many of them into AZO stores. In the same year, the first foreign AZO store was opened in Nuevo Loredo, Mexico.

Currently, AZO operates over 7000 stores in the United States, Mexico, Brazil and Puerto Rico. Pitt Hyde retired in 1997 as chairman of the board and turned his attention to the family’s philanthropy, the Hyde Foundation.

Bill Rhodes became CEO in 2007 and retired recently, writing his last shareholders letter in 2023. Phillip Daniele was appointed as the new CEO in 2024. He worked in AZO for more than 30 years, he started out as a sales manager and worked his way up the ladder, serving various roles along the way.

Today, all AZO stores are corporate owned without franchises.

Industry overview

We find it useful to give a broad picture of the car repair industry in America from the demand and supply side.

On the demand side, we know the following facts:

1. Stagnant growth in new cars sold every year, at about 0.4% per year.

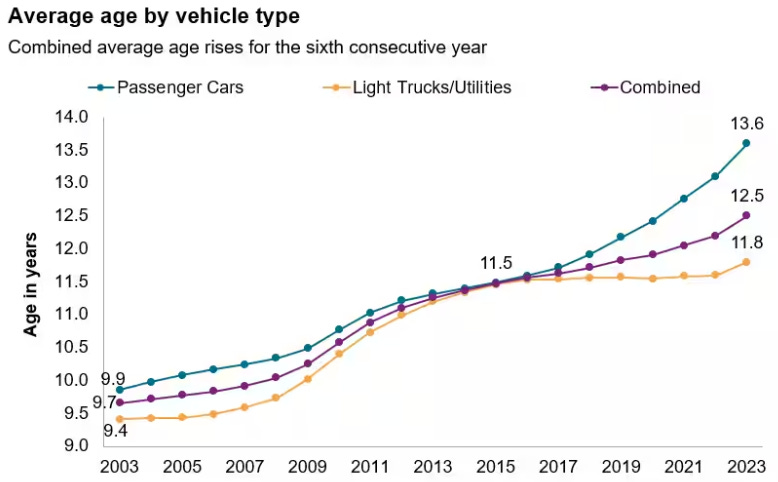

2. Average age of cars increases every year as they are better built. Today, the average age is 12.5 years.

3. Average distance driven grows at about 0.4% per year.

4. Price inflation is about 3% per year.

From these facts we can imply some strong characteristics in this industry:

1. Revenues are very predictable, cars that are addressed by this market are those which are out of warranty, so people have to repair cars themselves.

Stagnant growth in new cars brings more business to the car repair & maintenance industry. Between the years 1980 and 2000, America’s population grew by 13% or about 33 million people. Despite the increase in population over 2 decades, the number of light weight vehicles sold in years 2000 and 2018 (pre-COVID) was unchanged at 17 million.

2. Given the rising average age of cars, the maintenance costs are cumulative with age. For example, suppose a car needs 3 parts to be maintained in the first 5k miles. On the next visit at 10k miles, there could be an additional 3 more parts to maintain, adding up to 6 parts. So there is a compounding effect when cars last longer. Of course there will come a point where this effect drops off for very old cars either through replacement or neglect.

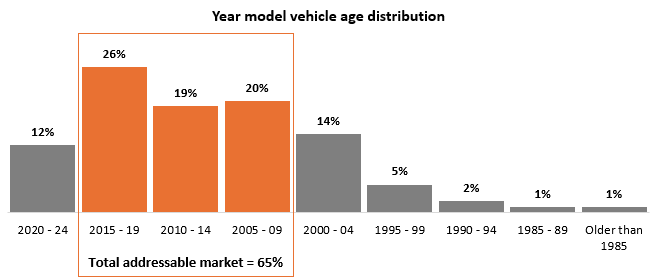

3. Total addressable market growth factoring in inflation would be about low single digits 3-4%. The chart below plots the vehicle model-year and highlights the total addressable market of vehicles between 7 to 14 years old, which sums up to be 65% of vehicles in operation:

Given that there are about 284 million vehicles in operation today, 65% of that is 184 million.

The average American spends about $0.08 per mile driven on repair & maintenance.

Average miles driven per year is about 13,500.

Average cost of repair & maintenance = 0.08 x 13,500 = $1,080 per year.

Addressable market = $1,080 x 184mil cars ≈ $200b

Out of the $200b market, AZO revenues are $17.5b, O’Reilly $15.8b, Advance Auto Parts $11.3b. The 3 major players combined revenues is $44.6b (22% market share). Remainder share goes to fragmented small players.

On the supply side, the 3 major players are quite similar in number of stores and have nationwide presence. Advance Auto Parts have more do-it-for-me business while Autozone is still more do-it-yourself. There’s also small differences in whether they own or lease stores.

Other than these differences, all 3 businesses come with wide margins, high returns on invested capital and very rational industry pricing.

We can also infer some favourable characteristics in the supply side equation:

1. Opportunities for acquisitions and consolidation in a fragmented market.

2. The industry is dominated by 3 large players where there are no incentives to wage price wars as a customer is unlikely to change supplier unless pricing is irrational.

Competitive Advantage #1: Customer Service

AZO business is split 75% do-it-yourself and 25% do-it-for-me services. They have a 30/30 rule which states that employees have to engage a customer within 30 seconds or 30 feet of entering the store.

AZO owns an incredible database of solutions, so they can look up your car through registration or model, and they can find the exact parts you need. Inventory availability is a key competitive advantage, because if you go to a store for a specific part and they don’t have it, you’re not likely to ever go back. Therefore, AZO emphasizes inventory availability, which results in a very low inventory turnover.

Usually you would think that for retailers fast inventory turnover is superior, however in AZO case it is the opposite, because it is important to have the parts in-stock to service customers quickly. This is a major barrier to entry for smaller players who cannot manage large inventories.

On the service side, they provide advisory and will lend tools to the customer free of charge (with deposit) for 72 hours if it’s a complex fix.

The factors of availability, service, locality and technical knowledge database is AZO value proposition to customers.

Competitive Advantage #2: Distribution Network

Firstly, AZO owns all of their distribution network. They do not have dependency on other firms, except for prehaps some third-party transportation to deliver items. All warehouses, hub stores, technology and support centers are wholly owned.

Merchandise is selected and purchased for all stores through AZO store support centers located in Memphis (America), Monterrey (Mexico) and Sao Paulo (Brazil). In 2023, one class of similar products accounted for approximately 14% of total revenues. No other class of similar products accounted for more than 10% total revenues, and no individual vendor provided more than 10% of total purchases.

Most of AZO’s merchandise flows through distribution centers to stores by their fleet of tractors and trailers or by third-party transportation. The distribution centers replenish stores up to multiple times per week depending on store sales volumes.

AZO runs 308 domestic and 39 international hub stores, which have a larger assortment of products as well as regular replenishment items that can be delivered to a store in its network within 24 hours. Hub stores are generally replenished from distribution centers multiple times per week.

Hub stores have increased AZO’s ability to distribute products on a timely basis to many of their stores and to expand product assortment. As a subset of domestic hub stores, AZO runs 98 mega hubs.

Mega hubs work in concert with other hubs to drive customer satisfaction through improved local parts availability and expanded product assortments. A mega hub carries inventory of 80,000 to 110,000 unique SKUs, approximately twice what a hub store carries. Mega hubs provide coverage to both surrounding stores and other hub stores multiple times a day or on an overnight basis. Currently, AZO runs over 6,000 domestic stores with access to mega hub inventory, most of these stores receive mega hub service on same day basis.

AZO has increased its target for mega hubs over time. Initially in 2013, they thought that 25-40 mega hubs would be enough domestically. In 2019, they increased this target range to 70-90. And in 2022, they increased the target to 200 mega hub and over 300 hub stores.

This operational experience and efficiency is another significant barrier to entry.

Competitive Advantage #3: Negative Working Capital

There are 2 ways to drive a high return on invested capital, it’s either having wide margins or having high working capital turnover. Most retailers tend to have low margins and high turnover, however in AZO case the working capital is negative. This unique characteristic is the inverse of the general retail model of “big inventories, sell cheaply, sell quickly”.

Negative working capital is not a disadvantage because AZO is able to negotiate for extended payment terms from suppliers resulting in a high accounts payable. This leveraging of inventory purchases is described below in the 10K:

Certain vendors participate in arrangements with financial institutions whereby they factor their AZO receivables, allowing them to receive early payment from the financial institution on our invoices at a discounted rate. The terms of these agreements are between the vendor and the financial institution. Upon request from the vendor, AZO confirms to the vendor’s financial institution the balances owed to the vendor, the due date and agree to waive any right of offset to the confirmed balances.

2023 10K, pg 33

On the current assets side, there is low levels of receivables obviously because most customers pay upfront at the stores. Most receivables are owed by commercial customers. It is quite rare to find retailers that can operate successfully with negative working capital.

For the curious reader: Amazon consumer-to-consumer segment also operates with negative working capital. Amazon sells online and receives payments immediately but keeps inventories on 60 days payment terms to suppliers. So they don’t need to fork out cash to finance growth – the suppliers effectively do it for them.

Competitive Advantage #4: Strong Unit Economics

To calculate the ROI per store, we assumed that the full amount of capital expenditure (CAPEX) spent each year is for opening up new stores (this is a conservative measure since we are ignoring maintenance CAPEX for existing stores). In 2023, AZO opened 197 new stores while spending $770m CAPEX, that means each store incurred $3.9m of cash outlay.

Applying operating margin of 17% on $2.4m of sales per store, we get operating income of about $0.4m.

ROI per store = 0.4/3.9 = 10.3%.

This is a very good number for first year ROI. Furthermore, this is a single year calculation of ROI, in reality as the store ages, customer count increases while the fixed cost of building the store does not change. There will be maintenance CAPEX, but we do not think it outpaces the growth in sales over time. This is another feature of compounding on the returns from the asset base they build out. As the company continues to operate and expand, this creates some form of barriers to entry to smaller players trying to compete at this high level of ROI.

Capital Allocation

AZO repurchases their shares aggressively, since 1997 the management has bought back at least 84% of shares outstanding. It pays no dividends.

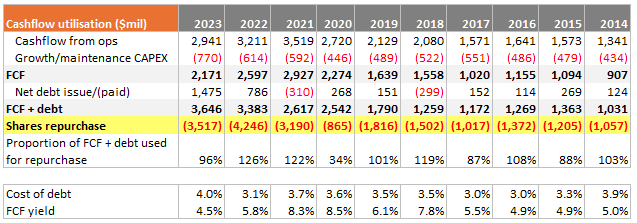

If we breakdown the use of free cashflows (FCF), we can see that cash used for shares repurchase is often almost all or even more than cash generated from FCF and debt issuance. A simple way to ask if this is rational is to look at the cost of debt compared to FCF yield: if the cost of debt is lower than their FCF yield, then it actually makes sense to use debt to repurchase shares because the business can generate more yield than it cost to service the debt.

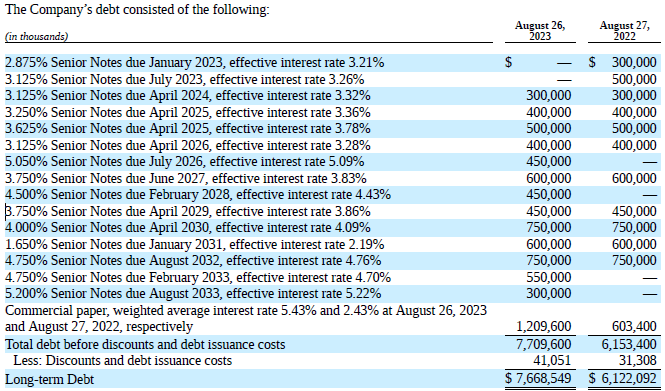

Below shows the indebtedness of AZO, the cost of debt of these notes are still below historical FCF yields:

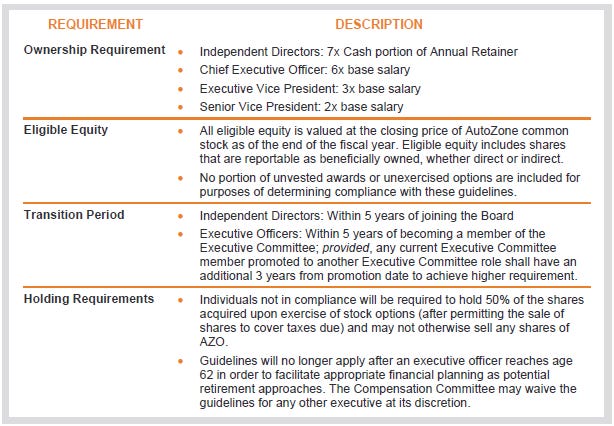

Compensation Structure

The metrics that drive executives’ compensation are:

Earnings before interest and taxes defined as net income plus interest and taxes.

Return on Invested Capital defined as after-tax operating profit (excluding rent) divided by average invested capital (which includes a factor to consider operating leases as financing leases).

Economic Profit is calculated as net operating profit (including rent) after taxes, less the cost of capital using a capital charge rate of 10.5%.

We contend with ROIC as a metric in compensation because this number can be “manipulated” by repurchasing shares even when it is not economically wise to do so.

There are requirements for executives to have ownership in the company:

The cumulative ownership of all current directors and executive officers as a group is 2.5%, majority of it comes from option awards and not out-of-pocket purchases.

Risk #1: Electric vehicles

Electric vehicles (EVs) are often cited as the bear case to AZO business given that EVs don’t have parts of a traditional car.

However, AZO services cars that are 7+ years old. Today, EVs do not take a majority share in new car purchases, which means that only the small portion will generate less revenues after 7 years. The remainder share of traditional cars will continue to be in favor of AZO’s business.

Furthermore, the predictability of the addressable market for the group of cars that are already 7+ years old is independent of EVs penetration. Unless we make an extreme assumption that the majority of old cars will be replaced by EVs. Today, about 1 million new EVs are sold out of a total of 16 million (~6% share).

We actually hope that the market downplays AZO due to concerns over EV penetration, because this would keep the valuation low and encourages value accretive shares repurchases.

Risk #2: Competition from online retailers

Amazon and other online retailers can provide fast delivery of car parts while offering lower prices than AZO. This is not a new business risk. However, there are limitations to this risk:

1. Not every item can be delivered, for example, items that are considered fire hazards (engine oil, brake fluid, batteries).

2. Problem of possible bad quality control. Nobody wants to risk brake pads that don’t function well?

3. Lack of advisory and technical knowledge on how to use the products.

The high margins captured by AZO tell us that customers are going back to their stores not purely because of price alone, there are other qualitative factors that defend the profits of AZO and the industry as a whole.

Other factors to consider

Commercial Segment Growth Prospects

The new CEO Phillip Daniele, in recent Q2 2024 earnings call, emphasized the source of growth to come from the Commercial segment. This segment sells after-market and OEM (Original Equipment Manufacturer) parts to local repair shops, garages and dealers. AZO uses its advantage in distribution networks to deliver parts quickly and efficiently, and this is a high value proposition for local repair shops.

Imagine you are a small car repair shop owner: one of the ways you can get more sales is simply to ensure that the mechanics working on cars have the parts they need on demand. After they finish one repair, the space can be used for the next car. Turn-around time is a crucial driver of revenues.

We do expect that growth in the after-market commercial segment can offset the issue of low organic growth rates.

Above Average Sales per Employee

AZO has the highest sales per employee amongst the other two major competitors (Advance Auto Parts, O’Reilly). The revenue per employee at AZO is over $200,000 while competitors come in at a significant difference of around $160,000 to $180,000.

We put this statistic out because for retailers, outstanding production and sales may be considered important drivers of high return on investment and generally success. An efficient distribution system, together with strong salesforce, creates a wonderful retail business.

Rational Pricing

Car parts improve with technology all the time. In the past, spark plugs were made of copper and lasted 30,000 miles. Today, they are made of iridium and last 100,000 miles, or 3.3x longer. However, the prices of spark plugs grew from $0.60 to over $10, or 17x more. Although the unit volume shrinks over time but the cost increase is passed onto the customer.

There is no rational need for the industry players to cut prices for market share because when parts take longer to replace, it results in lower quantities purchased. Since revenues are a multiplicative function of price and quantity, it does not make sense to engage in price wars.

Private Label

Private label is a unique situation for AZO because it contributes to more than 50% of total revenues. Duralast is the most well-known brand, accounting for more than 50% of hard parts sales, but the company also has ProElite, Shop Pro, SureBilt, TotalPro and others.

Duralast has gained a bit of brand equity over the years and the company has been able to offer brand extensions for brake pads, chassis, shocks and struts.

Tailwind Aging Vehicles

In Jan 2024, the US vehicles in operation count was 286 million, up 2 million over 2023, but the distribution of vehicles by age is changing. Vehicles under the age of 6 accounted for 35% (98m) of vehicles in 2019. Today, they represent less than 31% (90m) of vehicles and are not expected to reach that threshold again until 2028, when they will represent about 30% (according to S&P Global Mobility estimates).

As a result, the primary driver growth will be vehicles 6 to 14 years of age, that are expected to represent about 70% of vehicles for the next five years, which will serve as a tailwind to AZO.

International Expansion

Internationally, AZO sees ample opportunities in Mexico and Brazil as well as in other new markets. AZO has been in business in Mexico for over 20 years and the playbook is very similar to that of the US. The car age is a bit older in Mexico, many of which are US cars. The profitability and return profile of the Mexico operations have not recently been disclosed.

Brazil has been slower and the company is still losing money there. The car profile in Brazil is comprised of smaller cars with much smaller engines. AZO estimates that Brazil can account for over 1k stores at maturity.

International expansion will contribute more to growth in the future as the company builds out its network of stores in Mexico and Brazil. It still remains to be seen if they will return similar economics to that of the US, but we should be able to see the result of all the investments over the next few years. Further expansion into the rest of South America could be an option for the company in the future. Canada also remains an option as its car profile similar.

Playbook Copying

What’s great about AZO position in the industry is that there is a playbook that the company can easily follow. O’Reilly has taken the lead in heavily investing in distribution capabilities, including the hub and mega hub model.

O’Reilly calls them super hubs. Even though AZO is a few years behind in terms of infrastructure and distribution capacity, they’re still able to take ample share in the commercial market. Some of that has to do with AZO leveraging its already well established DIY business and private label brands. But it does seem like these two companies can both take market share because auto parts retail still remains very fragmented.

Valuation

We will outline the approach briefly here, details can be found in the worksheet download above.

Bottom up approach by estimating the number of operating stores in the future. Assume each year 194 new stores are opened.

Grow net sales per store by 1.9%, half of the total addressable market growth including inflation.

Set margins at average 10 year historical ratios.

Assume debt on balance sheet to grow at 6.6% (10 year historical), and cost of debt at 4% .

Share repurchases to continue at -4.6% (half the rate compared to last 10 years).

Net income to free cashflow conversion of about 103% (average last 10 years).

Discount rate 10%, terminal growth rate 2.5%

The intrinsic value after net of debt and cash is about $55.8b. Current market cap is $51.9b, we have about 7% discount to valuation.

Conclusion

We think that at current market cap of $51.9b, it is attractive to start accumulating shares in tranches given the competitive advantages and valuation highlighted above