ATCO.ST: Atlas Copco

Intro

In 2023, the present day Atlas Copco celebrated its 180 years history as an continually operating business since 1873. Only a few rare companies can last more than 100 years, in the US there are only about 1,000 companies that have survived for more than a century. Japan has the highest concentration, counting over 21,000 companies older than 100 years.

By contrast, we could only count less than 10 original companies in Sweden, including Atlas Copco, that is older than 100 years which are still operating. Fun fact: Sveriges Riksbank established in 1668 came from Sweden and is also the world’s oldest central bank.

Even though it is the third largest listed company in Sweden, many people know about famous companies from Sweden like Spotify or IKEA, but not Atlas Copco because it’s an engineering company that’s entirely B2B.

Indulge us with the long and interesting story telling of Atlas Copco history and business breakdown…

History

Railway Origins

Today, Atlas Copco sells mission-critical industrial products and services all over the world, supporting customers in 180 countries.

However, when it was first founded in 1873, Atlas only made products for Sweden’s railways. Nothing more, nothing less.

The railway was a beacon of technological innovation for its time. It changed societies everywhere, and in few countries with such force as in the geographically extended Sweden.

One person who saw the business upside was André Oscar Wallenberg, founder of Stockholms Enskilda Bank (today’s bank group SEB). He noticed that the equipment used to build and maintain railway systems had to be imported, primarily from the UK and Germany.

Surely a Swedish company should be able to make those instead?

So Wallenberg ventured ahead, together with three partners, founded a company to make railroad equipment. They named it Atlas, after the Titan in Greek mythology, who carries the skies on his shoulders.

Atlas built workshops in central Stockholm and in just two years it became Sweden’s largest engineering company. Engineer Eduard Fränckel was the first CEO put in charge, and they had the state-owned Swedish Rail as their largest customer.

For a few years, everything looked promising for the young company until a recession hit Sweden in the 1880s, bringing railroad construction to a halt and Atlas was in financial stress.

There was a change in leadership, Fränckel was succeeded by industrialist Oskar Lamm. New capital was injected from the Wallenberg family and the company changed its name to Nya Atlas (New Atlas). Production shifted to more advanced products, such as steam engines and boilers.

Changing with Times

The company reacted and adapted to new times, but to make the new products, they needed new types of tools. So, in the early 1890s, a young Atlas engineer named Gustaf Ryd went shopping in England and the USA. He bought a pneumatic caulking hammer, an air pump, and a riveting hammer.

It didn’t take Atlas’ engineers long to figure out how to build these new tools themselves. At first, they made them just for internal use. Soon, word of their efficiency spread, and Atlas started selling them externally.

By 1901, a whole new business area had spawned from this, making pneumatic and compressed air products. To this day, this is a core area for the company.

The Wallenberg family had other business interests than just railroads. In the late 1890s, they struck a deal with German engineer Rudolf Diesel, who named his diesel engine invention after himself. The deal gave Sweden manufacturing rights, and they formed the company Diesels Motorer. The company ended up not just producing diesel engines but also improving their design.

With Nya Atlas and Diesels Motorer sharing the same owner, it was not long after that the companies merged in 1917 to become Atlas Diesel.

At this time, WW1 broke out and was actually good business for Atlas Diesel, since most of their production had export demand. Atlas Diesel moved production of air compressor tools to Sickla, just outside of Stockholm. All production was now there, in a plot once bought for Diesels Motorer. Today, this is still the site for the company’s headquarters.

However, ravages of the Great Depression followed by World War 2 did not spare Atlas from the brink of bankruptcy, not just once, but twice. The Wallenbergs came in again to financially restore Atlas in 1925 and 1934.

How Atlas Copco got its Name

After WW2, Walther Wehtje, a previous department store manager, was now President and CEO and led the company in a more sales-focused direction. They stopped making the less profitable diesel engines and focused on pneumatic tools, compressors and drilling equipment. To improve their engineering expertise, Walther went on to acquire other engineering companies, starting in Sweden then later expanding overseas.

The first important international acquisition was the Belgian compressor company Arpic Engineering in 1956, moving most of the compressor production over to Belgium. This was also when the name was changed from Atlas Diesel to the modern day Atlas Copco. The word “Copco” is actually an acronym of a Belgian sales subsidiary in French “Compagnie Pneumatique Commerciale”.

Another interesting story from Australia was during an archeological dig in the 1980s, Atlas had lent equipment to the excavations and the paleontologist named one of the new species Atlascopcosaurus loadsi. The term “loadsi” was named after Bill Loads (Atlas Copco’s manager in Victoria who was personally involved in the project).

Atlas Copco continued to grow internationally, both through acquisitions and inventive new processes. One such innovation was “The Swedish Method” for drilling which allowed one person to operate a drilling machine where previously many people were needed. This method revolutionized the drilling industry and laid the foundation for international expansion.

Another growth area was compressor technology which would become the crown jewel of Atlas today. People found many uses for air compressors, from inflating things, supplying power for drills, to industrial applications like spraying crops.

More Acquisitions

Then came the oil crisis of the early 1970s and the following global recession. Atlas had to restructure internally and lay off workers, but at the same time, the crisis also opened up for strategic acquisitions. One such important purchase was French air compressor company Maugière, it is still a subsidiary of Atlas today.

The M&A efforts led Atlas into the US market and during the early 1980s, it bought Worthington Compressors. By then, Atlas was the world leader in rock drilling and pneumatics. Seeing the potential in industrial tools, they purchased Chicago Pneumatic Tools in 1987, which opened up the important American, French and British markets.

Atlas then became one of the world’s largest manufacturers of pneumatic tools and monitoring systems. At the end of the 1980s the company’s geographical foothold grew and product assortments expanded. In 1990, the British company Desoutter Brothers Plc. that supplied industrial tools and monitoring systems was purchased. In 1992, AEG Elektrowerkzeuge was purchased and in 1995 Milwaukee Electric Tool was acquired, which was later sold to Techtronic Industries Company.

In 1997, Atlas Copco made its biggest and most important acquisition with the purchasing of the Prime Service Corporation, which was the largest machine leasing company in the US.

The new millennium saw continued M&A with two key companies Edwards Group (UK) and Oerlikon Leybold Vacuum (Germany) which gave rise to the Vacuum Technique segment we see today.

Fast forward to recent times, in 2019, Atlas acquired 18 companies which was a record in any year. Then in 2022, they did even more with 30 acquisitions. Last year, in 2024, the trend continues with 34 acquisitions!

Global Presence

China first saw Atlas products back in the 1920s but it wasn’t until 1983 when they signed its first license agreement with a compressor factory in Wuxi. Two years later, Atlas opened its own representative office in Beijing. In March 1993, Atlas entered its first joint venture with Nanjing Construction Machinery Plant to manufacture and sell drilling rigs.

China has become one of the largest markets for oil-free compressors. In 2024, Asia/Oceania contributed 31% of total revenues. Just slightly lower than North and South America combined of 32%.

In 1960, Atlas first opened a sales office in India after many years of selling through an agent. Two years later, it opened a factory and became a significant supplier. In the 1970s, the Indian government passed a law in the 1970s mandating that all foreign companies must have majority Indian ownership. This caused many international companies to leave India. But Atlas remained and even with Indian owners, they managed to continue the corporate culture of innovation and customer obsession.

Willingness to Divest

Mining equipment was a key part of Atlas portfolio, way back in 1905 it had already begun producing rock drills named Cyklop was a lightweight handheld drill that continued into the 1930s. When the Mont Blanc tunnel opened in 1965, it was the world’s longest car tunnel (11.6km long, 8.6m wide). The tunnel was drilled from two directions, from France and Italy, Atlas drilling machines were used on the Italian side and workers reached the middle of the tunnel on August 3, 1962, a few days before their French counterparts.

So it came as a surprise that in 2017, Atlas announced a spin-off from its mining equipment business, stating that Atlas will focus on industrial customers and not mining, infrastructure and natural resources. The new company was Epiroc, and has since been a fully independent company with its own stock publicly listed.

Before splitting up, the mining & rock excavation segment grew revenues from SEK20.2b to SEK29.2b over a 8 year period, a modest 4.7% CAGR. Operating margins averaged 20.3%. So it wasn’t a bad business, and the split was supposed to allow Epiroc more focus and agility to innovate.

Post spin-off the results of Epiroc was impressive, from 2018 to 2024 it grew revenues by CAGR 8.9% with EBIT margins of 19% in 2024.

It is believed that the spin-off was not to realize short-term market valuation gains since Atlas had no ownership stake in Epiroc. Rather, it was done because management thought that the combined entity was getting too big and bureaucratic.

This decision points to the long-term value sensitive thinking of management for the benefit of the business and not to appease any shareholders.

Business Segments

Before we dive into the segments, there’s one thing we need to know; Atlas sells productivity.

All their customers are businesses, and they obsessed with maximizing productivity.

Why so?

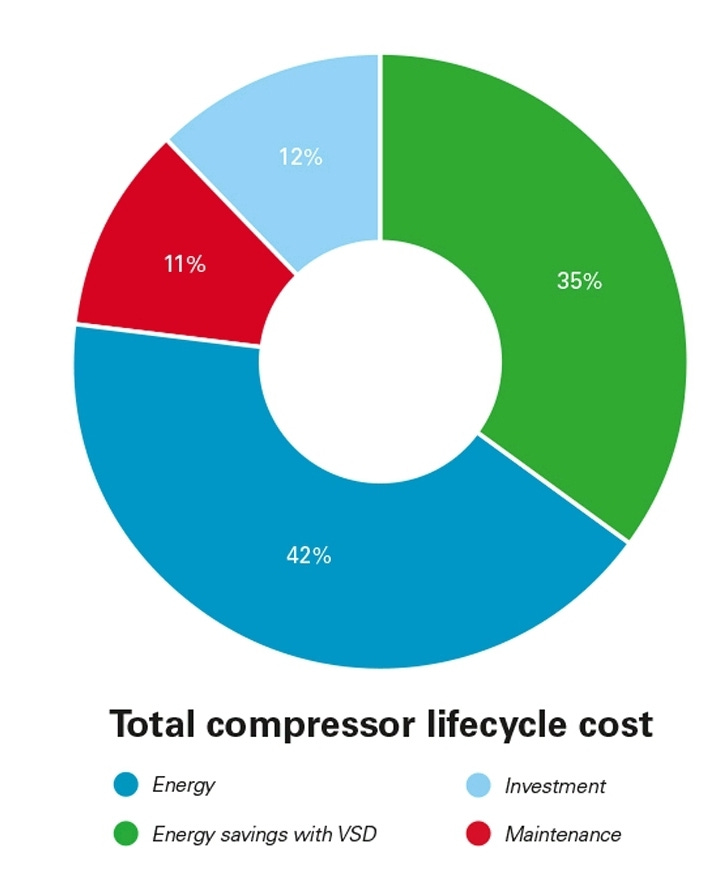

In industrials, when we think about an equipment’s total cost of ownership (TCO), most of the cost comes from energy and operations over the lifetime of the equipment. The actual equipment cost outlay is small in the scope of TCO.

For example, 80% of the TCO is coming from energy powering that compressor. If you have a compressor that is 5% more energy efficient, over a 10 year life cycle, that is what customers really focus on:

Interested readers can check out their annual reports where they list out the innovations by segment every year. Obviously, we don’t know what the scientific details mean, but we are satisfied to read that every innovation is described to “improve efficiency and lower energy consumption”.

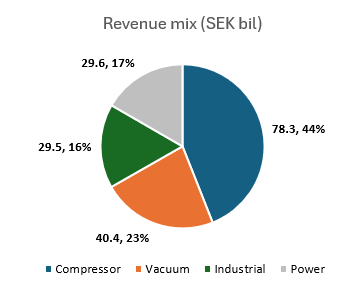

Atlas splits the business into 4 segments with revenues and operating margins in 2024:

Compressor Technique (SEK80b, 25.2%)

Vacuum Technique (SEK36.6b, 21.1%)

Industrial Technique (SEK29.5b, 20.5%)

Power Technique (SEK29.6b, 18.5%)

As a group Atlas operates comfortably at above 20% margins. Equipment sales still contributes a large 63% of revenues, while services make up the remainder 37%.

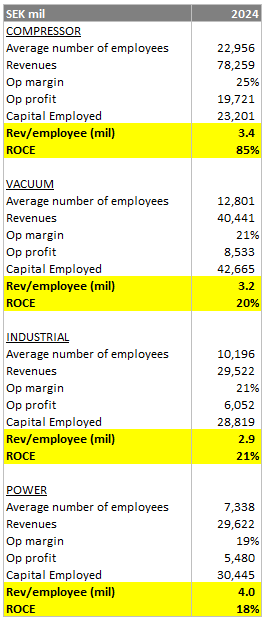

Below are the unit economics by segment:

Compressor Technique

Atlas first got into the compressor market in 1904 when it started making piston compressors. Since then, this segment is the most profitable and Atlas intents to keep innovating and delivering productivity to customers.

Today, compressor technology is led by Guy Mareels (VP Engineering, Oil-Free Air Division) who joined 16 years ago, starting out as an engineer running simulations.

Atlas has repeatedly made breakthroughs in oil-free air compressors since the first oil-free series in the 1960s. They are now making another leap in energy efficiency with a new generation of oil-free screw compressors.

This segment closed 17 acquisitions in 2024:

Ace Air (NI) Ltd

Hycomp Inc

Druckluft-Technik-Nord

Pacific Sales & Service Inc

Zahroof Valves Inc

Tecturbo

Baraghini Compressori S.r.l.

AE Industrial Ltd

Emcovele S.A.

Kingsdown Compressed Air Systems Ltd

Compressed Air Technologies Inc

Danmil A/S

Easy Filtration S.r.l.

Arlógica Máquinas e Equipamentos

Pennine Pneumatic Services Ltd

SCS Makina A.Ş

Metalplan Equipamentos LTDA

Atlas reports Compressor ROCE to be 85%, which is very impressive!

Definition: Capital Employed = Average total assets, less non-interest-bearing liabilities, less cash & tax liabilities/receivables.

Almost every industrial process requires a compressor, and there’s no substitute for it. The compressor is such a rudimentary component of power generation that it is sometimes called the fourth utility after electricity, gas and petrol.

Oil free compressors are those that don’t use oil as a lubricant for moving parts. Most crucial benefits are higher air purity and lower maintenance cost.

In terms of market share, it’s estimated that Atlas has 30% global share, which is at least twice as large as the next competitor Ingersoll Rand. This shows the market is still fragmented and there’s room for further consolidation.

Vacuum Technique

To over-simplify, vacuum is just the opposite of a compressor, it sucks in air while the other blows out air.

The first vacuum pump was invented in 1649 by Otto von Guericke, but it would take 250 years until the potential of this technology could be realized. At the turn of the 1900s, humanity transitioned from candles to light bulbs, and vacuum pumps had a key role to play. It was the German company Leybold which offered one of the first air pumps in 1899, it was eventually acquired by Atlas in 2015 for €486m.

Atlas has been building this segment through the 2000s. It’s been very acquisitive over many years now, noticing trends towards increasing uses and applications for vacuum pumps. In particular, dry pumps are required in making semiconductors.

These vacuum pumps are exposed to the semiconductor markets because you need a clean environment to fabricate chips. As the world demands more high-performance chips, wafer fabrication will require higher purity.

Vacuum pumps are essential for creating the necessary vacuum in deposition and etching chambers. By avoiding contamination and reaction with atmospheric air, they guarantee the quality of semiconductor manufacturing at nano scales.

Furthermore, photolithography machines use plenty of toxic materials and generate lots of waste products, without an advanced dry pump fabs risk damaging these very expensive machines.

The economics goes back to the productivity concept; vacuum pumps are a fraction of setup cost but are a large proportion of energy savings in terms of TCO.

Atlas is the largest player in the vacuum pump market, much bigger than the next competitor Pfeiffer Vacuum. Opportunities are mostly in APAC, estimated 47% revenue share in 2022.

This segment closed 5 acquisitions in 2024:

Presys Co, a manufacturer of vacuum valves for the semiconductor market based in South Korea.

Montajes Electromecánicos e Ingeniería, provides vacuum pumps and related services to industrial customers in Mexico.

AVT Services, a company providing vacuum pumps and system sales, and service to customers in Australia.

Anhui NOY Technologies Co. Ltd., a Chinese helium leak detector manufacturer.

ESA Service S.r.l, an Italian company designing and manufacturing leak detection and gas recovery systems.

Industrial Technique

In the 1960s, engineers at Atlas began exploring the potential of using electricity as a source of powering tools. After decades of R&D, a completely new design principle was invented by a team led by Christer Hansson. Their work culminated in the first generation of the Tensor nutrunner in 1987, followed by the second version, Tensor S in 1993.

The Tensor family of tools gave Atlas market leadership in the automotive industry, it provided precise and reliable assembly processes. For example, it gives accurate torque and angle control, data collection, error solutioning etc.

Today, the automotive manufacturing process is a smart factory. Productivity is the key to lowering cost for car manufacturers. We circle back to the same principle: Atlas sells productivity.

This segment closed 4 acquisitions in 2024:

Swed-Weld AB, a Swedish provider of smart automated screw and nut feeding systems with focus on the automotive industry.

Mont-Tech, a Czech engineering company offering customized engineering solutions for assembly automation.

Air Way Automation, a US supplier of automated bolt feeding solutions to the automotive and general industries.

VisionTools Bildanalyse Systeme, a German company that develops and sells integrated solutions for quality control in assembly lines.

Power Technique

Organizationally, the Power Technique segment was only born in 2017 after the company restructured its Construction Technique segment following Epiroc spin-off. However, Power segment has century-old roots going back to both compressor and mining businesses. The segment is now centered around air (portable compressors), power (generators) and flow (pumps), along with related products such as light towers and services, including equipment rental.

The majority of applications for products in the Power segment are in remote locations where access to electricity is limited. In the past, diesel was the source of powering portable compressors, generators and pumps. But the energy efficiency was low.

Atlas started with HVO (hydrotreated vegetable oil) and recently invented a series of lithium-ion energy storage systems called ZenergiZe in 2020, launching the TwinPower generator series. This innovation provides up to 40% lower fuel consumption and 80% lower emissions.

This segment closed 7 acquisitions in 2024:

KRACHT, a German manufacturer of external gear pumps, fluid measurement, valves, hydraulic drives, and dosing systems.

Delta Temp, a Belgian company that provides specialty rental solutions for industrial cooling applications.

Generator Rental Services, a company in New Zealand providing specialty power rental solutions.

Integrated Pump Rental, a specialty rental provider of dewatering solutions in South Africa.

Pomac BV, a Dutch company which develops and manufactures hygienic pumps.

Kinder-Janes Engineers Ltd, an industrial pump distributor in UK.

Perslucht Wilda BV, a compressor distributor in Netherlands.

Ownership & Incentives

Since Atlas was founded in 1873, it has been managed by 13 CEOs. That’s an average tenure of 12 years.

Currently, Vagner Rego is the CEO, taking over Mats Rahmström, who held the position from 2017 to 2024. Vagner has been with Atlas since 1996, starting as a trainee engineer in Brazil. He owns 28,179 Class A shares and 412,096 stock options, assuming everything is vested his ownership is worth SEK69m (US$7.3m). This is not a large multiple of his base salary of SEK10.7m plus bonus of SEK7.7m.

Peter Wallenberg Jr is the only member of the Wallenberg family on the Board, he has 666,668 Class A shares worth SEK105m (US$11m).

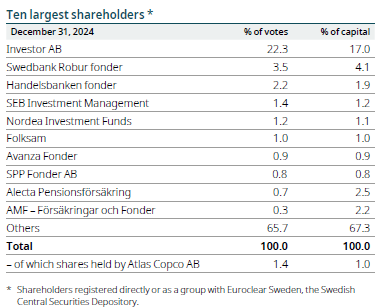

As mentioned in the history section, the Wallenberg family has been involved with the company since the beginning. Today, it is still the largest shareholder, their stake comes from Investor AB through the dual class shares with 22.3% voting rights and 17% economic rights:

Investor AB in turn is mainly owned by the Wallenberg Foundations.

We could go all the way back to the 1850s when André Oscar Wallenberg founded the Stockholm Enskilda Bank, which is now known as SEB. Till this day they still have 1.2% economic interest.

M&A

If there was a defining decade in Atlas Copco’s long history, it would be the restructuring done back in the 1990s. They adopted a decentralized conglomerate approach, then they ramped up the M&A consolidation strategy, growing the air compressors business and then expanding overseas. By the late 1990s, foreign revenues was 80% of total.

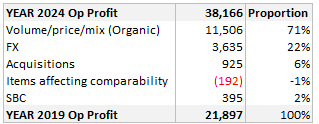

Below is the operating profit bridge between 2019 and 2024, separated by organic, acquisitions and FX impacts:

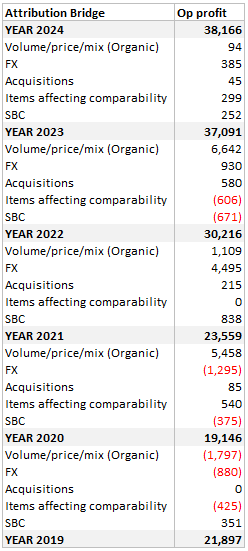

The attribution for the difference in operating profit is mainly organic growth and FX benefits. Incremental acquisitions contributed 6%. Since M&A gets reclassified into Organic as years progress, it is useful to see the year-by-year attribution bridge:

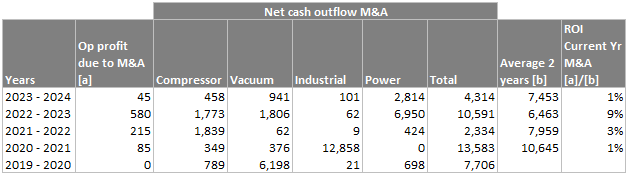

To work out the immediate next year’s ROI of these acquisitions, we use these reported figures:

Note: This is only measuring the following year’s M&A contribution against the cash spent. Obviously, an older acquisition will become categorized as “organic” after 1 year and we cannot measure over the lifetime of these M&A. The better way to check is to refer to ROIC in the next section.

M&A a sustainable strategy as long as fragmented markets exist across their products. They are usually small bolt-on acquisitions (average spend of SEK393m or US$36m) and the odd large one. They are also buying businesses with lower margin profiles where there are willing sellers in tougher times.

Valuation

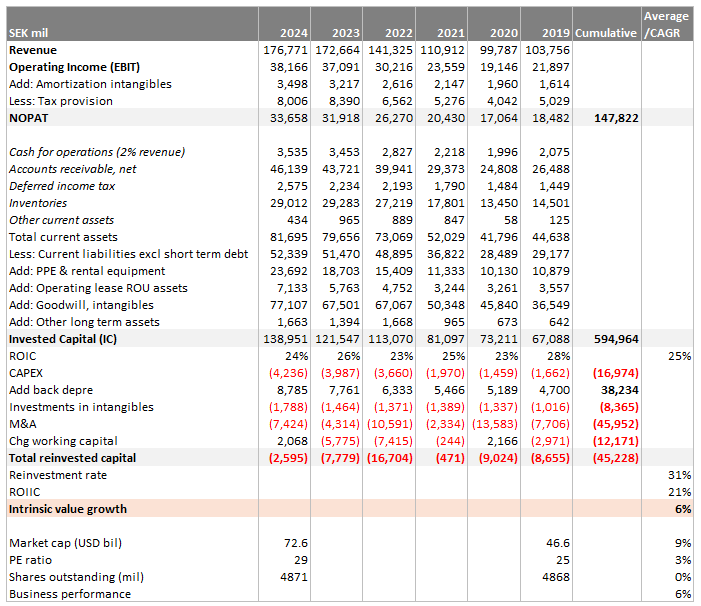

First, we want to sense check management’s calculate of ROCE. We independently estimate the ROIC over the last 6 years at 25%. Both measures are not exactly equal but should directionally point to above 20% rates.

Atlas market cap grew by 9% CAGR, of which 3% was due to multiple expansion. So the underlying business only grew at 6% CAGR.

To breakdown this growth we can estimate the intrinsic value growth by the reinvestment rate and ROIIC. Although ROIIC is quite good at 21%, the reinvestment rate is only 31%. Not surprisingly, all of the reinvested capital was used in M&A.

Currently, the stock trades at PE 24x, if we want IRR = 12.5% with ROIC = 25%, the implied growth rate = 10%.

Lowering the IRR = 10%, the implied growth rate = 7%.

Compared to a historical performance of 6%, we don’t think there’s good value here.

There’s a few reasons why margins might be on a cyclical high now:

R&D expenses have increased from 2% of revenues in 2014 to 4% in 2024, the margin expansion since 2020 was due to price/mix/volume.

We are not sure if volumes can continue to keep increasing at the end markets. Volumes have generally been the primary driver of margin expansion via higher throughput over its fixed manufacturing lines. As volumes slow, margins generally fall.

Atlas has benefited from a rising USD (revenue) and weaker Euro (costs). These benefits are subsiding and could become a headwind.