APH: Amphenol

History

Amphenol (APH) was founded in 1932, manufacturing tube sockets for vacuum tube radios. The company IPO in 1957, and was merged with Bunker Ramo Corporation 10 years later. Then, in 1981, AlliedSignal purchased Bunker Ramo Corporation which is now part of Honeywell group.

AlliedSignal then sold APH for $430m to LPL Investment, who IPO the company again in 1991. With 30% of shares under its ownership, LPL backed the $1.5b sale of 75% of APH to KKR, who reduced their stake to less 49% three years later before exiting completely in 2004.

After the dotcom bust, APH sales were affected due to their high proportion of exposure in the sector. As a result, APH learned the lesson and made an effort to diversify its end markets and products.

APH stock has returned more than 35x over the last 20 years. A closer look at what APH is doing might make an investor impressed by how this stellar result was achieved. APH basically is a manufacturer for selling connectors, sensors, and antenna solutions.

Another more impressive result is how much APH has outperformed their closest competitors for the past 20 years despite operating in a highly commoditized and competitive environment. TE Connectivity (TEL) is the closest and largest competitor, its shares only grew 4x since 2004. Aptiv, the Irish-American automobile tech supplier grew 6x over the same period.

What are connectors?

Connectors, or “interconnects”, come in a wide variety of shapes and sizes, and carry strange technical labels, but we can basically think of them as the things we find at the end of electric and fiber optic cables and the ports that those things plug into. Terence Curtin, CEO of TE Connectivity, once put it:

When you think about what we do, the semiconductor is the brain of the applications we’re in. You might have a power supply that’s the heart. I say what we do are the arms and the legs to really make sure how you get the connection of the different modules and inputs together.

We can infer that although the connectors are immaterial from a cost perspective to the end products, it is mission critical for the proper functioning of all electronic devices.

Connectors are important but forgettable. After considering the features and capabilities of a system, an OEM will call upon APH to make connectors. Over the years, APH has expanded the product portfolio to include antennas (akin to a connector for radio waves) and sensors. The sensor business came through acquisitions on the back of its $318m purchase of GE’s orphaned sensor division in 2013.

Who buys APH products?

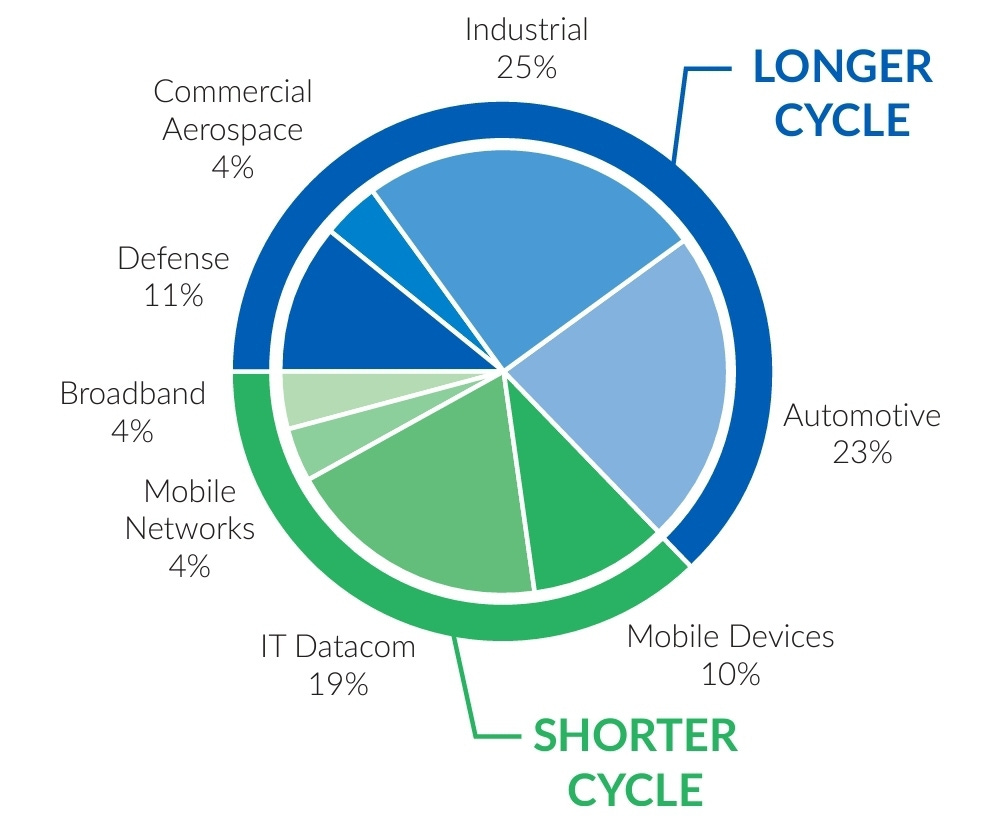

The end market looks like this:

The rationale for this diversification is because APH operates in a cyclical industry. For example, automotive, industrial and aerospace have a longer cycle while IT and data communications have a shorter cycle due to their fast moving innovation pace. The mixture of long and short cycles should act as a hedge against cyclicality.

APH products are critical components that make up a small fraction of the material cost for complex electronic systems. They can be found everywhere, if a system receives or transfers power or signals, it most likely has connectors. APH sells a large number of SKUs to customers, who embed those connectors into an even larger number of modules. Upon being qualified into a system, APH enjoys the benefits of a sticky supplier.

Industry Characteristics

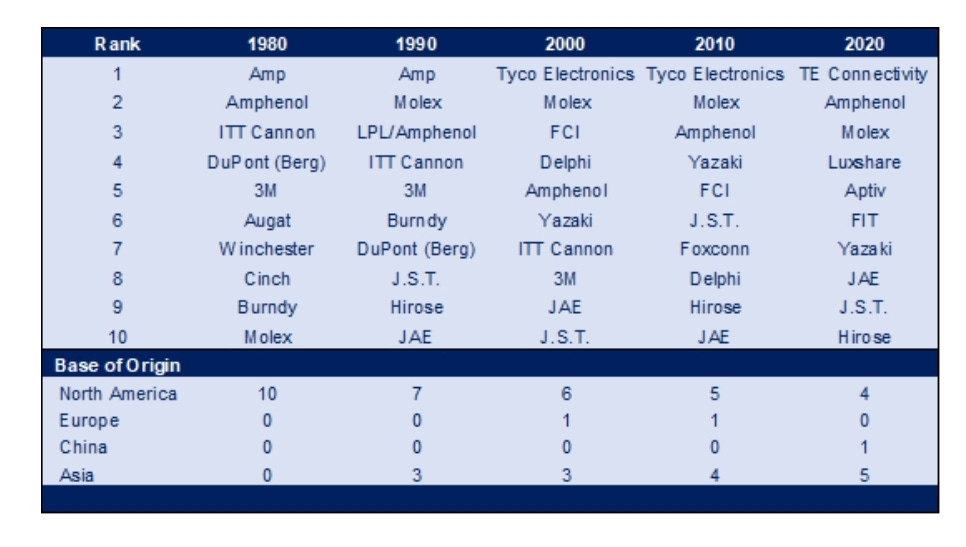

Below is the market share of top 10 players within the industry since 1980:

The connector industry is certainly highly fragmented as it encompasses thousands of players. From the table above, the obvious trend is that the industry is becoming more consolidated over time.

The top 10 companies in the industry gained market share from 38% to 61%. This trend is believed to continue for the foreseeable future, meaning that M&A plays an important role for companies gain dominance in the industry.

Below table shows the competitive nature of the connector industry:

Many industry leaders in the 1980s didn’t make it in 2020 either due to M&A or bankruptcy. It is not surprising that the newcomers that are replacing the incumbents are mostly from Asia, which are known for their highly competitive pricing and quality:

Total Addressable Market (TAM)

TAM is about $220b (connectors $85b + sensors $135b), implying APH revenues of $12.5b in 2023 is only 5.7%.

The reason for a small market share is due to the large array of end markets. Each industry vertical is different but in general most are fragmented. The top 20 companies can account for as much as 88% of a market such as automotive, but as little as 58% in aerospace & defense. APH highest market share is in aerospace & defense at 34%, but it only has 2% of the consumer and automotive verticals.

Main reasons are sticky suppliers, regulatory requirements and industry-wide competition. Certain verticals require certifications, and once a company is considered a qualified supplier, they tend to be sticky.

There seems to be exciting potential growth of the connector industry, due to datacenters, wearable technologies, car sensors are gaining traction very quickly. As a result, as long as there are more connections, there will be more connectors to be sold. A good example will be the number of connected devices growing 16% to $16.7b globally in 2023 with a forecast of $29.7b by 2027.

In the sensors segment, APH realised that there is more integration between sensors and interconnect products as their business evolved. As a result, APH entered the business in 2013 so that they could collaborate or cross-sell into different markets. It will also further strengthen their relationship with customers due to the increase in penetration of content per customer.

Being a latecomer in the sensors market, APH has been capturing market share through acquisitions. They just completed their #9 sensor company acquisition in 2022.

Business Model

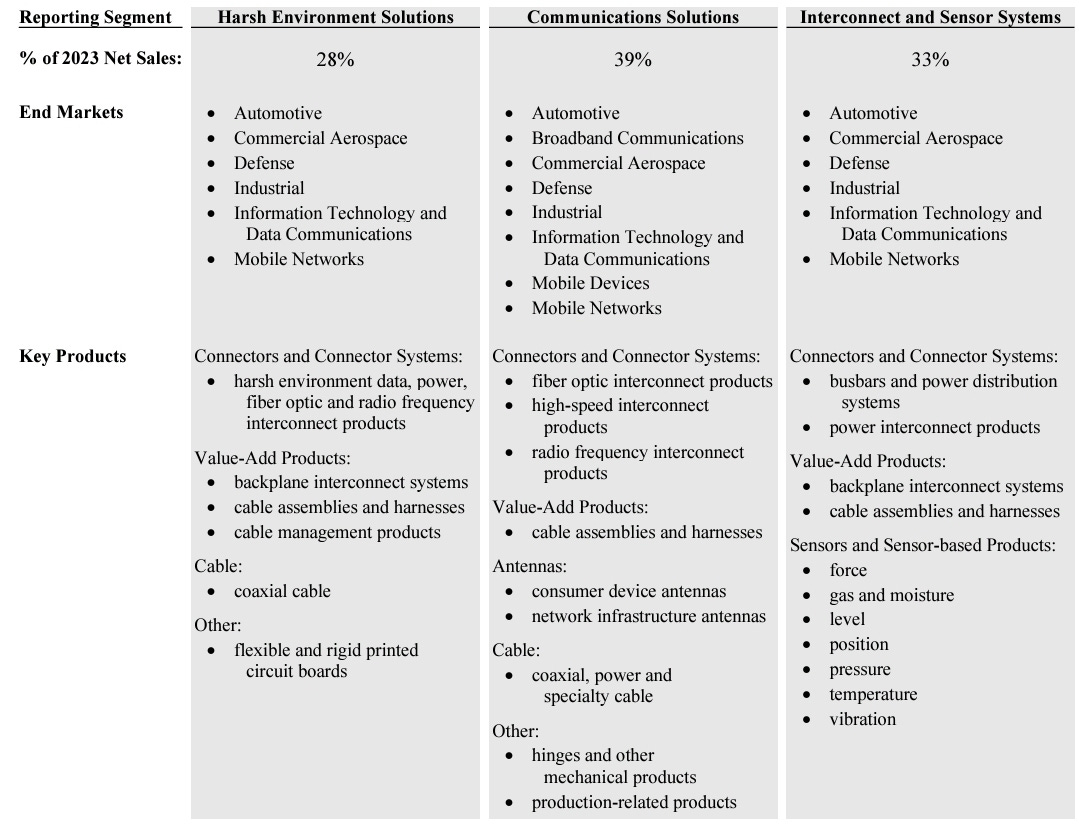

APH used to report the revenue stream into 2 segments: Interconnect and assemblies (95%), cable products and solutions (5%). However, as APH grew bigger, the categories were changed into 3 segments:

Harsh Environment

Communications

Interconnect & Sensors

With the new alignment, APH appointed three new segment managers:

William Doherty (joined 2005, Communications)

Peter Straub (joined 2013 from the GE acquisition, Sensors)

Luc Walter (joined 1984, Harsh Environments)

They report directly to CEO Adam Norwitt who joined APH in 1998 and worked his way up to CEO in 2008.

We like to see that the top executives have long tenures within the company.

Competitive Advantage #1: Operating Margins

One of the most common understandings is that APH products are mostly commoditized. It is also operating in a low barrier of entry industry. Therefore, they have to compete aggressively for price and quality in order to win market share, this translates to low margins.

APH has no scale advantages when it comes to purchasing materials as their materials are mostly commodities like aluminum, steel, copper, gold, etc. The cost of manufacturing depends on market prices.

However, let’s examine the operating margins of the 3 segments:

Harsh Environments segment have the highest operating margins at around 25% due to lower competition as the technology requirements are much higher.

Interconnect & sensor segment have around 18% due to the tough competition and APH trying to gain market share by lowering prices.

Communications have around 20%.

Typically, industrials have operating margins of 15% and below. If APH is getting above 15%, it means that either their products are not commoditized, or they provide a differentiated quality.

APH products have high durability that can withstand harsh environments, transmit data at high speed with low signal loss, and are highly customised. For example, it is not easy to be the supplier of automobiles OEM, as the repercussions of equipment failure is more serious than lower financial profits. These OEM go through thousands of hours of stress tests on chips, which connectors are highly important to ensure the success of the test. As a result, due to the long qualification time, APH products are more sticky.

APH makes specialized products that meet the specific needs of a particular application or industry. Adam Norwitt says this in 2022 Q4 earnings call:

We don’t view our products as a commodity. Actually, we view them as a very precious piece of jewelry. Interconnect, sensors, antennas; these are highly critical components that go into very complex systems, everything from mobile devices all the way up to fighter jets and everything in between. And they also represent a very high risk and relatively low value as a percentage of the total bill of materials.

Competitive Advantage #2: Capital Allocation

Let’s look at Sensata Technologies (ST) and TE Connectivity (TEL), they have gross margins similar to APH at 33%. But they lack behind by about 3% points in operating margins. We can attribute this to subpar capital allocation compared to APH.

TEL is in a perpetual state of reorganization. Over the last decade, they’ve gotten out of professional services, touch screens, broadband network connectivity, wireless, and subsea communications, indexing themselves to the more long-lived automotive and industrial markets, which now comprise 85% of revenue, compared to 48% for APH.

TEL recorded significant restructuring charges every single year since 2009. TEL trades at a lower earnings multiple than APH for good reason: In 2009, a year when organic growth declined by 16%, APH reported 18% EBITDA margins (worst in last 22 years). In constrast, 18% margins is about what TEL manages in its best years; gross margins are eroded away by less productive R&D and more operating expenses.

Over the last decade, APH has made more than 50 acquisitions. Cumulatively, APH has spent 23% of its capital on capex, 19% on R&D and 58% on acquisitions. Some of the bigger ones ($200m revenue) were once non-core segments of larger corporate entities (GE’s sensor business, Teradyne Connection Systems). Some are owned by private equity (Halo Technology, FCI). Or publicly traded (MTS Sensors). But for the most part, APH is buying $50-100m revenue businesses, often owned by families who are looking for a permanent home (APH has never divested a business).

In 2021, APH acquired MTS, a leading supplier of precision sensors, test systems and motion simulators for $1.7b (21x EBITDA). MTS sensor unit was complementary to APH’s portfolio of Harsh Environment sensors. MTS sensors include position sensors that are used for a wide range of industrial applications, test sensors used in the auto and aerospace & defense industries, and industrial sensors for the heavy industrial and energy verticals.

MTS was the first public company that APH acquired. It divested the test and simulation division to Illinois Tool Works for $750m. The sensor division was what APH wanted, which was actually the smaller but more profitable business unit. Net of the divestiture, APH paid $950m for the MTS sensor business (14x EBITDA). Assuming APH improved MTS operating margins to the corporate average of 21%, the effective EBITDA multiple paid would have been less than 10x.

Another large acquisition in 2016 costing $1.2b was FCI Asia. FCI was a leading interconnect solution provider for the communications and wireless networks verticals. It was reported that FCI had revenues of $600m and EBITDA of $120m, implying a purchase price of 10x EBITDA.

The latest largest acquisition is Carlisle Interconnect Technologies (CIT), costing $2b in cash. CIT is a leading global supplier of harsh environment interconnect solutions primarily commercial air, defense and industrial end markets. It is expected to have 2024 sales of $900m and EBITDA margin of 20% (11x EBITDA).

In its acquisition targets, APH looks for engaged and competent managers, which leads us to the decentralized structural advantage below.

Competitive Advantage #3: Decentralized Business Units

There is certainly some proprietary IP to ensure those connectors reliably transmit signals while preserving energy in even the harshest conditions, such as inside an HVAC system, an offshore oil rig, an engine cabin, the wheel of a plane, and other environments exposed to extreme heat and vibrations. But R&D makes up just 3% of revenue and we wouldn’t call this as a key advantage.

What really separates APH from its peers is how this diffuse set of products is manufactured and sold. That’s where there are commonalities with the Constellation Software playbook applying across vastly different verticals. We think it’s probably far less true of electrical components, where implementation details and margins can vary greatly by product, customer, and end market. But there are certainly relevant similarities between the two companies when it comes to organizational structure and the degree of operational autonomy granted to managers.

APH has 130+ business units, each led by a general manager who has autonomy over almost every aspect of the business including R&D, engineering, sales, marketing, quality control, manufacturing, sourcing, and back-office functions like HR, finance and IT. Each of these business units even operate their own ERP system, which could be viewed as inefficient. But it works for APH because these managers have incentives tied to accountability of their decisions. This autonomy also allows the managers to adjust quickly during sudden demand shifts in their end markets.

Cyclicality and Volatility in Organic Growth

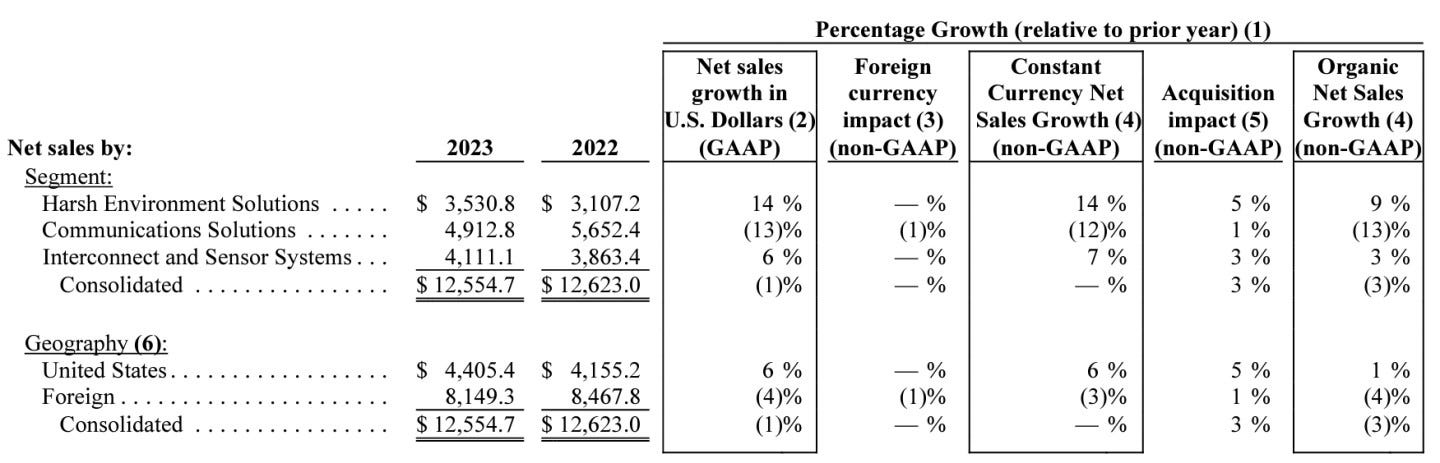

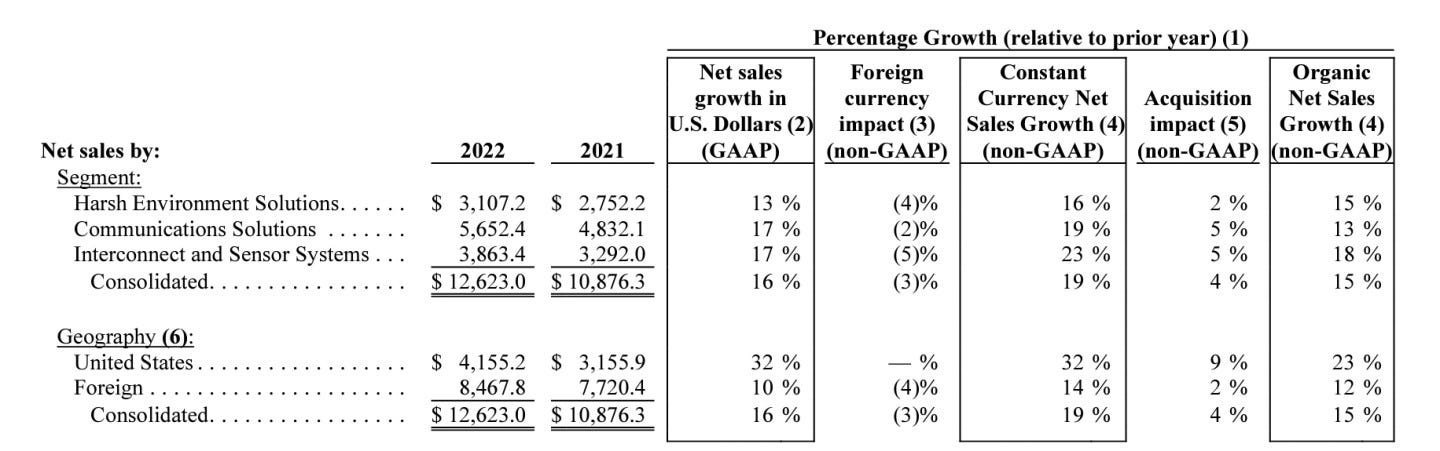

Organic growth rates follow the volatility of the industry cycles, it can range from above 20% to 0%. In 2023, organic growth was 3% versus 2022 of 15%:

APH is not immune to cycles but the swings are tempered by the wide diversity of end markets:

In 2015 – 2016, oil and gas markets fell while medical had strong demand.

In 2019, industrials fell while military and commercial aerospace recorded high growth.

In 2020 – 2022, automobiles declined due to COVID while industrials grew.

Beneath the cyclical swings, there is secular demand for more electronics that require greater speed and lower loss transmissions. This provides tailwinds for APH value propositions.

EBITDA margins are about the same since 2001, with very little variance in the intervening years. This is the result of constant acquisitions, which eventually converge to the company average but tend to dilute profitability for the first few years. Management claims that it doesn’t manage ROIC targets when evaluating acquisitions, which we find a little odd. They clearly abide by some valuation discipline, as acquisitions have consumed ~60% of free cash flow and returns on capital have remained steady through the years.

Management & Compensation

The management is rewarded based on metrics: 7% revenue growth and 11% EPS growth. Although it is not perfect, the target growth rate is fairly reasonable for a company their size. Note: The target rate has been revised downward from 8% sales growth and 14% EPS growth in 2018.

CEO pay structure is also highly performance based at 89% variable vs 11% fixed.

Management team collectively owned 2.1% stake in the company with the CEO owning $400m worth of shares. The CEO recently has made some sales on his holding for the past 2 years for around $180m cumulatively.

Valuation

We will have to do a detailed P&L with an attempt to factor in:

Cyclicality, we are possibly at the peak now;

Recent growth is due to price inflation more than volumes;

Margins to possibly decline in the future due to higher labour costs in Asia.

But at first glance, the market cap is $79b, with free cash flows of $2.2b, we can agree that it is probably too expensive to provide an adequate return.

Conclusion

Researching companies like APH made us appreciate the fact that investors don’t have to chase for the “next big thing” as these types of “boring” companies are producing market-beating results with great long term track records.

The price is too expensive to pay now, we hope that cyclicality can help depress the price.