AMZN: Amazon (4)

Preface: We have a small holding in AMZN and this post gives a short Q1 2026 update. Valuation not included.

Q1 2026 Update

AMZN delivered a great Q1 2026.

Net sales of $181.5b (+17% YOY).

Operating income of $23.9b, their highest ever margin at 13.1%.

AWS reported fastest YOY growth in 15 quarters of +28%, annualized run rate of $150b.

AI infrastructure buildout supported by $364b AWS backlog (excluding $100b Anthropic deal which is projected to contribute $18b this year).

$225b in Trainium revenue commitments.

AWS AI revenue growing triple digits YOY.

E-commerce & Advertising

North America

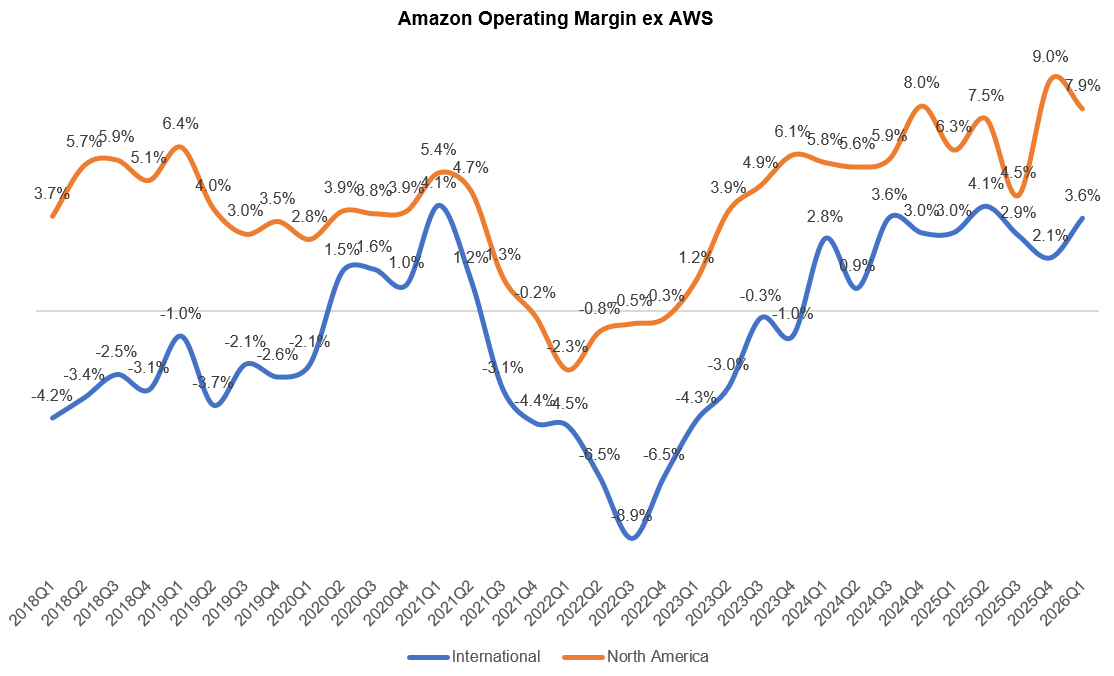

North America segment operating margin expanded YOY from 6.3% to 7.9%, the fruits of investing in logistic infrastructure and robotics automation are showing (FY2025 6.9%).

Think about this: +0.1% margins increase on revenue base of $426b is more than $4b of profits, and revenues have been growing double digits!

Unit growth went up +15%, the highest since COVID (total number of physical and digital products sold, net of returns and cancellations). Interestingly, average prices were actually falling:

In Q1, the average prices of products offered on Amazon.com decreased compared to the same period last year.

Q1 2026 earnings call

AMZN is now the second-largest grocer in the US by gross sales, with Whole Foods expanding to 650+ stores.

The combination of faster delivery, broader selection, and AI-powered personalisation (Rufus, Creative Agent) is widening their economic strengths in retail.

The ecosystem of AMZN benefits immensely from advertising. There are formidable competitors in this space, especially against Google. It is interesting to observe a noticeable drop in AMZN ads incremental share compared to Google.

Although AMZN ads grew faster for the last 4 quarters at +22% each quarter (FX neutral), but Google ads revenues accelerated every quarter:

+10% (Q2 2025)

+13% (Q3 2025)

+14% (Q4 2025)

+15.5% (Q1 2026)

Remember that even Google was losing share to META ads.

It is well-known consensus that AI is a massive tailwind for scaled digital ads players, but we think AMZN ads may be structurally positioned worse compared to Google and META.

AMZN mentioned Rufus which had MAU (monthly active users) growth of +115% and engagement growth of +400%, but we need to ask how Rufus is being used by customers?

Logically, anyone who goes to AMZN is very likely to already know what they want. AI recommendations wouldn’t have a significant impact compared to Google Search, which is further upstream where AI can genuinely improve comparative shopping queries.

The positive offset is that AMZN ads are intent driven, because shoppers who go to AMZN already want to buy something. The return on ad spend is strong. We think that AMZN ads segment should not be hurt by competitors.

With LTM ads revenues of over $70b, AMZN ads is now one of the largest digital advertising platforms in the world!

International

International segment went from an operating loss of -$0.5b to $1.4b profit in Q1 2026. Revenue growth of +11% (FX neutral) shows that the international expansion strategy is beginning to pay off.

Same-day delivery expansion across European hubs and the early-stage international rollout of Amazon Now (30-minute delivery in India growing at +25% month-over-month) are meaningful signals for further margin improvement ahead.

Put together, this is the e-commerce operating margins over time:

AWS

AWS is the segment everyone's most interested in.

Despite AMZN being the largest cloud provider in the world, growth still accelerated from +24% last quarter to +28% on a base that is now $150b annualised!

AWS reported $37.6b revenues that are very profitable with operating income of $14.2b (37.7% margins).

AI revenue within AWS is running at over $15b annually and growing triple digits. This is evidence that the ROIC of AI CAPEX might not be as lousy as most people suspected.

CAPEX was $43.2b in Q1, a huge number at $175b annualized. The front-loaded nature of AWS investment means that land, power, buildings, and hardware must be committed 6 to 24 months before billing customers.

Management expressed high confidence that AWS CAPEX will be monetised well, backed by customer commitments. They pointed to AWS 37.7% operating margin as validation.

AMZN is also selling Trainium racks. These are their proprietary chips for AI compute. Andy Jassy stated that Trainium2 is largely sold out. Trainium3 (30—40% more performant than T2) is nearly fully subscribed despite having just started shipping in early 2026. Trainium4 is still ~18 months from broad availability and is already substantially reserved.

The chips business has a $20b run rate (growing triple digits YOY), and Jassy estimated a standalone rate of $50b if all chips produced this year were sold externally.

Capital Intensity

For the past 10 years, the PPE asset turnover ratio have been decreasing. In other words, to produce $1 of revenue requires more capital than before.

This trend of higher capital intensity is not a new thing, but AI investments have significantly accelerated it.

We don't have to look too far back: In 2022, for AMZN every $1 of PPE produced $3 of sales (turnover ratio was 3). Then in 2025, the ratio was 2.4. This trend is consistent across the hyperscalers (Google, Microsoft, META), and not just AMZN.

If we look back further in 2016, the group collectively had PPE turnover ratio of 4.

Through this investment cycle, AMZN cumulative operating cash flow over this period is still higher than cumulative CAPEX by 10%. However, compared to the other hyperscalers, AMZN scores the lowest on this metric. This is due to AMZN having physical logistics that it needs to upkeep.

On incremental basis, operating cash flows increased by $93b, on incremental CAPEX of $60b.

We don’t know if this trend of PPE turnover will continue to fall. There might be a scenario where AI reaches an efficient/sufficient point that there is no need for incremental infrastructure spend.

Declining PPE turnover means that over-capacity and/or under-utilization is a risk — this worry is not new.

This risk explains why hyperscalers have lower valuations compared to the past. It’s not because investors think that ~20% topline growth is impossible at their scale, since the group has proven that their businesses can indeed grow fast. Rather, the reason is lower expected return on invested capital.

Conclusion

In summary, this was an outstanding report that showed the business is firing on all cylinders. So far, we have seen evidence of monetisation from their CAPEX spending.