AMZN: Amazon (2)

Intro

If we count AMZN’s roughly 500,000 subcontracted drivers alongside its 1.5 million employees, this gigantic organisation is likely the largest employer in the US, beating Walmart, which has held that designation for three decades.

In terms of revenues, AMZN is second only to Walmart. It is also a very strange company which has software, retail, logistics… basically it wants to be everything for everyone. Just a little more than a decade ago, AMZN had no outbound transportation capabilities, but today it has so many sortation centers and delivery stations that it delivers more packages than UPS.

What exactly is Amazon?

Why has it been so successful?

We try to get into the core of AMZN competitive advantages in this post.

AWS & Logistics Network

There are people who claim that AWS and their logistics operations can and should be separated because bulk of AMZN profits come from AWS, splitting it out will create a separate entity free from the burden of the low margin logistics business.

This argument misses just how integrated AWS is with the logistics operations. In the first place, AWS emerged from the competitive drive to enhance the efficiency of commodity circulation. AMZN then commodified and sold these capacities as standalone services, and the high returns and low marginal costs involved incentivized them to further expand these capacities.

But we can’t just cut AWS from the rest of the company without damaging its overall competitiveness. AWS still helps coordinate their highly advanced and flexible logistics network.

And of course, AMZN leverages AWS profits to support its extremely high levels of investment in its retail and logistics operations, which make up ~85% of net sales.

This integration is becoming even more important with time. AMZN is facing growing competition in the cloud sector from Microsoft and Google. As a result, it is expected that margins will start to come down.

AMZN’s strategy for dealing with this has been to leverage its advanced logistics to maintain its leadership in the cloud sector, enticing companies which are already using its cloud to also use its logistics as well.

If you like the cloud, why don’t you also let AMZN manage the back-end of your business?

Indeed, AMZN is currently positioning itself to offer supply-chain management and third-party logistics services. This means that AMZN strategy for maintaining its edge in the cloud business is completely bound up with its ability to sustain the competitiveness of its logistics.

Cash Conversion Cycle (CCC)

The CCC measures the difference between the time (in days) that it takes a company to sell inventory and receive payment and to pay its bills to suppliers. The lower the CCC, the longer a company holds on to cash after selling its inventory before paying its bills.

By a combination of these factors, a company can reduce CCC; collecting payments faster, selling inventory faster, or delaying payment to suppliers.

AMZN has a negative CCC. It has achieved this by maximizing the efficiency of its logistics system, selling inventory, and collecting payment extremely quickly. This rapid turnover has helped attract a large number of third-party (3P) sellers to sell on AMZN, which makes up a large and growing part of its business.

AMZN extremely efficient logistics and the reach of its e-commerce platform has allowed these sellers to benefit even though it delays payments it owes them for a considerable period of time.

So, the key to sustaining this negative working capital is to sell inventory quickly. If this competitive advantage can be maintained, AMZN will enjoy many billions of interest-free float, a very strong cash position, while displacing the debt and interest load on to smaller and weaker supplier firms.

In other words, suppliers are helping fund the growth of AMZN.

That’s the financial incentive for continuous reinvestments in productivity tools like robotics in their distribution networks.

Structural Differences in Suppliers

In a typical retail operation like Walmart, it has an advanced logistics system born out of necessity to survive high competition in the retail space. Walmart negotiates high-volume contracts with a smaller number of larger suppliers, receiving discounts via bulk purchases.

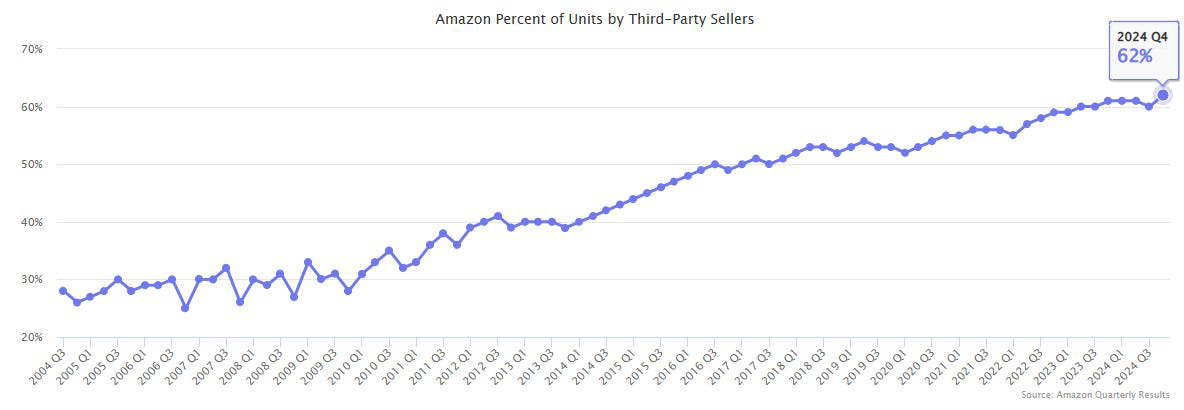

But AMZN is structurally different due to its heavy reliance on 3P sellers in terms of unit sales representing more than 80% of products and ~60% of units sold.

Note that 3P revenue numbers are lower than 1P (first party where AMZN sells directly to consumer) because 1P records on GMV (gross merchandise value) basis.

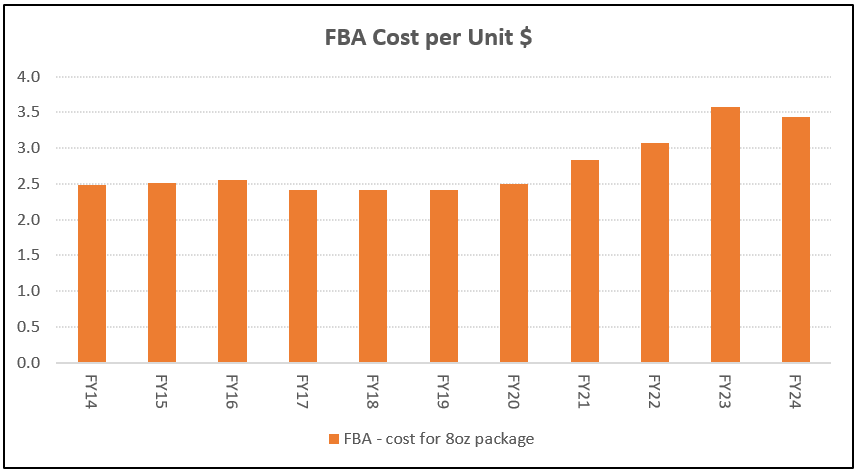

Rather than negotiating favorable wholesale prices, AMZN charges these sellers fees to use its system. It’s like a toll road, although with the very important caveat that AMZN also adds value to the platform that it operates.

This toll road increases FBA (Fulfillment By Amazon) fees at inflation rates:

This is turning its logistics operation into a commodity, making its system and platform available to anyone willing to pay the fees it charges for these services.

Instead of a scale-based model in which it gets discounts from large sellers for large volume, AMZN relies much more on the extraction of fees by its control and competitive operation of an e-commerce logistics system.

Because 3P sellers are fragmented, while AMZN is centralized, it also gains more leverage over these firms and is able to capture a large proportion of their total revenues in the form of seller fees, as well as, interest-free cash by delaying payment to them.

This underlines the importance of AMZN logistics; without its highly efficient distribution network, it’s not going to attract sellers.

From a seller perspective, their per unit fulfillment fee remains constant while having “infinite” shelf space, and they can scale without needing to build a logistics network.

This was what Nick Sleep calls “Economies of Scale Shared”:

If he [Jeff Bezos] shares the efficiency benefits that come with growth with his customers, he turns size, frequently an anchor on business performance, into an asset. In other words, the moat surrounding the firm deepens as the firm grows.

Subscription Services (Prime)

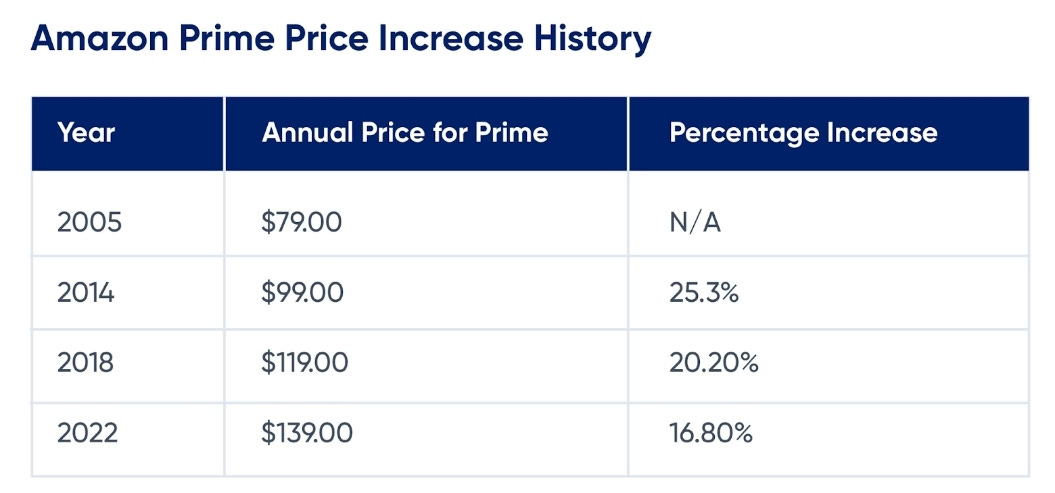

We think Amazon Prime doesn’t make good margins. Instead, the purpose is customer retention; offering substantial value relative to low subscription cost. AMZN has only raised subscription prices three times in the US since inception:

Revenues for subscriptions compounded at 18% since 2019. Prime is adopted by 85% of US households while international penetration is much lower. New subscribers will have to come from overseas.

Given the costs associated with Prime Video, Music, and same-day delivery, it is likely that this segment becomes profitable only at scale.

Advertising

Around 2012, AMZN started building their own ads tech. Only in 2021 did they separately report this segment. The growth was remarkable as it is now the 4th largest revenue contributor.

Monetisation primarily comes through Sponsored Ads, where customers can promote their products and brands across AMZN platform. The service has expanded to Display, Stores and TV & streaming, enabling customers to reach target audiences via a multi-channel approach.

Potential upside can come from AI-driven decisions that leverage on the deep database that AMZN has, turning into higher ROI ads targetting.

Competitive Dynamics

AMZN is competing with other players in various sectors across the economy over market share, but it is also locked in a struggle with its customers and suppliers to capture the maximum surplus for each other.

It wants to acquire the largest possible amount of surplus by forcing suppliers to accept the lowest possible prices while charging customers the highest possible prices. But its ability to raise prices is limited by the competitive nature of these markets.

AMZN has to attract supplier firms by offering them the opportunity to reduce their costs, lower turnover time, and reach the widest markets. Meanwhile, it has to attract customers by offering them fast delivery times and low prices.

Therefore, what is truly important is maximizing efficiency on both ends of their value proposition.

We argue that AMZN has pricing power due to its ability to expand both the willingness-to-sell (WTS) of their suppliers, and the willingness-to-pay (WTP) of customers. Gross margins can only provide a snap-shot of pricing power. True sustainable pricing power comes in the ability to raise WTP & WTS. The surplus is the gap between price-WTP and cost-WTS. Companies that can leave surplus for their customers and suppliers while expanding WTP & WTS have durable pricing power.

This circles back to the reason that AMZN prioritizes reinvestment.

Long Runway?

We think it’s very long. Because the unchanging fact is that customers always want lower prices and faster delivery, and if AMZN can achieve that, it attracts more suppliers to the network.

This means that there is always something AMZN can do to keep the flywheel spinning.

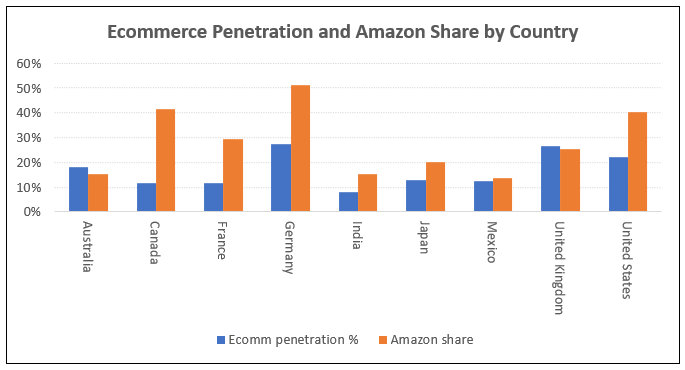

For example, the international expansion potential is still untapped. Germany is the only country that has higher penetration than the US:

The cloud opportunity remains significant. In 2023, Accenture estimated adoption was around 20% on cloud; 80% on premise. Now, we have more potential for AI, and these computations have to happen on cloud.

Some Challenges

3P Sellers conflict

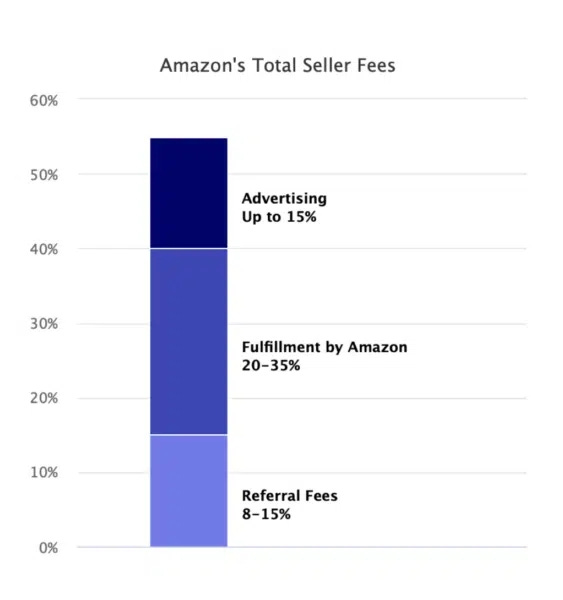

If you are a 3P seller, your relationship with AMZN is asymmetrical. AMZN has all of the leverage, which means you are at the mercy of fee increases across fulfillment, advertising, and commission rates.

The obvious way to combat some of these cost increases would be to increase prices, but AMZN gets a vote on that as well. If AMZN deems your price to be too high, they will suppress your listing from owning the “buy box” making it difficult to sell. In short, AMZN can raise your cost but prevent you from raising your prices.

China competition

In 2016, only 5-10% of AMZN sellers came from China. Today, this share has ballooned to more than 60%.

The most notable threat comes from the Chinese drop-ship players, primarily Temu owned by PinDuoDuo. Other companies include Alibaba, Shein and Tiktok. These players sell directly from manufacturers in China to consumers, removing the need for a middle-man distributor and bringing down prices.

Temu has the inherent advantage of having semi-managed logistics that can integrate into local seller systems. This reduces delivery times.

To fight this in the US, AMZN launched its own low-cost platform for items under $20 called Haul. AMZN has the advantage of an efficient localised returns process, a strong brand and a trustworthy screening process that protects shoppers from lower quality goods. But prices are slightly higher than Temu.

However, Temu is operating at a loss and will have to hike prices in the future, weakening the competitive threat.

Shopify

Shopify is a platform provider for independent merchants and brands who wish to sell directly to consumers. These merchants can set up individual branded online stores to either bypass or complement their Amazon storefront.

While Shopify offers more control and resolves the 3P seller conflict mentioned above, it doesn’t offer the consumer reach, marketing and logistics of AMZN.

We think both players are not direct competitors.

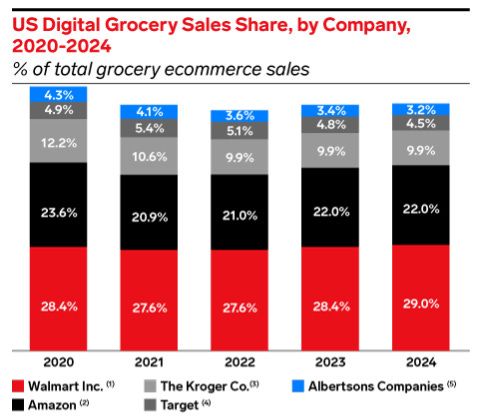

Digital Grocery

Walmart

AMZN has its own grocery subscription service at $10 per month, offering unlimited grocery delivery on orders above $35. The company operates Fresh and Whole Foods. The latter was acquired for $13.7b, since then AMZN has improved stores with checkout technology and lowered prices.

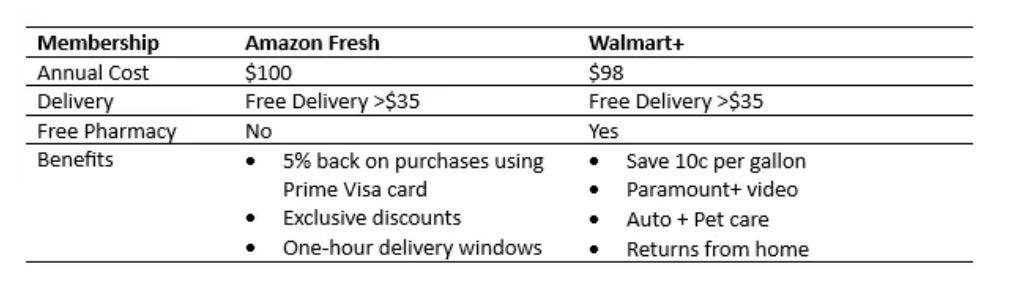

Walmart has a better value proposition in this area:

AMZN has yet to win in the grocery business, but it has really only been doing it since 2017. It will be a battle with Walmart while smaller competitors such as Kroger and Target lose share.

AI economics

Honestly, we don’t know how to measure this space, but we wouldn’t bet against the tech leaders who continue to signal progress and the transformational impact of AI.

Capable readers can go to Amazon blog here to read the tech behind cost savings.

Conclusion

In the past, we have owned AMZN at a cost basis of $2,000/share (pre 20/1 share split), but sold at $3,000/share (we make dumb mistakes all the time).

Now, we are quite satisfied with our understanding of AMZN business economics and will start purchasing at the current $2,380b market cap.