AMZN: Amazon (1)

Preface

In our quest to improve our understanding of the economics of tech companies, we inevitably studied Amazon, but we found that the economics of Amazon had little to do with tech itself although its success was leveraged on tech.

We wrote about Amazon in the past through the lens of Walmart here. This article further expands on the thinking and includes a valuation exercise.

Strategy #1: Leveraging Internet

Let’s start with a fun fact that if you enter the URL relentless.com in your web browser it redirects to Amazon.com.

Any attempt to understand the relentlessness of AMZN redirects to the founder Jeff Bezos. He created three massive businesses within AMZN, all of which generate huge consumer surplus and have super wide moats: Amazon.com, AWS, Amazon Platform (this platform is a catch-all for Marketplace and Fulfillment).

We start by analyzing his strategy of leveraging technology, specifically the Internet during its nascent age.

Most founder-led businesses emerge by solving a problem for themselves and then discovering a product that fits the market. Bezos, however, started with the solution and then looked for the problem. That solution was the Internet which he calls “the everything store”, the problem was how to start? And Bezos decided to start with selling books.

In 1994, web usage was growing exponentially. Bezos saw this and understood that humans have difficulty understanding exponential growth. So he made a list of 20 different products that he might be able to sell online. He settled for books for the primary reason that there were over 3 million different books in all languages during that time. The second choice was music, there were about 300,000 active music CDs. He saw that when there’s a catalog of products so huge, the only way was to host them online, no physical location will be able to carry them all and give easy access to consumers.

Being able to do something online that is impossible any other way is important. It’s the basic tenet of building any business, which is creating a value proposition for the customer. In the early years of the Internet, the value proposition AMZN had to built was incredibly large; modems were slow and websites often crashed. This meant that AMZN had to offer overwhelming compensation to get people to use online for this primitive tech.

Bezos understood that the value proposition of having access to millions of products around the world was worth the investment in the Internet. This type of business thinking shows that Bezos both grasped the opportunities and pitfalls of the early Internet, and took the decision to it’s logical conclusion.

Strategy #2: Leveraging Tech Economics

Although AMZN was considered as a “tech company”, we think that it’s purely because of the timing in the Internet boom. Every online business then was considered “tech”. The truth is AMZN is very much a retailer, the company recruited managers from Walmart and after the dot-com bubble burst, it was under pressure to raise prices for profitability.

There were two turning points at this stage.

First, Bezos had a meeting with Costco founder Jim Sinegal in 2001 who explained the Costco model to Bezos:

The membership fee is a one-time pain, but it’s reinforced every time customers walk in and see 47-inch televisions that are $200 less than any place else. It reinforces the value of the concept that customers will find really cheap stuff at Costco.

Low prices generated high sales volumes, and Costco then used its significant size to demand the best possible deals from suppliers.

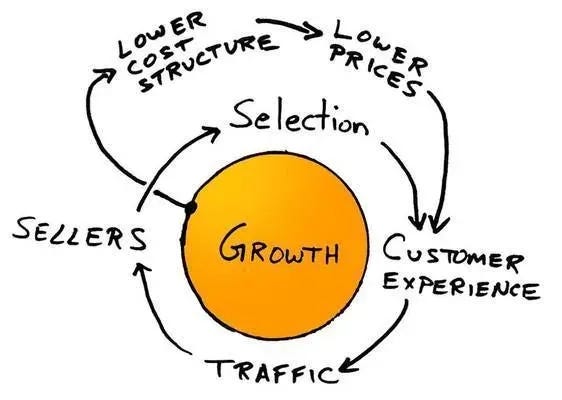

Bezos immediately went back and cut prices, but Sinegal’s core insight only really crystallized later when Bezos and his team created the AMZN flywheel model.

Lower prices led to more customer visits.

More visits increased volume of sales and attracted more commission-paying third-party sellers.

Per unit cost decreases, increasing efficiencies.

Greater efficiencies allowed for further lower prices.

Feed any part of this loop and it will accelerate the effects. This resulted in the famous Bezos napkin diagram:

Tech economics are different from most other businesses because of the near zero marginal costs. In the book The Intel Trinity, Bob Noyce at Fairchild Semiconductor had this critical understanding:

In the spring of 1965, Noyce got up before a major industry conference and in one fell swoop destroyed the entire pricing structure of the electronics industry. Noyce may have had trouble deciding between conflicting claims of his own subordinates, but when it came to technology and competitors, he was one of the most ferocious risk takers in high-tech history. And this was one of his first great moves. The audience at the conference audibly gasped when Noyce announced that Fairchild would henceforth price all of its major integrated circuit products at one dollar. This was not only a fraction of the standard industry price for these chips, but it was also less than it cost Fairchild to make them.

The reason this was possible is that the true cost of integrated circuits came from the R&D costs to design them, and capital costs to manufacture them; the actual materials cost was practically zero. This meant that the best route to profitability was to make it up in volume. This equation is even more powerful in software, which has only R&D costs, and zero material costs. This overall concept, that tech is governed by a world of zero marginal costs, is what makes tech economics fundamentally different from most businesses.

However, still AMZN actually had to pay for the products it sold. To bet everything on volume in an attempt to gain leverage on fixed costs was risky when there was marginal costs that AMZN could not escape from.

What Bezos did was to priortize boldness, to maximize future cashflows rather than maximize current reported earnings. In his inaugural 1997 shareholder letter:

We will make bold rather than timid investment decisions where we see a sufficient probability of gaining market leadership advantages. Some of these investments will pay off, others will not, and we will have learned another valuable lesson in either case.

This approach led to the success of AWS. During the initial launch of AWS Bezos wanted it to be a utility with discount rates, even if that meant losing money in the short term. Willem van Biljon, leader of the team that created AMZN Elastic Compute Cloud (EC2), proposed pricing at $0.15/hour, a rate that he believed would breakeven. Bezos unilaterally revised that to $0.10/hour.

A decade later AMZN would finally separately report AWS results in 2015, revealing both sales of $7.9b and operating income of $1.9b, an impressive 24% margins! Fast forward to 2023, AWS reported sales of $90.7b and operating income of $24.6b (27% margins)!

It is no surprise that Andy Jassy, the head of AWS, is not an engineer but holds a MBA instead. He succeeded Bezos as CEO, reflecting the company’s business-centric roots, rather than what the market categorizes AMZN as a tech company.

Strategy #3: Leveraging Platforms

There’s a popular believe that AWS was created out of the desire to utilize spare capacity. We don’t think that’s the case, because it took years for Amazon.com to fully run on AWS. It was created to solve an internal problem: how to create new customer experiences without constantly waiting for the infrastructure team to set up dedicated capacity?

The solution was to offer basic compute offerings. For example, EC2 is a web service that offers scalable computing capacity in the cloud allowing users to manage virtual servers and run apps without need for physical hardware.

After solving this problem for themselves, AMZN could extend this out to outside developers.

The AWS layer has high fixed costs but benefits alot from economies of scale.

The cost to build AWS was justified because AMZN’s own e-commerce business was the best use case.

Selling web services to outsiders increased the returns to scale and widened AWS moat stemming from switching costs.

The above describes a play on the power of platforms.

Another similar approach comes with Amazon Prime platform, it offers superior experience, prices and selections. It also plays on the concept of scale.

Fulfillment centers have high fixed costs but benefit alot from economies of scale.

The cost was justified because AMZN’s own e-commerce business was the best use case.

Most third-party sellers have their products stored at AMZN’s fulfillment centers and covered by Prime. This increases return to scale, increases value of Prime, widens AMZN’s moat.

Over the years AMZN’s investment in fulfillment has ballooned into a multitude of new distribution and sorting centers, a transport hub for a growing fleet of airplanes, trucks, and a massive delivery operation that largely bypasses UPS and Fedex. To put in perspective, in 2023, third-party sellers contributed $140b out of total sales of $575b.

Culture Matters More

While the Internet was unquestionably a critical component of AMZN’s success, the true competitive advantage AMZN possess is not a technology advantage. Real moats are built with real dollars, and AMZN’s management has been relentless in pushing the company to continually invest in solving problems with real world costs. Compound this culture with the application of tech economics and we arrive at what sets AMZN apart as a wonderful business.

Valuation

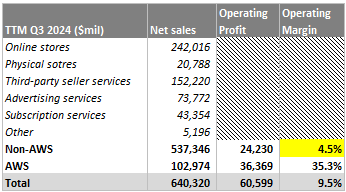

First off, AMZN does not provide the operating margins of non-AWS segments. Since AMZN reports AWS separately we can use it to imply the non-AWS segments, the result is weird that it only gives 4.5% margins as a group (TTM as of Sep 2024):

This is nothing new, AMZN has always been known to have thin margins for non-AWS. However, we will need to restate the reported accounting earnings to arrive at the true economic earnings to correctly judge AMZN.

Let’s rationalize by segment…

Online Stores

This is AMZN’s largest and oldest segment. We think that this segment’s margins should be at least equal to Walmart’s of 4%.

Walmart depreciation expense, a proxy for how much it must spend to maintain its physical stores, is about 2% of annual sales. AMZN’s online stores logically don’t require such high maintenance CAPEX.

Walmart also suffers from shrinkage theft of average 1.5% of annual sales. AMZN does not have this disadvantage.

So the true economic margins for online stores is probably 7.5% = 4% + 2% + 1.5%

Physical Stores

The majority of physical stores refers to Whole Foods which AMZN acquired in 2017. Before that, Whole Foods was running at ~5% margins. We continue to assume 5% margins.

Subscription Services

AMZN views subscription business as ways to bind customers to its platform. The revenues from Prime subscription is offset by cost for streaming video services and free shipping costs.

This segment can be thought of as the “loss leader strategy” retailers use in order to attract customers into the store.

We suspect this segment is breakeven at 0% margins.

Third-party (3P) Seller Services

In 2000, third-party seller revenues represented only 3% of sales, today it’s 24%. When 3P merchants sells products on its website, the 3P pays for the goods, meaning that AMZN avoids the COGS. This platform model have almost no marginal cost for onboarding a new seller.

We can think of this as a toll bridge type of business. So what type of margins should such a segment earn? The positives are no COGS and fees charged are pure margin, but the negatives are cost associated to packing, storage and shipping.

If we reference to eBay (pure 3P reseller) it enjoys ~20% margins. There are offsetting effects, although eBay doesn’t incur shipping fees, its biggest expense is marketing. AMZN probably does not need to spend on marketing given the strength of it’s brand.

On balance, we assume that AMZN’s 3P segment earns 20% margins too.

Advertising Services

Advertising happens in the online world, apart from payroll for engineers to configure ads, we don’t think there are other significant costs. We can reference with Google which has 40% operating margins on ad-related segments (search, YouTube).

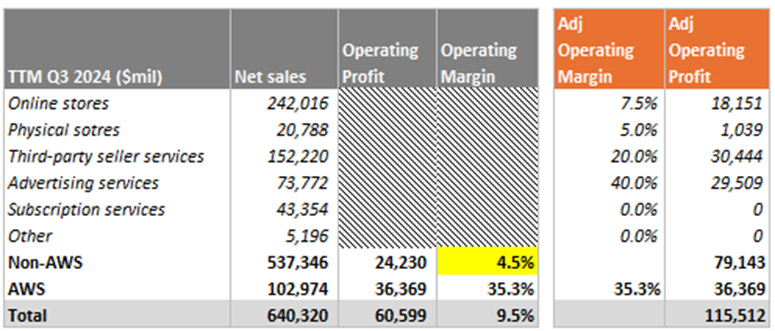

Below is the restated operating profits that more likely represents AMZN economic earning power:

After applying an effective tax rate of 17%, the adjusted PAT is $96b. An after-tax improvement of $46b.

The market cap today is $2,290b which translates to an adjusted PE ratio of 24x, while the GAAP PE ratio is 46x.

Another Way to Adjust

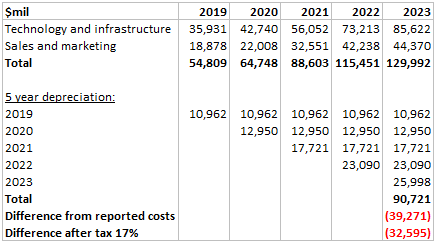

GAAP rules for marketing and R&D spending states that these costs should be immediately expensed off in 1 year. However, do we think that the benefits for such costs only last for 1 year? Clearly not. R&D today is more maintenance than research in nature, the latter might be speculative and should rightly be expensed off. Similarly, marketing expenses have multi-year benefits, the brand awareness gained does not disappear the next year.

Using this approach, we can depreciate these costs over some period of time. We don’t profess to know what is the correct “useful life”, but let’s assume it’s 5 years:

The result is a lower expense of $39.3b, if we apply the same 17% tax, then $32.6b of benefits flow to the bottom line.

The adjusted PAT would be ~$83b, implying PE 27x.

In running through this exercise, if you feel uncomfortable with the adjustments, then we have achieved our goal. The lack of exactitude drives most analysts crazy, but treating GAAP earnings as representative of businesses like AMZN which thrive within tech economics is not right.

Now, if you believe that AMZN trades at 24x to 27x true PE, it is still not very cheap. Because we have to remember that AMZN will likely continue to reinvest into the future, and as shareholders the returns we get are still the present value of future distributable cashflows.

The basis of restating earnings is to simulate the situation when AMZN becomes a steady-state business and stops reinvesting most of their FCF. Time frames become an important variable in this equation, the longer we have to wait for cashflows, the stronger the reason we have to demand a cheap valuation.