ADBE: Adobe

History

Adobe was started by John Warnock and Charles Geschke, the company was named after a creek in Los Altos near Charles’ house. The founders met each other while working for Xerox, John was leading a team at Xerox to build InterPress, a protocol for Xerox printers and became disillusioned as Xerox showed little interest in going to market with his product.

They developed PostScript, a programming language between PC and printer that could describe text, graphics, and images on one page. PostScript, along with the Apple Macintosh graphical user interface and laser printers, launched the desktop publishing industry in the 1980s. ADBE found the product market fit right away and kept growing revenues at more than triple digit rates in the first six years since its founding. Apple, under Steve Jobs, bought ~15% stake in ADBE in November 1984 for $2.5m. ADBE went public in 1986, and when Apple decided to sell its stake in 1989 (Steve Jobs wasn’t there anymore), the investment was worth ~$84m, returning 3,400% or 102% CAGR over 5 years! Since Apple sold, ADBE continued to compound at 30% for almost 4 decades. So why did Apple sell?

In 1989, although ADBE had 30 customers, Apple accounted for 29% of ADBE revenue and decided to work on a rival product of PostScript. Given the former partners were becoming potential rivals, Apple sold its ADBE stake. While ADBE sales decelerated dramatically in 1989, it also laid out the groundwork to diversify its products. By 1990, ADBE launched two more products that defined their categories: Illustrator (vector-based editing software) and Photoshop (pixel-based editing software). Illustrator was developed organically, while Photoshop software was licensed from the Knoll brothers in 1988 and eventually acquired for $34.5m in 1995. In 1991, Adobe Premiere (video editing software) was launched. Then, in 1993, ADBE launched Portable Document Format (PDF).

The history of PDF is quite interesting. While PDF is by far the most pervasive digital document format today, during the early 1990s nobody understood how important sending documents electronically was going to be. In fact, ADBE board wanted to kill the project, but John had a vision that industries needed a universal way to communicate documents across a wide variety of machine configurations, operating systems and networks.

It wasn’t the private sector which internalized the value of PDF, but the Internal Revenue Service (IRS) which really made good use of PDF in digitizing its tax forms. In early 1990s, IRS used to send mails to hundreds of millions of individuals during tax filing season. Given the complexity of tax code, these forms came with wide variety of clauses. By 1994, IRS started distributing tax forms in PDF format which accelerated the adoption curve.

The speed of product launches during those early years were impressive: Photoshop, Illustrator, PDF, these are still household names even decades later. Considering the natural obsolescence risk the tech industry generally faces, it is a remarkable feat.

From 1996 to 2002, ADBE slowed down and revenue grew at less than 7% CAGR. Warnock retired from CEO in 2000 and then from CTO in 2001. Both founders co-chaired the board until 2017. After Warnock, Bruce Chizen became CEO who came to ADBE from the acquisition of Aldus in 1994. During his tenure, Chizen made a significant acquisition of Macromedia primarily to get Flash for $3.5b in 2005. Then in 2007, Shantanu Narayen became CEO who is still leading the company today.

While ADBE somewhat got out of the slump it found itself during the rise of internet, sales continued to be lumpy and much more volatile. During the 2008 GFC, sales fell by 18% in 2009, ADBE experienced higher volatility than most software businesses at that time because recurring revenues were only 19% in 2011, and the rest of the revenues were mostly generated by selling perpetual licenses, meaning that customers pay once and can use the software indefinitely. Narayen wanted to make the business more predictable and stable even in difficult periods. As a result, ADBE announced the switch to subscription model in 2011 and for a couple of years, they supported both perpetual licenses and subscription model. By May 2013, they fully went into the subscription business.

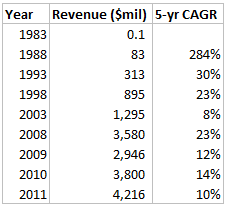

Below table shows the snapshots of revenues since IPO in 1986, showing the high initial growth, volatility post tech-bubble and the recovery post-GFC:

The decision to go subscription model has been a great success. But it was far from an obvious decision at that time. Apart from reducing revenue volatility, there were other important reasons behind ADBE’s change to subscription model. Under the perpetual licensing model, the number of units shipped was about 3 million for a long time, and the only way they could increase sales was by raising prices or customers upgrading products. For example, the perpetual license for Illustrator used to cost $399 in 2004, $499 in 2005, and $599 in 2008. Even though ADBE clearly had pricing power, the management perhaps suspected such a strategy had an expiry date, especially in the zero marginal cost of software world. Moreover, ADBE suspected there was a much bigger market out there which it was not serving, for people who were unwilling to pay a high upfront cost.

After being stuck at 3 million units under the perpetual licensing model, ADBE out-performed its guidance of 4 million subscribers for 2015, ending the fiscal year with more than 6 million subscribers. As of 2023, ADBE reported 33 million subscribers in its Digital Media segment which is mainly Creative Cloud (contains Illustrator, PDF, Lightroom, Photoshop, Premier Pro etc.).

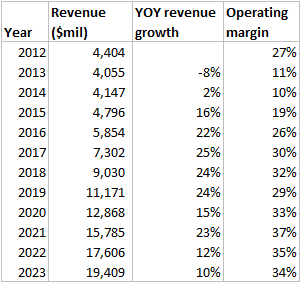

More importantly, the subscription model increased operating margins significantly. Even though margins took an immediate hit following the switch, it quickly recovered to 26% in 2016, and in 2023 it was 34%.

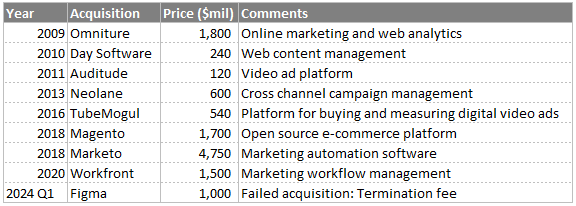

What made this transition perhaps even more impressive is not only ADBE continued its dominance in Creative Cloud but also expanded its business to a new segment Experience Cloud via the acquisition of Omniture (digital analytics tool for online platforms) in 2009 for $1.8b. Then in 2012, Adobe launched Adobe Marketing Cloud which was later renamed to be “Adobe Experience Cloud”.

Business Economics

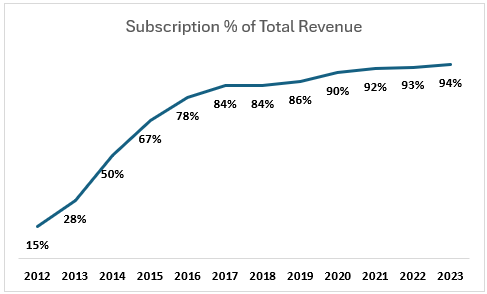

Almost all of ADBE current revenue comes from subscriptions:

Adobe breaks down its revenue into 3 segments: Digital Media (73%), Digital Experience (25%), and Publishing & Advertising (2%).

Digital Media

Adobe reports Digital Media in two categories: Creative Cloud (CC), and Document Cloud (DC). ADBE disclosed the user base of 6 million in 2015 and does not provide this statistic anymore, only mentioning in press releases that Digital Media has 33 million subscribers today.

Creative Cloud

CC is cloud-based subscription solution related to photography, design and video. The whole CC package cost $59.99/month for individuals. Since individual apps such as Photoshop cost $22.99/month each, anyone who needs at least 3 apps is better off buying the whole package.

For context, the CC package used to cost $2,599/year under the licensing model back in 2012 compared to $659.88/year under the subscription model. A typical customer under the licensing model used to buy a new license approximately every 4 years to access all the new features and updates, ADBE needs to keep a subscriber for 4 years to make the two models breakeven. The fact is that most creative professionals who stop using Adobe are those who end up leaving the profession. Therefore, the retention ratio, especially for enterprise customers, is likely to be extremely high.

Moreover, because of the low upfront costs, ADBE products can reach a much wider population. With the rise of social media and digital content, ADBE products reached an audience much bigger than it perhaps could imagine in 2010.

In 2023, CC contributed 81% of Digital Media revenue and 48% of total revenue.

Document Cloud

DC segment consists of Acrobat branded products which allow users to create, edit, export, combine, share, and collaborate on PDF documents. If a customer buys the whole CC subscription, it already includes Acrobat Pro subscription, it is also possible to buy only Acrobat subscription for $19.99/month. Adobe Sign, which allows users to send and sign any document from any device, and Adobe Scan are also included in the Document Cloud segment. Unlike CC, everything is bundled together in Acrobat subscription.

In 2023, DC contributed 19% of Digital Media revenue and 14% of total revenue.

Digital Experience

With its Omniture acquisition back in 2009, ADBE showed intent in building Digital Experience business, which was formerly known as “Digital Marketing” segment. Shantanu Narayen explained the thinking behind building this business:

We said (at the time of the first Experience Cloud acquisition), instead of just focusing on enabling people at the front end of the creation process, why don’t we really look at what role we can play in the management, monetization, and mobilization of all of this content.

Digital Experience focuses on four key categories: content and commerce; data insights and audiences; customer journeys and marketing workflow which are all delivered on a common platform called Adobe Experience Platform.

Since 2009, we estimate ADBE spent at least $12b in various acquisitions to build its offerings on Digital Experience; the actual amount spent is likely to be higher since many of the purchases were undisclosed. We can estimate that since 2009, Adobe spent $13.6b in acquisitions which was ~38% of cumulative FCF. The only major acquisition related to CC segment was Frame.io in 2021 for $1.3b, so ADBE spent ~$12b to build the Digital Experience business.

For context, Digital Experience generated $4.9b revenue in 2023 which contributed 25% of total. However, we will argue later that the Digital Experience segment is likely close to breakeven from operating margin perspective.

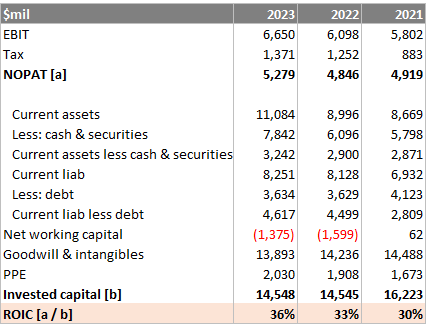

Constructing Operating Margins by Segment

ADBE has an effective “monopoly” in Digital Media segment, especially the CC segment and it deploys the cashflow to build another business in Digital Experience segment, in order to gain exposure to broader profit pool of the content/creativity value chain.

Management perhaps wants to diversify the business, but the core business is doing so well that they’re not being able to diversify much despite spending a lot of money on acquiring companies related to Digital Experience.

On margins, segment information is not disclosed but we can try to rationally construct the cost structure. We will use Salesforce as a competitor comparison to Digital Experience as they are of the same nature. Salesforce is of course on a much larger scale and could provide hints on what margins might look like if Digital Experience reaches scale.

To construct Digital Media margins:

R&D was 18% of total revenues, we think that most of Digital Media R&D is maintenance rather than invention. We assume 15% goes to R&D.

Marketing was 28% of total revenues. Apps in Digital Media most likely require little marketing as everyone knows Photoshop and PDF, selling to enterprises probably needs more effort and discounts given throughout the year also contribute to marketing expenses. We assume 27% goes to marketing.

Sanity check: 46% implied marketing cost to Digital Experience, which can be compared to Salesforce also averaging 46% in marketing spend.

If we believe our educated guess is directionally correct, then Digital Experience is probably operating at breakeven while Digital Media drives all the profits.

Notes on Competition

With such juicy software margins, competitors are bound to attack every business segment. We attempt to provide some insight into the major competitors.

Figma

It is interesting that while ADBE raised price for Illustrator by ~50% from 2004 to 2008, CC prices have gone up by only ~10% (individual subscription) over the last 10 years. We think that following the switch to subscription plan, ADBE was positively surprised how a large part of the market remained untapped for a long time, and with the rise of digital content, ADBE might want to grow the user base instead of price maximization.

ADBE still has a price lever to pull if they ever feel they are reaching near the full penetration level. Short-term inflation may give software companies such ADBE a good excuse to raise prices permanently. The power of zero marginal cost in software can only be fully enjoyed if ADBE can protect it’s product, it will be more difficult to extract supernormal profit from its CC software given the rise of compelling alternatives.

We will focus on the recent failed acquisition of Figma to demonstrate how smaller firms can challenge ADBE.

When customer needs rapidly change, there is less advantage in being an incumbent. Instead, legacy companies are left with all the overhead and a product that no longer is what customers want. There are many causes of changing customer needs. Often there are new and growing segments of customers with different use cases. Existing products may work for them, but they are not ideal. The features they care about and how they value them are very different from the customers the legacy company are used to. Incumbents resist changing core parts of their product for every new use case since it’s costly. But every once in a while, what was once a small use case grows into one large enough to disrupt the incumbent.

The core insight of Figma is that design is larger than just designers. Design is all of the conversations between designers and project managers (PM) about what to build, the prototypes, feedbacks and implementations.

Figma is browser-first, which was made possible and perfomant by their understanding and usage of new technologies like WebGL, Operational Transforms and CRDTs. For a user’s perspective, there are no syncing that needs to be done with others editing a design. Features like team libraries gave designers incentives to pull their colleagues into Figma. While Figma is building the ideal tool for designers, they also built something more important: a way for non-designers to be involved in the process.

Historically it has been very difficult for non-designers to be involved during the design process. If PMs or engineers wanted to be involved, there were many logistical frictions. If they wanted the full designs, the designer would need to send them the current file. They then need to download it, and also make sure they had the right Adobe product installed on their computer (costly tools for those who didn’t design regularly). And these tools were large, slow, specialized programs that were difficult for those not familiar with using them. It is hard to navigate a project without a designer to walkthrough it.

Designers who wanted feedback need to guide their PMs through the process; exporting the designs into images, sending screenshots, and later figure out how to translate the feedback into changes in the actual design. The turn-around-time was so long that designers needed to pause their process while waiting for feedback.

Figma fixed these problems by putting the process entirely cloud-based with real time collaboration.

The best tool for individuals may also be the best for the entire team. But it’s the latter that matters. And beyond some level of enhancing individual productivity, it’s the team aspects that are increasingly important.

For example, in word processing, there used to be lots of experimentation and customization around individual features like typesetting. But once this was good enough, the focus has shifted towards collaboration. And for most use cases, few care about typesetting today. Increasingly, our tools must understand and align with how we collaborate. This was less important when collaboration was logistically difficult and prohibitively costly, but as collaboration becomes easier, its importance has risen. This is essentially Figma’s value proposition.

To put some numbers into perspective: Figma was launched in 2016, it was estimated to more than double annual recurring revenues from $75m in 2020. While the growth % seems impressive, ADBE’s absolute dollar growth in 2021 was 12x the size of Figma’s estimated topline. In June 2021, Figma raised $200m at $10b valuation, likely valued at ~67x price-to-sales. For context, it took ADBE about 8 years to exceed $150m revenue in the 1980s while Figma took 5 years.

Given that regulators blocked the $20b Figma acqusition, the challenge to ADBE remains as Figma continues to improve its products and ecosystem. It seems difficult to predict now, but it’s something that needs to be closely watched, especially given that CC likely generates almost all of ADBE cashflows.

Generative Artifical Intelligence

Text-to-image generative AI tools such as Dall-E creates realistic images from a description in natural language. The big tech are building their own AI tools and they have deep pockets to experiment. It remains to be seen how such innovation would affect ADBE.

To keep up with technology, Photoshop now has AI tools to help manipulate images. The productivity boost is quite substantial, for example, functions like “Generative Expand/Fill” and “Variation” instantly solves repetitive tasks. Language based prompts can quickly layer on background images without the need for traditional masking and layering techniques.

DocuSign

In the enterprise market, ADBE and DocuSign operate in largely a duopoly. However, DocuSign is a much larger player than ADBE. Based on revenues, DocuSign is the clear leader in the purely e-Signature market.

We think that e-signature itself is a commodity business and it can be hard to justify the premium DocuSign charges unless they provide more than e-signature solutions.

As expected, DocuSign is trying to build a platform business via “Agreement Cloud” which includes e-signature, contract lifecycle management, and electronic notarization.

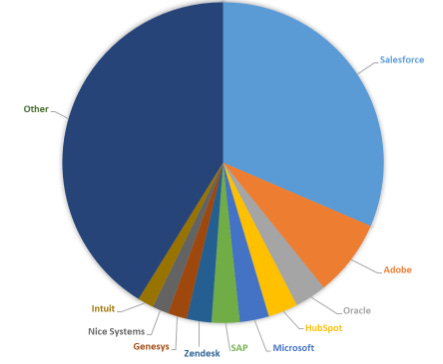

Salesforce

Salesforce competes within the Digital Experience segment. This is the top 10 CRM vendors by market share:

Salesforce is obviously at a much larger size and enjoys better economies of scale, as mentioned above ADBE spent significant amounts of capital building Digital Experience from acquisitions, unfortunately we don’t think it is a profitable segment.

Capital Allocation

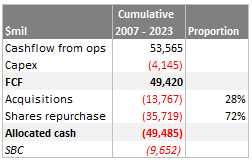

We take a look at the cumulative use of FCF from 2007 to 2023 since the current CEO Shantanu Narayen took over:

ADBE is a capital light business which is expected of a good software business.

Shares repurchases made up a huge portion at 72%.

Acquisitions is also significant at 28%. We have doubts that these acquisitions mainly done for Digital Experience actually yield decent returns.

There are 2 recent examples in the last 5 years that suggest ADBE overpaid.

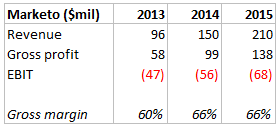

Marketo

Since Marketo went public in 2013, we have their financial statements until 2015 after which Vista acquired it for $1.8b in 2016. Marketo’s revenues more than doubled but it was making EBIT losses every year:

Just 2 years after Vista’s acquisition, ADBE bought Marketo for $4.75b in 2018, higher than what Vista paid for by $3b. ADBE mentioned Marketo posted $320m revenue in 2017 which implied 23.5% 2-year CAGR from the reported revenue in 2015. Presumably, while the revenue growth had slowed, operating margin supposedly improved (ADBE confirmed this but didn’t explicitly disclose the numbers).

If we assume Marketo’s revenue to grow at 20% CAGR from 2017 to 2027, it will have $2b of revenue.

Assuming cost numbers: gross margin 70%, R&D 15%, Marketing 35%, SG&A 10%… we get EBIT of $200m (or 10% margin).

For ADBE to get ~10% IRR on the $4.75b price paid, Marketo has to sell for 60x EBIT multiple. That’s obviously overpaying.

Figma

Adobe’s acquisition of Figma was reported as a $20b consideration, 50% cash and 50% stock, plus 6 million ADBE restricted stock units (RSUs) in retention packages for Figma employees.

However, the number of RSUs was fixed based on the date of the deal announcement on 15 Sep 2022, not the closing date. This means the actual consideration received by Figma shareholders would vary based on fluctuations in ADBE stock price.

At the time of the announcement, ADBE traded at $370/share. The total consideration for Figma was then $10b in cash, $10b in stock and 6 million retention RSUs worth $2.2b, for a total of $22.2b.

Regulators eventually blocked the deal. As part of the termination, ADBE paid Figma $1b breakup fee in cash. This fee was set as part of the initial acquisition agreement, and in some ways, it highlighted Figma’s bargaining position at the time and the perception of potential risk to the acquisition.

Figma has attracted $333m in funding, so the $1b breakup fee received just 3 days after termination is triple their total raised capital. Figma with 1,400 employees could probably sustain 3 years of OPEX with the $1b fee alone.

At the time of acquisition, Figma’s revenues were $400m, meaning that ADBE was willing to pay 50x price-to-sales. This is an expensive price to pay to acquire a strong competitor. Furthermore, in the next 18 months, Generative AI took off and put more pressure on ADBE competitive position.

Incentives Structure

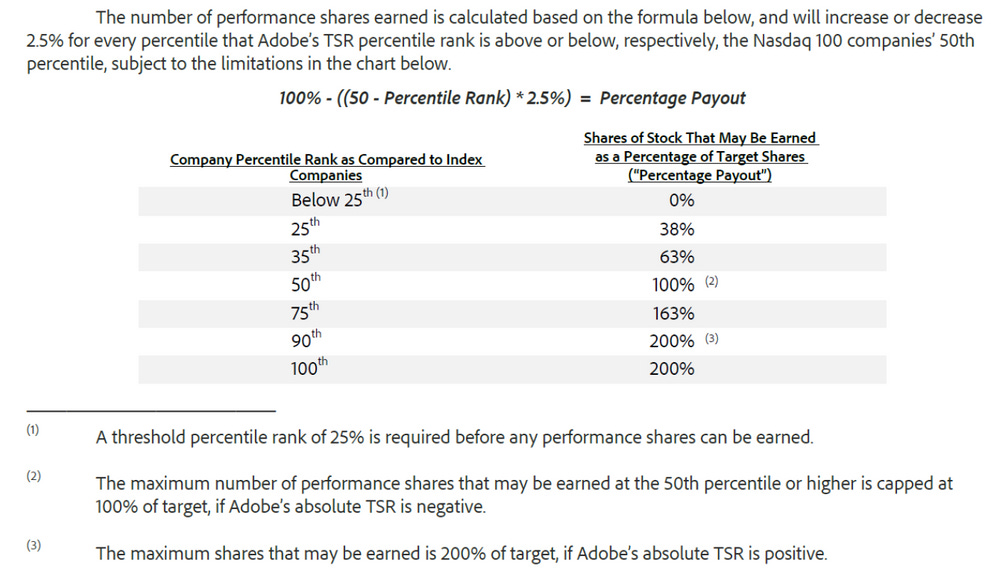

For long-term incentives, ADBE follows a relative Total Shareholder Return (TSR) approach, benchmarking against NASDAQ100. If TSR is negative, the maximum payout is 100% even if relative TSR percentile is above 50.

Disclaimer before Valuation!

For readers who have made it this far, you should have got the sense that it is not easy to predict with confidence the growth rates of tech-software businesses. Competitors can spring up and sell at expensive prices. Disruptive technologies can also emerge and threaten the business in a profound way.

So we are not going to pretend that we can do a bottom-up approach and arrive at anything less than a fuzzy valuation. Instead we will invert the problem and find the implied growth rates if we were to buy ADBE today at $225b market cap.

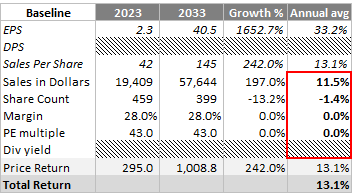

ROIC, PE, Implied Growth Rate

With average ROIC = 33%, PE = 43x, we test for required rate of return:

IRR = 10%, implied perpetual growth rate = 8.5%

IRR = 12.5%, implied perpetual growth rate = 11%

For context, FCF (less SBC) had 10% 5-year CAGR.

Factors of Returns

We use past 5 years revenue CAGR and share count reduction, assume no contraction in margins or PE multiple. If the PE drops to 25x, total return drops to 7.4%.

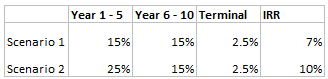

Reverse DCF

To solve for today’s market cap of $225b, these are the variations of FCF growth rates and their returns:

Conclusion

We usually shy away from tech investments due to our inability to confidently know what the business will be like in the long-term. Although we can factually learn about the economics and somewhat understand ADBE competitive strengths and weaknesses, the predictability and durability of its moat still allude us.

We put out the valuations as a rough guide for interested readers to measure for themselves.