9983.T: Fast Retailing

History

Fast Retailing (FR) was founded by Tadashi Yanai who is currently the richest man in Japan, although FR was officially created in 1991, its roots date back to 1963. Tadashi was born in Ube, Yamaguchi in 1949. When he was born, his father Hitoshi Yanai was already in the business of selling clothing under a shop named Ogori Shoji. The store location was located in the same building as where the family lived.

He attended Ube High School and later Waseda University, graduating in 1971 with a degree in Economics and Political Science. After graduation he got a job in the same clothing industry but he was not working for his father yet, instead Tadashi worked at a supermarket selling men’s clothing and kitchenware. He was in charge of replenishing inventories and his manager would reprimand him often because he came to work wearing shirt and jeans, while others wore formal outfits. Tadashi questioned the manager about the choice of outfit since it was not going to help him in stocking up inventories, following this Tadashi quit his job after only a year. This starts to give us a glimpse of his ideas of functionality over style which would manifest in the products of Uniqlo that we are familiar today.

After resigning from the supermarket, at age 23, Tadashi went to work for his father selling suits and ties. He initially thought that it would be a dreadful job, but eventually came to realize that running the business was interesting. By 1984, his father had 22 stores in several locations.

In the same year, Tadashi now 35 years old travelled to Europe and America to discover the impact of brands like GAP and Benetton. They were making casual, non trendy clothes where simplicity was their competitive edge. He was able to see the immense potential if this style was introduced in Japan, so he started making plans on evolving his family’s business to go from suits to casual wear.

That is when the first Uniqlo store opened in Hiroshima, 1984. It was initially named “Unique Clothing Warehouse” which later was renamed to “Uniqlo”. His focus was on non trendy casual wear that were inexpensive but made of high quality fabrics.

The brand grew quickly. Its success led to opening the first large roadside outlet in Yamaguchi to cater to the bulk buying segment and customers arriving by car. In 1991, the company renamed the parent company to “Fast Retailing”. It was subsequently listed in both the Hiroshima and Tokyo Stock Exchange.

During this period, the Japanese Banking Crisis happened, leading to stagnating household consumption. FR took advantage of the economic downturn by continuing to sell good quality products at low prices. In November 1998, the first store in Harajuku district, Tokyo, was opened. It featured a budget fleece jacket product which cost only JPY1,900 (at that time fleece was considered luxury).

The mission statement was clear that Uniqlo is a modern Japanese company that inspires people to dress casual, there is no visible brand mark and designs are simple and comfortable. This is in contrast to their biggest rivals Zara and H&M which differentiate themselves through sophistication and trends.

After dominating the Japanese casual clothing domestic market, Uniqlo experienced saturation. Thus, it pursued aggressive international expansion to continue its growth and compete with global brands. In 2002, FR launched two large retail stores in Shanghai. The response was phenomenal as the sales skyrocketed and the number of stores grew exponentially, as of 2023 there are 930 stores in mainland China, surpassing 811 Japanese stores.

However, FR expansion into European and US markets was not as desirable. In UK, only 17 stores exist today compare this to H&M which entered the UK market in 1967 and now has 238 stores. For the US and Canadian markets, they announced a goal of 200 stores but today only 72 stores exist.

In 2019, Uniqlo entered into New Delhi, India. Today they have only 13 stores. Compared to South East Asia 287, Taiwan 73, Hong Kong 33, South Korea 131.

It seems like the brand does not travel well outside of Asia.

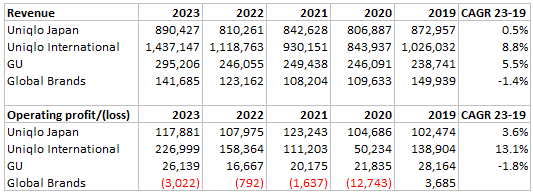

Today, FR operates 2,469 Uniqlo, 468 GU and 654 Global Brands stores (Theory, PLST, Comptoir Des Cotonniers, TAM.TAM). In 2023, FR made US$18.9b revenues of which contributed by Uniqlo 84%, GU 11%, Global Brands 5%. For context, revenues of main rivals are H&M US$21.7b and Zara US$36.9b.

Product Innovation

Although the clothing designs are simple, they pride themselves in fabric innovation. In 2006, FR partnered with Toray Industries to further push innovations on materials for example:

Ultra-light down product line jackets with 90% down and 10% feather ratio and just weighed 206 grams.

Heat Tech featuring lightweight yet warm innerwear.

Ultra Stretch jeans designed to feel soft yet having the look of regular jeans.

Quick dry wear using polyester fibers made from recycled PET bottles.

The focus on functionality over design gives FR space to produce clothes that ignore the ever-changing trends, marketing itself to the larger segment of customers who want clothes that will never look old fashioned.

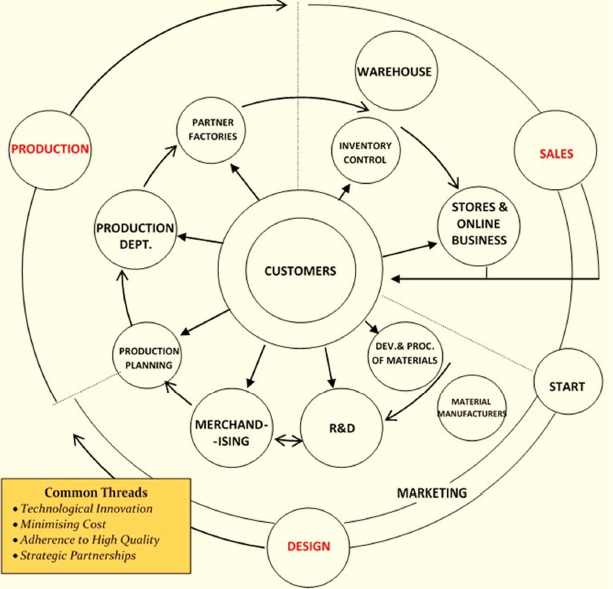

Product Development Cycle

Competitors (Zara, H&M) who chase trends need to change inventories rapidly, whereas FR does not need to respond and plans its product lines up to a year in advance. This ensures that their product development team is aware of how the customer actually responds. The product team also handles customers’ concerns and gives information on how their products can be improved. Below is the business model taken from their website:

Employee training & customer service

The average training period for each new employee is up to 3 months. Below are some of the unique characteristics:

All Uniqlo stores have a poster in the manager’s office which reads: “Always follow company direction. Do not work your own way.”

Every Uniqlo shop assistant must memorise six phrases and be ready to recite them to all customers as they meet them in the store:

(1) “Hello, how are you today?” or “Welcome to Uniqlo.”

(2) “Did you find everything you are looking for?”

(3) “Let me know if you need anything.”

(4) “Thank you for waiting.”

(5) “Did you find everything you are looking for?”

(6) “Good bye. We hope to see you again soon.”

The repetition at 2 and 5 is not a mistake; every customer is supposed to hear it twice.

Uniqlo’s offshoot brand, G2, allows people to wear the clothes out of their Tokyo store before coming back to buy them.

Employees must be able to fold 6 shirts under one minute.

Return customer’s credit card with both hands and full eye contact.

FR understands that every single touch point with a customer is an opportunity to reinforce the brand.

Low SKU

Ignoring fashion is probably the most important distinction between FR and its competitors. There is a cost advantage because if FR doesn’t care about fashion, it follows that they carry much lower SKUs.

This explains the low inventory turnover ratio, over the past 10 years inventory turnover days increased from 104 (2014) to 128 (2023). This means FR sells and replaces its stock of clothes about 3 times per year, which makes sense because they mostly change stocks on 2 seasons: summer and winter.

This should give FR better negotiating power with suppliers and lower chances of supply shortages.

Competition

Retail is brutally competitive. There are a lot of incentives to undercut prices and this causes the industry as a whole to suffer from low margins. We present the two main competitors below.

Zara (under Inditex Group)

Amancio Ortega, the founder of Inditex (parent company of Zara), built the retail giant by establishing Confecciones Goa in 1963 as a dress-making workshop for housecoats and robes in north-western Spain. By the early 1980s, Zara had a stronghold in the Spanish retail business and had expanded to several major Spanish cities. It continued its expansion as Zara went international with its first store in Portugal in 1988, and the following year went into the US market. Further expansion into foreign markets continued with Mexico (1992), Greece, Belgium, and Sweden (1993).

By the end 2001, Zara was listed public and its shares were over-subscribed by 15.9 times. Two decades later, store count has nearly doubled with a presence in 96 markets globally. This success can be attributed to Zara’s unique business model of quick response. It starts with the design process via Inditex, which in-houses 700 designers who churn out 50,000 fashion creativities per year. The designs are in constant sync with customer feedback, and the sketches go from drawing board to stores in just 6 weeks (source: Inditex annual report, 2022).

This is achievable due to its robust supply chain, location of its logistic center and production houses. Unlike its competitors, who have outsourced production to low cost Asian countries and have a long wait time, Zara’s competitive advantage lies in its quick response time.

H&M

Erling Persson, the founder of H&M, started with a women’s clothing store named Hennes in Sweden (1947). It gradually expanded its footprint to Stockholm and pursued its first international expansion to Norway in 1964.

In 1968, with the acquisition & merger of Mauritz Widforss, the brand was renamed Hennes & Mauritz or commonly referred to as H&M. Steffan Persson, the founder’s son took over the operations and replaced traditional newspaper advertising with large city billboards. H&M engages supermodels and famous actors within the fashion industry to boost its branding.

In the 2000s, H&M expanded to the US and the emerging economies of Asia. It also began collaborating with famous designers like Versace, Karl Lagerfeld, Sabyasachi, placing affordable design products in stores.

In 2021, H&M operated the highest single-brand stores globally, far more than Zara and Uniqlo.

Weakness #1: Unit Economics

To calculate the unit economics of running a new store (currency in JPY):

Sales per store = $770m

Return per store = op margin * sales = 13.8% * $770m = $106m

Capex per new store = $28,600m / 16 = $1,788m (2023 AR, note 13: PPE)

ROI = 106/1788 = 6%

We estimate new stores give about 6% return on investment, which is not a good ROI. This is due to the unprofitable Global Brands segment which recorded closures of about 290 stores (-30%) since 2019. If we exclude Global Brands segment in our calculation, we get a small improvement to 7% ROI:

Sales per store = $905m

Return per store = 14% * $905m = $128m

Capex per new store = $1,788m (assume no capex was spent on Global Brands)

ROI = 128/1788 = 7%

Weakness #2: Expansion into Western World

The Uniqlo brand and culture does not travel well outside of Asia. The main reason is due to Japanese, Chinese and Korean culture as a group is very homogenous, but the western world is much more diverse. The Global Brands segment reported operating losses year after year:

Uniqlo International segment is doing well mainly due to China, South Korea and South East Asian markets.

Weakness #3: Casual Functional Wear is Not Defensible

It is not impossible for existing or new competitors in retail to copy what Uniqlo is doing. Examples of similar alternatives are: COS (H&M), MUJI (Japan), GAP (US), Pull & Bear (Inditex Group) etc.

Valuation

A quick glance would tell us that FR is overpriced. The business produces 15% return on equity over the last decade, and market cap grew in line at 13%.

Excess cash is returned to shareholders via dividends, excluding COVID year, the average payout ratio is 33% of net income. Shares outstanding have remained constant since 2002.

Management has significant net worth tied to the shares of FR. Tadashi Yanai holds 18.4% of the company, and both his sons Kazumi and Koji holds 4.7% each. Total family control is 27.8%. The other major shareholder is the Bank of Japan at 31.8%.

FR provides guidance for 2024 financials of ¥3t sales and 14.9% op margin (source: here). We use approximately the same figures. Operating margins have been high in recent years attributable to price inflation rather than volumes, as we can see customer numbers are flat, but average purchase size increased:

We assume that operating margins will gradually decrease over time to the long run average of 11%.

Converting the P&L projection into cashflows, we assume a discount rate 12.5% and terminal growth 2.5%. The intrinsic value is about ¥7.8t, current market cap is ¥12.4t.