9537.T: Hokuriku Gas

Introduction

During our study of Hikari Tsushin, we came across an utilities company that Hikari Tsushin owns 6.3% of shares.

This company is Hokuriku Gas, it is traded on Tokyo Stock Exchange and is very cheap for an utility business.

Hokuriku Gas was founded in 1913 and supplies city gas to homes and businesses across Niigata Prefecture. It operates as a local gas utility and has been part of the region’s infrastructure for more than a century.

The business model is simple: it delivers gas to residents/industries who use it everyday for heating and cooking.

While sales can fluctuate based on weather, gas is a basic necessity and hence exhibits predictable demand.

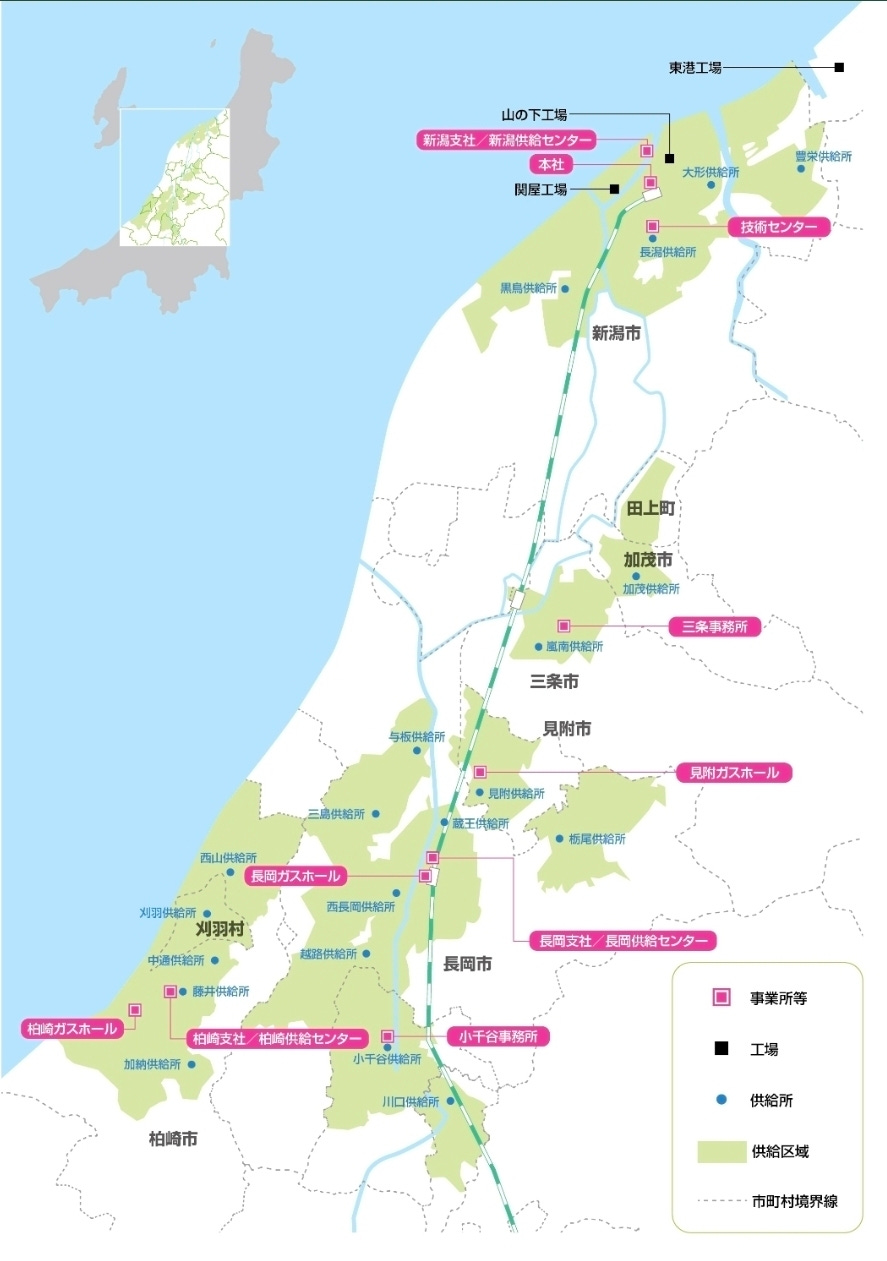

Hokuriku Gas owns and controls 6,098km of gas pipelines in the areas it serves. These pipelines run under city streets and connect directly to homes, offices, and factories. Building a competing gas network would require digging up roads, spending huge amounts of money, and getting approval from local governments. Because of the cost, complexity, and disruption involved, it makes little sense for a new competitor to try.

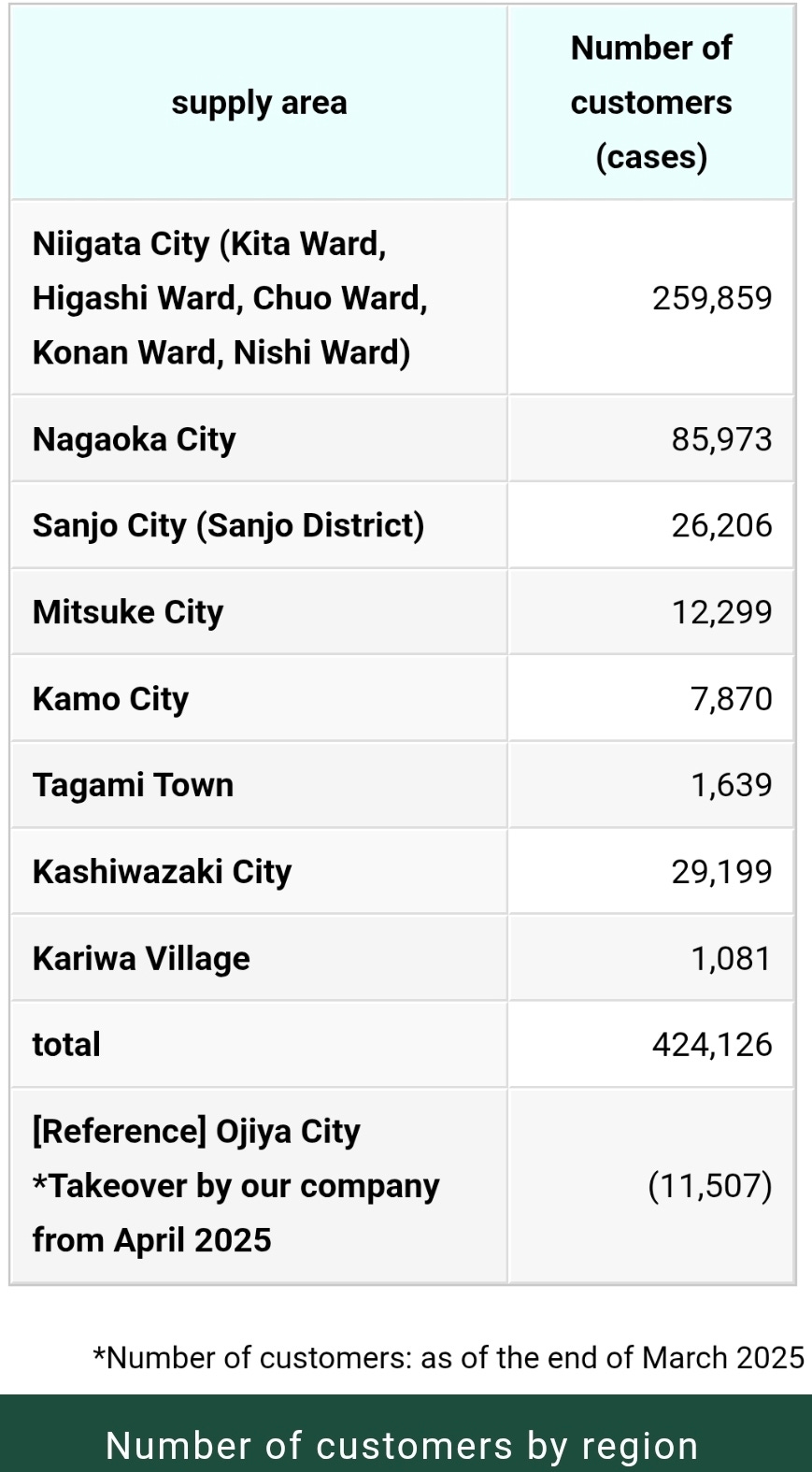

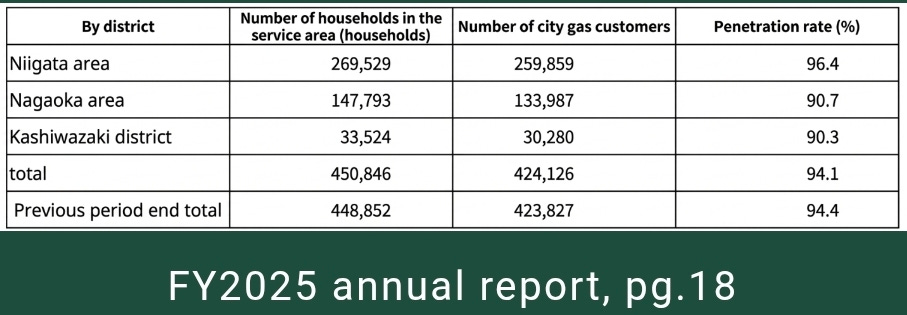

As a result, Hokuriku Gas operates as a monopoly in the cities and towns it serves. These include Niigata, Nagaoka, Sanjo, Kashiwazaki, Mitsuke, Ojiya, Kamo, as well as Tagami Town and Kariwa Village:

Together, these areas are home to over 430,000 customers. Hokuriku Gas is the only realistic provider of city gas in these locations not because of a legal monopoly, but because the economics make competition impractical.

This position is strengthened by high switching costs. Homes and buildings are already designed to use gas, and appliances are built specifically for it. Switching to another energy source cost time, money, and inconvenience, so most customers stay with the existing provider.

Over the years, Hokuriku Gas has grown by taking over former municipal gas operations and integrating them into its existing network. This adds new customers without changing the nature of the business.

Most of the expensive infrastructure was built long ago 1960s to 1990s, which means today Hokuriku Gas mainly focuses on maintenance (pipelines barely expanded less than 1% for the past 5 years). As a result, it generates steady cash flows from an essential service that people need everyday.

Natural Monopoly

What would it cost to replace or compete with Hokuriku Gas?

It delivers city gas through 6,098km of pipelines to over 430,000 customers in Niigata Prefecture. To compete in a meaningful way, a new entrant would need to build a parallel pipeline network under cities that are already developed, which is very expensive and disruptive.

Even a starter network could still require 300–500km of new pipes. With regard to pipeline network constructions, the Japanese government has not yet made official plans for a nationwide pipeline network, nor has it provided financial aid for its construction.

Therefore, upstream and downstream companies need to fund construction of their own pipelines. On a per-unit basis, gas transported by pipeline may be generally cheaper than transporting and re-gasifying LNG but the former option tends to require considerably more capital expenditure to build the pipeline.

For instance, when facing with large uncertainties including the weather conditions or a volatile industrial demand that is affected by the economic conditions, new entrants are discouraged from investing in a pipeline even if large demand is expected. In these cases, the utility must purchase LNG via tank trucks. Thus, although the natural gas industry has been regulated for a long time, the government has never had a strong concern for pipeline construction.

There are a 3 options for gas procurement stipulated by authorities:

1. If wholesalers (upstream companies) in the vicinity are already transforming petroleum and coal gas into natural gas, and utilities can purchase natural gas from the wholesalers, then these utilities should purchase natural gas from local wholesalers via a pipeline connection.

2. If utilities cannot purchase natural gas from wholesalers via pipelines, then they should construct their own regasification facilities, and purchase LNG delivered by tank trucks from wholesalers.

3. If utilities can neither purchase natural gas via pipelines nor construct regasification facilities, then they should provide substitute natural gas (SNG, a blend of gas from other hydrocarbon sources) to their end users.

The current state is that almost all distribution utilities procured natural gas by #1 or #2 methods.

Japan imports nearly all of its natural gas from overseas, the country has been the world’s largest LNG importer since 1969 only to be surpassed by China in 2023.

In 2017, LNG imports was 91.3% of all natural gas, 5.4% was produced domestically, and the remainder was generated from imported petroleum-based gas. Niigata Prefecture produces 74% of Japan’s domestic natural gas due to the Minami-Nagaoka Gas Field being one of Japan’s largest onshore gas fields in terms of reserves (located 10km southwest of Nagaoka City in Niigata Prefecture).

Hokuriku Gas benefits from this as a purchaser (through wholly owned subsidiary Hokuriku Natural Gas) and distributor of LNG. It’s not the best position in the supply chain in terms of capital intensity, but still it has a monopolistic position in Niigata region.

Ownership Structure

Hokuriku Gas is led by Kazutomo Atsui (敦井 一友), the current President and Representative Director. He’s been a Director since 2006, moved up to Vice President in 2012, and became President in April 2017. He owns 840k shares worth ¥3.1b (1.75% voting rights).

The Chairman is Eiichi Atsui (Kazutomo’s father), who previously served as President. He owns 556k shares worth ¥2b.

Related to the Atsui family, the single biggest holder is Atsui Sangyo (11.3%), and then a cluster of Atsui-linked foundations:

Hokuriku Gas Scholarship (9.6%)

Atsui Scholarship (7.1%)

Atsui Collection (3.2%)

Atsui Co Ltd (2.2%)

Together, the Atsui-related shareholding is ~33% of the company. Outside of that bloc, notable holders include Hikari Tsushin (6.3%) and UH Partners 2 (5.2%). Local stakeholders like Niigata Hume Pipe (5.6%) and regional financial institutions include Sanjo Shinkin Bank (2.5%) and Daishi Hokuetsu Bank (1.85%).

Risks

Natural Disasters

Japan is a hotbed for earthquakes so we cannot escape this risk of damaged pipelines and the costs associated to repair/replace.

As an example, in the 1964 Niigata earthquake, the pipes of a gasoline tank owned by Showa Shell Sekiyu, located between the airport and the harbor were damaged. Fire spread to nearby tanks and induced explosions that continued the fire for 12 days.

More recently, in 2024, Noto Peninsula earthquake resulted in disaster losses of ¥203m for Hokuriku Gas.

Shift to Electric Homes

There are pressures to move away from LNG to electric homes.

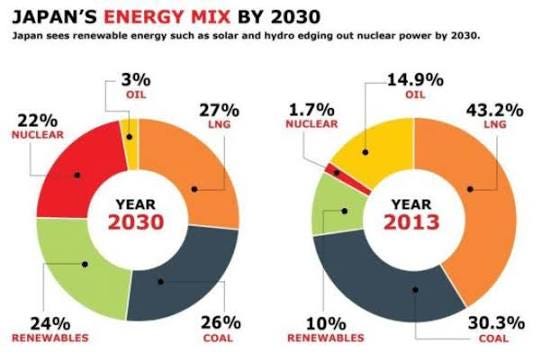

In 2013, LNG accounted for 43% of Japan’s power generation, with 30% coming from coal and 15% from oil. Nuclear accounted for just 1.7%, with the remainder coming from renewable sources.

By 2030, Japan plans to have 27% LNG and much more nuclear and renewables.

In response to the shift, Hokuriku Gas sells their own system to generate electricity using gas, it claims to reduce utility bills substantially and offers 10 years of free maintenance.

Volumes have actually declined for the past 5 years, but price increases have kept sales up from ¥48.3b to ¥61.8b. In October 2024, they revised gas rates for the first time in 14 years.

Capital Allocation

This is a capital intensive business with CAPEX consuming 66% of cash flow from operations (CFO). Cumulatively for the past 6 years, CFO was ¥42.5b and CAPEX ¥28.1b.

Shares repurchases only spent ¥471m (1% CFO) even though the stock has been cheap. Dividends paid was ¥2.4b (6% CFO), but every year it’s constant at around ¥400m.

We don’t like management’s attitude towards keeping cash when they should distribute it out.

Activism as a catalyst is also difficult because of the sticky ownership structure and illiquid trading volume, it would be difficult to get substantial voting power without affecting the share price.

Valuation

Current market cap is ¥17.2b with a small amount of long term debt at ¥108m and equity of ¥52.2b. Cash is ¥8.7b, making up half of the market cap.

Intangibles assets are ¥2.4b, so the price to tangible book value is just 0.35x.

10-year average FCF yield is 18%. FY2025 (ending March) FCF was ¥3.4b, that’s a LTM yield of nearly 20%.

In short, we have a business that has defensible competitive advantages, trading cheaply, but is family controlled. Cash is returned to shareholders mostly via dividends. The current dividend yield is 2.1%.

Conclusion

It’s obvious that Hokuriku Gas shares are cheap relative to cash flows and asset base. It controls the local market, sells an essential service, and trades at 20% FCF yield. Even better, it has negligible debt and real assets already in place.

We wouldn’t need growth for the investment to work, it just has to operate as usual. This is a very attractive proposition, but the capital allocation part is lacking.