9435.T: Hikari Tsushin

Stock & Business Performance

Hikari Tsushin (HIK) (9435.T) is a Japanese conglomerate trading on the Tokyo Stock Exchange. It has a fascinating history and management adopts the most capitalist mindset which is uncommon for a Japanese firm.

Over the last 15 years (fiscal year ends March), its share price went from ¥1,518 to ¥38,550 (CAGR 24%), plus paying out a total of ¥4,854 dividends per share. The dividends itself would have covered 3.2x the initial purchase price in 2010!

For the past 15 years, the business highlights were:

Operating profits CAGR 24%

Interest and dividend income CAGR 30%

Profit after tax CAGR 39%

Shareholder equity CAGR 15%

Through shares repurchases, the per share statistics are even more impressive:

Earnings per share CAGR 42%

Dividend per share CAGR 17%

What is the most amazing is that the employee count actually shrunk by 3% CAGR in the past 15 years (from 8,768 to 4,861 employees) and the operating profit per employee increased by 29% CAGR!

History

The Telecom Boom

Founded in 1988 by Yasumitsu Shigeta, Hikari Tsushin (光通信) translates to “Optical Communication Network”. Just like how “Berkshire Hathaway” refers to the original textile mill which has no resemblance to today; Hikari Tsushin started out by capitalizing on the growing demand for mobile phone and office solutions in the 1990s. But it also evolved into a conglomerate that doesn’t resemble its origins.

Shigeta came from an elite family where his father was a lawyer. However, he took the unconventional route: after dropping out of Nihon University, 23 year old Shigeta founded HIK by selling home telephones door-to-door. Then, the company expanded to selling copiers (mainly made by Sharp) and business telephones. Shigeta used data from the telephone directory “Town Pages” published by NTT (Nippon Telegraph and Telephone) consisting of 5.3 million companies and created a list for sales targets, focusing on small and medium-sized businesses.

In 1993, prices of mobile phones started to fall. In response, NTT and DDI (Daini Denden, Japanese telecom company that later merged with KDD and IDO to form KDDI) switched from a rental model to a one-time purchase model for mobile phones.

HIK reduced its traditional door-to-door sales and opened mobile phone sales stores, launching the “HIT SHOP”. The first HIT SHOP opened in Shinjuku, Tokyo in May 1994.

The business model revolved around a “stock commission” paid by mobile phone companies (¥300/month per phone, with a contract period of 5 to 10 years). The more mobile phone users there were, the greater the stock commission.

In addition, when a new contract was acquired, the company received approximately ¥43,000 from the mobile phone carrier as an “acceptance commission”, which was recorded as revenues.

To expand the number of HIT SHOP stores, HIK decided to adopt franchising instead of direct ownership. By end of 1998, the number of HIT SHOP stores reached 1,816; a rapid expansion considering only 4 stores were launched in 1994.

In the near future, most people will be using communication devices such as mobile phones and pagers. The key to success will be whether we can build a sales network before other companies do.

If we don’t think about mobile phones all day long and come up with our next strategy, we won’t be able to keep up. Because it’s a completely new market, rules of thumb don’t apply, and we have no choice but to build up our know-how by trial and error.

Yasumitsu Shigeta, 1995 Nikkei Business

Riding the waves of the telecom boom, HIK reported sales of ¥23b in 1995 and Shigeta took the company public at the age of 32. He was the youngest founder in Japan’s corporate history to go public.

This is the major shareholders listing as of Feb 1999, just before HIK was listed:

Near Death Experience

At the height of the dot-com bubble, HIK market cap was over ¥3t, making Shigeta among the world’s richest individuals for a brief moment until everything came crashing down.

Like all telecom businesses during the dot-com era, many of them took on risky investments. HIK flourishing mobile phone business suddenly turned unprofitable due to fictitious transactions that misrepresented revenues.

This HIT SHOP fraud came to light and the stock crashed for 20 consecutive days, from peak of ¥218,000/share to trough of ¥2,220/share. That’s 99% drop, if you’re wondering!

HIK crash actually started the avalanche which burst the dot-com bubble.

Reverse & Rebuild

After seeing his networth almost wiped out, Yasumitsu Shigeta is not a person who gives up easily. It was time to rebuild his company.

HIK decided to close 1,041 HIT SHOP stores and switched back to directly managed stores. In a few years time by 2003, HIK renamed the segment as “SHOP business” with only 394 stores.

HIK recorded a loss of ¥52b in relation to the store closures. Its venture investments also recorded a loss provision of ¥10b. To cover these losses, HIK sold its SoftBank shares recording a gain of ¥80b.

The financial situation worsened due to weak business performance as the economy went into recession. HIK was high on debt with ¥231b as at March 2000, but managed to reduce it to ¥37b by March 2003.

Shifting the company towards more stable revenue streams such as corporate telecom services and insurance, they reduced its reliance on volatile consumer mobile phones. Shigeta and his management team realised the true value of recurring revenues.

Steady revenue growth ensued from the depths of ¥710b in 2002, increasing every year to ¥3,489b in 2010.

Since 2010, HIK has rebuilt itself with a diversified operations across telecom, IT services, insurance, utilities (electric & gas) and beverages (subscription beer/water servers).

And this is where we start to breakdown the business model of modern HIK…

Diversified & Recurring

The business model focuses on collecting “recurring revenue” types of businesses under its umbrella. Since the traumatic dot-com bubble experience, HIK has focused on recurring revenue streams (82% of revenues is recurring) across a variety of industries and reinvesting the cashflows back into the business and/or their investment portfolio.

Management focuses on 3 questions:

How much does it cost to acquire?

How long will they be in contract for?

What is the ROI over time?

We are not aware of the criteria that would cause them to exit a business but one of their KPI is to achieve above 30% IRR for their operating business.

HIK looks for contracts that can span multiple years which are selling products on a recurring basis to SMEs and consumers. To do this, HIK is willing to take losses in the beginning but must ensure profits over the long run.

The diversity of businesses is truly unique. It can be anything from internet subscriptions to water server subscriptions. In fact, Premium Water Holdings (2588.T), a company that produces and delivers mineral water, was acquired by HIK.

Another example is DreamBeer which started in 2020. This provides a subscription beer server which can sends a batch of craft beer from regional areas of Japan either bi-weekly or monthly.

What HIK end up with is a funnel for diversified recurring revenue stream, increasingly creating a uncorrelated business portfolio that is not dependent on a single industry.

HIK has relationships with a massive network of 1.3 million corporate customers, 4 million consumers and 1,000 sales partners which houses more than 20,000 sales staff. Of this, 1/3 are run by former HIK employees. They also have exclusivity agreements with their partners to ensure that they don’t sell competitor products.

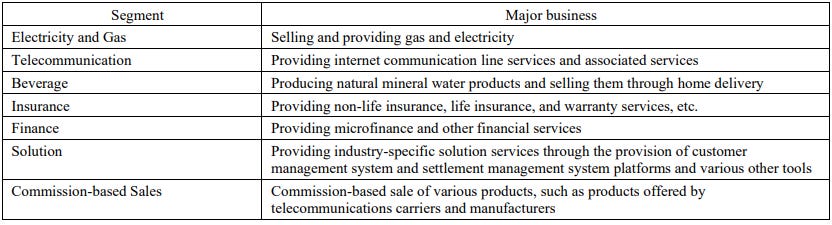

These are the description of their reportable segments:

Investment Operations

Equity portfolio

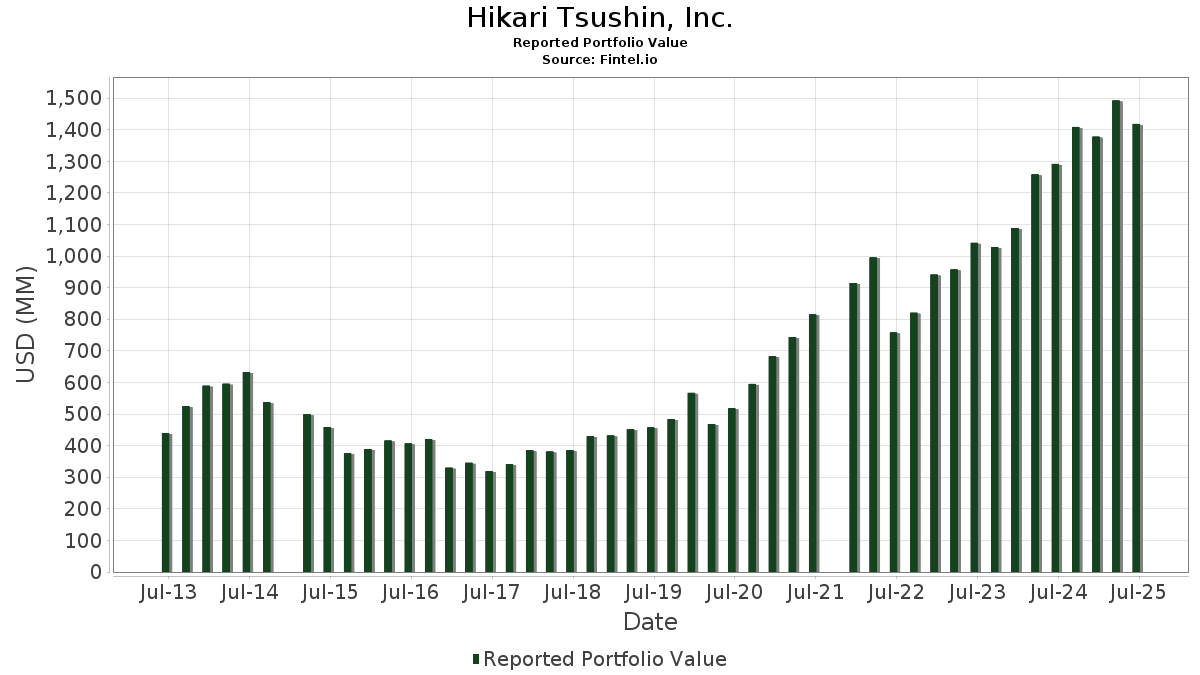

HIK core operating businesses delivers the highest yield, they can produce a 5-year IRR of ~30%. Some recurring businesses have a long lifetime value of 10 to 15 years. Management would like to invest everything back into the business, but of course that is not possible. So the excess cash is invested in public equities.

Today the equity portfolio is worth ¥1.2t (US$8.2b). 80% is in Japanese stocks, remaining 20% in US stocks, below is the US portfolio value over time:

The allocation is concentrated, with most of it in Berkshire Hathaway:

BRK.A 57.9%

GOOGL 7.4%

BKLN Senior Loans ETF 3.7%

VOO Vanguard S&P500 ETF 2.9%

Visa 2.5%

There’s no disclosure of what Japanese stocks they own.

Operating approach

The head of investment is Masato Takahashi who was previously Director and GM of financial planning department. His small team is just 3 other internal staff, no professional money managers are involved.

HIK has no investment committees and each team member get full autonomy on their decisions. They see the Japanese equity market as an extremely asymmetric opportunity set for high-quality companies with recurring profits selling at very cheap valuations.

Management has also explained that they are willing to borrow at very low rates to put more money into these undervalued shares. However, they have a rule: cash must cover all interest-bearing liabilities maturing in the next 3 years. Anything above that is investable excess cash.

If management cannot find anything desirable, they will return excess cash to shareholders through buybacks and dividends.

Valuation approach

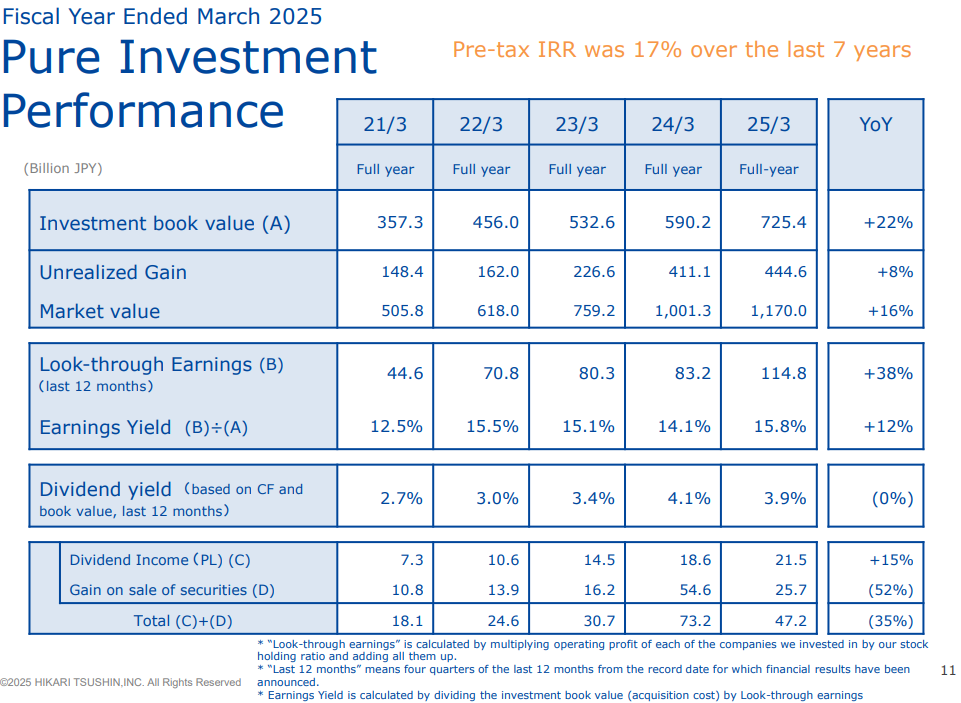

We just had to look at this page from the 2025 investor presentation and was immediately impressed by the way they think about value:

A few things stand out:

Pre-tax IRR was impressive at 17% for the last 7 years.

Using the concept of “look-through earnings” which is the operating profit of each invested company multiplied by HIK’s ownership %.

Very high earnings yield.

Core Business

Electricity & Gas [FY2025 revenue ¥288b (+37.8% YOY); op margin 12%]

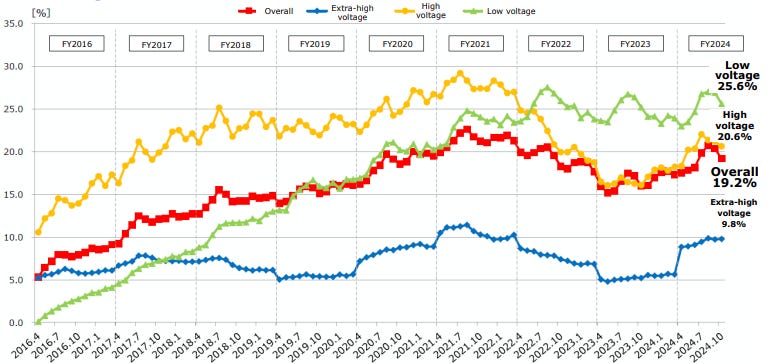

In April 2016, Japan fully liberalized electricity retailing allowing all consumers to choose their electricity provider. Since then, the share of power producer and supplier (PPS) has been increasing:

In 2022, HIK was ranked 4th in terms of market share, in just 3 years it’s ranked 2nd today.

Telecom [FY2025 revenue ¥123b (+3% YOY); op margin 21%]

The telecom segment mainly provides SMEs and individual customers with internet communication line services and associated services.

Beverage [FY2025 revenue ¥79b (-2.2% YOY); op margin 10%]

The water delivery industry grew at 7% CAGR since 2010. HIK grew much faster at 15% CAGR.

In 2015, HIK went in full-scale and had a 10% market share in terms of number of customers. Ten years later, in 2024, they have tripled market share to 30%.

Insurance [FY2025 revenue ¥27b (+12.9% YOY); op margin 31%]

They sell general insurance that has small sum assured and short-term in nature. It can be grouped into 2 parts:

Mobile phones insurance: Coverage for repair cost.

Anshin Sumairu home insurance: Coverage for household goods, liability for damages to landlords, liability for damages to third party, repair cost of rented rooms.

No long-tail or life/health related risk.

Finance [FY2025 revenue ¥33b (+9.7% YOY); op margin 54%]

This segment provides microfinance and other financial services.

Solutions [FY2025 revenue ¥28b (-2% YOY); op margin 9%]

This segment provides SMEs with industry specific solution services through the provision of customer management systems and settlement management platforms.

Commission-based Sales [FY2025 revenue ¥108b (-1.5% YOY); op margin 11%]

This segment mainly engages in commission-based sales of various products, such as products offered by telecom carriers and manufacturers, targeting SMEs and individual customers.

Management

Founder: Yasumitsu Shigeta

The details of Yasumitsu Shigeta are obscure despite the size of the business he managed to build. Shigeta has been meticulous in maintaining his privacy.

One interview that provided a hint of what kind of CEO he was came from Koji Yamamoto, who was one of the top-class salesmen at HIK and had become a Director at the young age of 28. He has since started his own company and also has a YouTube channel where he discusses his business and sometimes touches on his past experiences at HIK. On this video, he was asked by his colleague about Shigeta and he’s reluctant to talk about it from the start. But he did say some useful points:

Shigeta was a philosopher, thinking deeply about everything, including shareholder capitalism. He had a single minded goal of generating profits and wealth.

Meeting with him discussed only ROI and IRR, which in the context of Japan was a very rare trait.

Shigeta thinks of opportunities like an investor, whether the new businesses were worthwhile investments.

He would focus on one thing, then after achieving it, he totally delegates it to his subordinates and move on to the next thing.

He was not afraid of using debt as long as the financing made economic sense.

KPIs were set to only one or two key items, he believed in keeping things simple and focusing to win where competition is weak.

Shigeta doesn’t care about his colleagues’ private lives. It all just business matters.

New CEO: Hideaki Wada

Shigeta moved on to Chairman and Hideaki Wada took over as CEO in 2019. He’s a long-time employee who joined in 1997 right after graduating from university, and climbed his way up the corporate ladder. He was the #1 performer in the country among new hires and got promoted only after 5 months.

This points to an important culture of meritocracy which is actually an uncommon feature in corporate Japan.

Management fosters a culture of frugality, customer focus and willingness to adapt. Of course, the key is always hyper focused on ROI.

Look at the run down building of their HQ in Ikebukuro, talk about frugality:

Hideaki Wada’s CEO term is renewed on a yearly basis. He has made this statement:

[…] if I were to produce no results in a given year, I believe I would step down. If an exceptional next-generation leader were truly ready to take over, I would have no hesitation in handing over the role, even as soon as tomorrow.

Therefore, I have no predetermined commitment like “I’ll stay for another 10 years”. I do feel a desire to pass the baton to a younger generation as early as possible. On the other hand, there are also inspiring examples like Mr. Charlie Munger of Berkshire Hathaway, who remained active until the age of 99.

So, as long as I believe that Hikari Tsushin can deliver the best possible performance with me as its CEO, I intend to continue. Ultimately, though, that decision rests with our shareholders.

Hideaki Wada, CEO, Q4 2025 earnings call

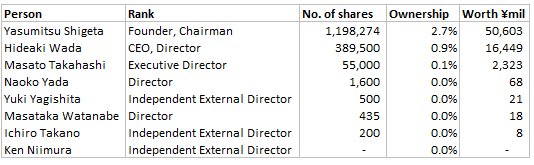

Insider Ownership

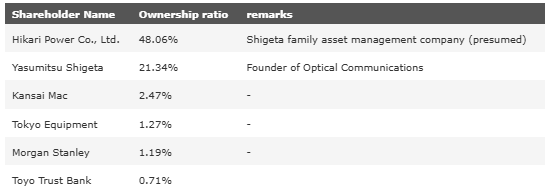

The majority of Shigeta’s wealth comes from a 39% stake in HIK.

Shigeta holds shares through a 79% stake in Tokyo-based holding company Hikari Power (along with his wife and children). Shares held by his family are credited to Shigeta to reflect his status as founder and chairman. About 4% of these shares are pledged.

The table below shows direct ownership only:

HIK grants 20% incentives to members of the employee shareholding association. We think this is a discount given to internal staff wanting to buy HIK shares(?)

They claim that executive directors have most of their networth in HIK shares. Another interesting point is that all executive officers purchase HIK shares every month. However, we don’t know if this is simply gifted SBC(?)

The CEO, Hideaki Wada disclosed some very interesting facts:

HIK is the only company he owns, he doesn’t own any other company.

Since 1991, every month he has been accumulating shares of HIK.

He’s happier being paid in dividends than in salary.

Compensation calculated as a % of equity capital (similar to a fund manager).

Recurring earnings growth % is his bonus.

As a result of this high founder ownership, the free float is only 40%. Effectively based on the above points, we can think of this as a family business with management devoted to increasing shareholder value.

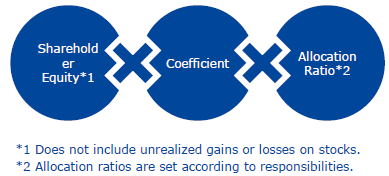

Incentives Structure

The remuneration for directors depends on shareholder equity:

Individual compensation is set based on each director’s contributions and achievements in their respective areas of responsibility. Evaluation metrics include things like operating profits, growth in recurring profits and earnings yield of the investment portfolio.

Latest News

In March 2025, HIK announced that they hired 100 student interns and commenced the planning, development and sale of AI-driven services. And conducting programming training for management-level staff.

They plan to sell AI call center services specialized in making appointments and AI generated sales materials such as quotations and proposals.

HIK does not intend to allocate capital into vague possibilities and after about 1 to 2 years of discussions with various AI vendors, they concluded that it’s faster to build it themselves. They explain that the reason is outsourcing AI development incurs high costs and once they start using an external service, all the data tends to be stored on the vendor’s servers, making it difficult to terminate the contract. Therefore, they want to be a “provider” rather than “user”.

Nothing innovative here, simply spawning more recurring revenue types of businesses.

Valuation

In the FY2024 presentation, page 17 contained an estimate of intrinsic value calculated by management. They did this because they believed that HIK shares were very undervalued at that time (~¥27,700/share).

Now, 1.5 years later, the shares are trading at ¥42,200 (+52%).

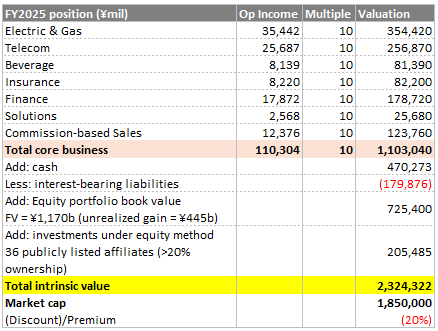

As a reference, in March 2024, management thinks that intrinsic value should be ¥2.5t. We independently worked out ¥2.3t using FY2025 numbers:

Apparently there’s still some 20% discount. At current market cap of ¥1.85t, the implied operating income multiple is only 6x. We think this is too low for the recurring quality and margins of these segments.

Note that we are not even counting the unrealized gain of ¥445b. If we add it in the estimate would be ¥2.8t.

Management stopped publishing their intrinsic calculation, stating that over the past year its shares have appreciated substantially, and so they think the undervalued situation is not as extreme anymore.

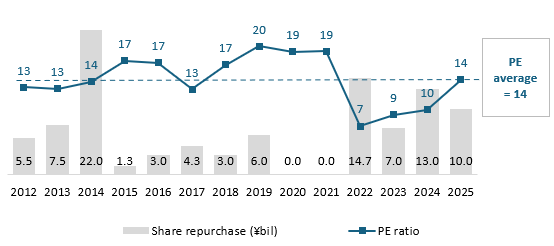

Roughly speaking, we can see that shares repurchases increase when the shares are cheap on a PE basis. The buybacks are low when the PE is higher than average:

Risks

We would like more disclosure in the financial statements, this is a common problem in the Japanese market.

For example, we are not sure how HIK sells electricity & gas without owning the production assets. It seems like the utilities supplier provides HIK, and then HIK sells to the consumers and pays the suppliers. We don’t know why suppliers require HIK to act as the middleman?

It could be the Japan Electric Power Exchange (JEPX) facilitates the trading of electricity between power generators and retailers.

Retailers then sell electricity to consumers, offering various plans and pricing options.

Suppliers might be leveraging on HIK strong consumer network and sales force?

The economic moat of the core business is not very clear to us.