4275.T: Carlit

Intro

This post explores the business of Carlit, a small Japanese firm that controls a critical resource production of ammonium perchlorate (AP).

Carlit was founded in 1918 when a pharmaceutical division was established at the Asano Family Company. Manufacturing and sales patents were obtained for “Carlit Explosives” based on technology licensed from Sweden.

In 1964, Carlit started producing AP kicking off Japan's space program. The company enjoyed stable growth and had several business lines spawned along the way…

Metal electrode manufacturing (1983)

Silicon Technology Corporation (1994)

Hazard material assessment (1997)

JC Bottling (1991)

Toyo Springs Industrial (2014)

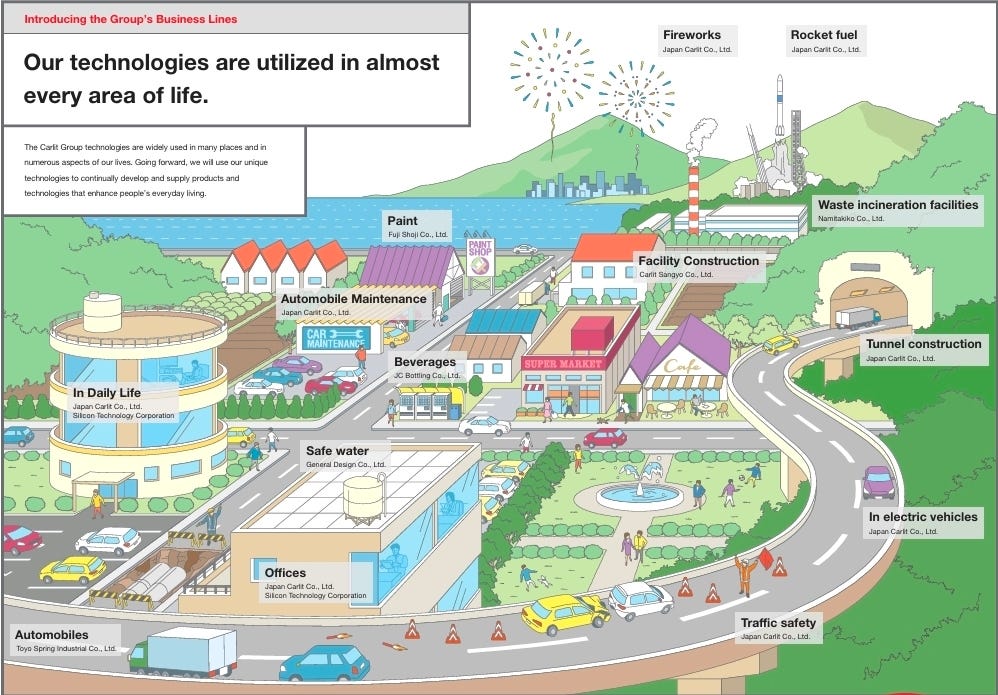

Taken as a whole, Carlit is a diversified industrial conglomerate. This pictogram describes it well:

Except for a Shanghai office, all their sales offices and plants are situated across their home country Japan.

What piqued our interest in that Carlit is the only producer of AP in Japan.

Let's understand what is this chemical compound and why it is important for Japan's defense plans.

What is Ammonium Perchlorate (AP)

The primary use of AP is in making solid rocket propellants. When AP is mixed with a fuel, it can generate self-sustained combustion at pressures far below atmospheric pressure.

Earth’s upper atmosphere and space contains little to no oxygen, so missiles and rockets have to carry their own source of oxygen for combustion. This is where AP comes in.

AP is an oxidizer, which means when ignited, it decomposes rapidly and produces oxygen needed for combustion in space. AP comprises 50–70% of the weight of the solid propellant.

There is no other oxidizer that can match AP’s combination of high performance, cost, and track record. This compound has been used globally as the dominant oxidizer for the last 70 years.

Why is AP Important to Japan

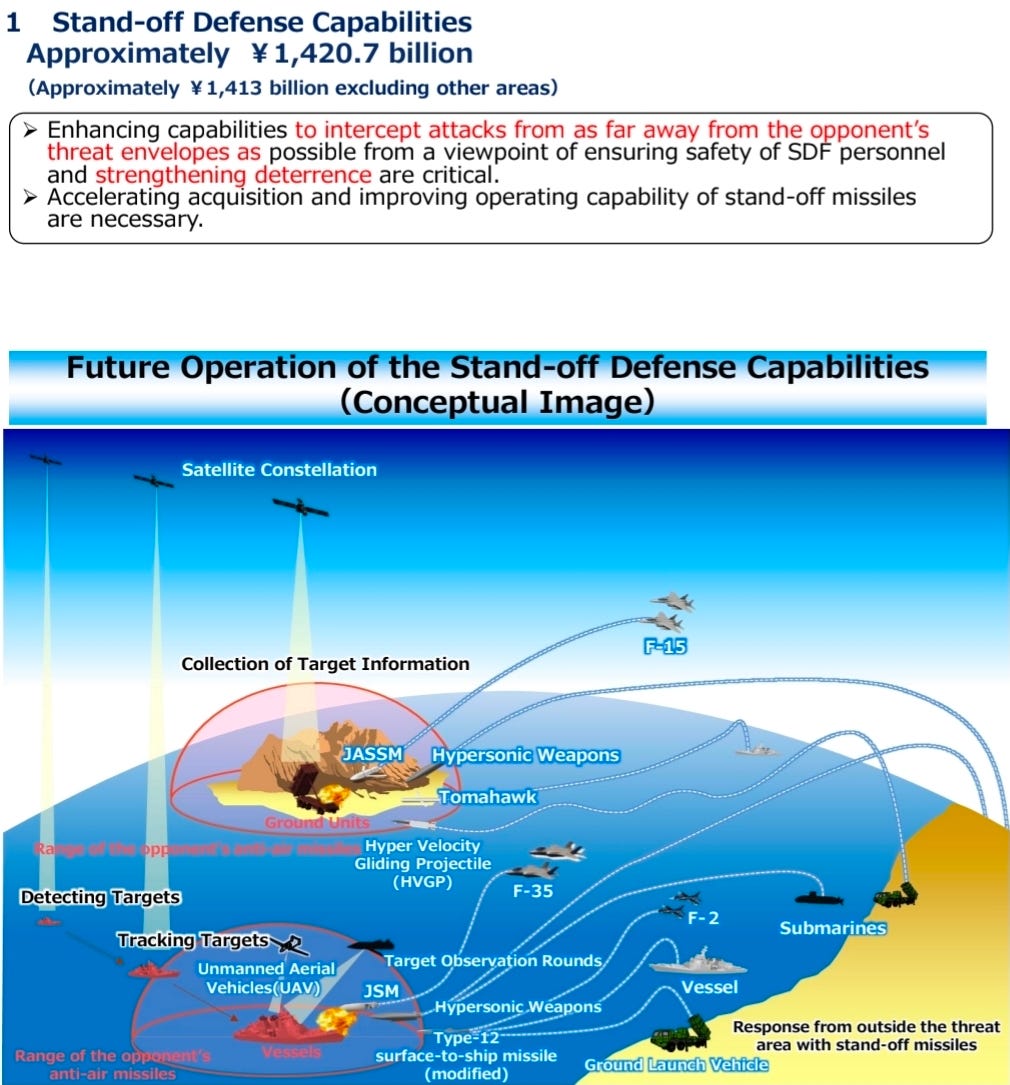

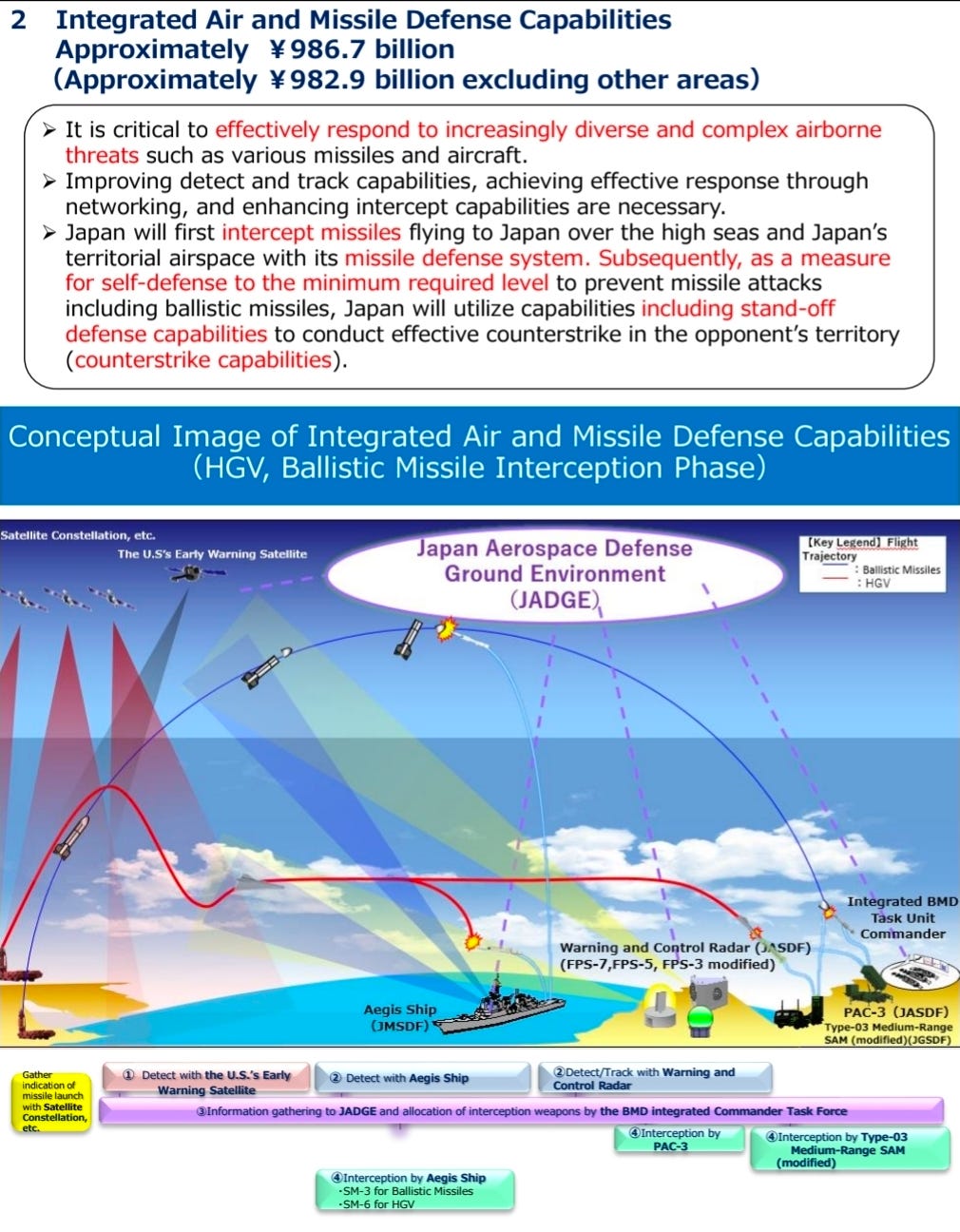

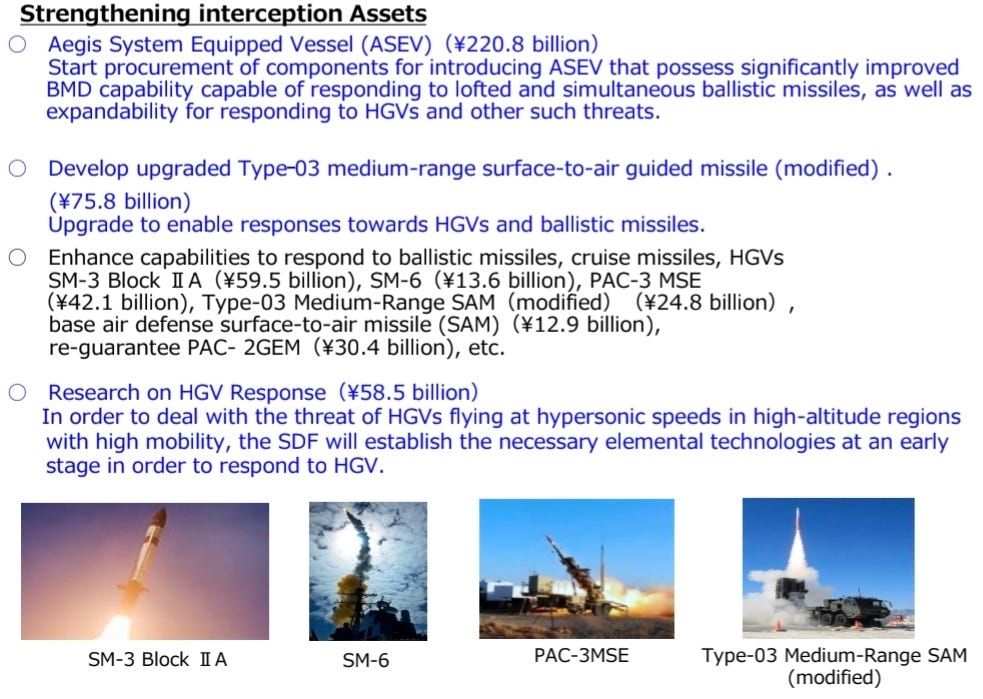

Japan stands out for having underinvested in missiles “peacetime” defense. It is now playing catch up. Japan’s defense spending plans for FY2019–23 versus FY2023–27 illustrate the scale of this shift:

Budget for “stand-off defense capabilities” will jump from ¥0.2t to ¥5t! This covers offensive ground/sea/air missiles.

Budget for “integrated air and missile defense capabilities” will rise from ¥1t to ¥3t. These are defensive systems to intercept incoming missiles.

Budget for “cross-domain operation capabilities” will increase from ¥3t to ¥8t, which includes investments in the space domain.

The most notable increase in this period occurred in FY2023, where the budget jumped by a historic 27.4% YOY, reaching approximately ¥6.8t. This was a clear departure from the previous informal limit of around 1% of GDP.

In the first few pages of the FY23 5 year plan, it's all about missles:

Supply Chain of AP

Carlit will be a direct beneficiary, since the company is Japan’s monopoly supplier of AP to both the defense and space programs (with defense expected to be the bigger contributor to growth). Currently, 100% of Carlit’s AP production is consumed domestically. Japan’s rising demand alone is absorbing all the capacity but in the future we think there could also be a market for exports.

Because of the drastic budget increases, Carlit is currently undergoing AP capacity expansion that will increase its total production by 2–3x.

Total investment is ¥2.5b of which ¥1.5b is completed. Overall, expected to be complete in the second half (by March 2026). Full operations to begin from April 2026 onward.

The supply chain works as follows:

Carlit produces AP and supplies it to NOF Corp.

NOF blends the AP with other materials to manufacture solid propellant.

NOF delivers the solid propellant to IHI Corp.

IHI integrates it into a rocket motor, before supplying to final assemblers such as Mitsubishi Heavy Industries.

NOF itself is undertaking a major capacity expansion for solid propellant, with completion timeline around September 2027. Since Carlit’s expansion will be finished by March 2026, there will be a lag before sales ramp up.

Competitive Moat

For a chemical producer, we are concerned if Carlit's monopolistic position is durable, because the production of chemicals is generally speaking not sophisticated. However, for the chemical AP, it has actually quite high barriers to entry.

This feature is not only unique to Japan.

AP production in most countries operate under a mono/duopoly structure:

United States: Duopoly (American Pacific and Northrop Grumman) with American Pacific main supplier.

Europe: Duopoly (French state-owned Eurenco and ArianeGroup, which is a JV between Airbus and Safran).

UK: Monopoly (Chemring).

Russia: Monopoly (state-owned ANOSIT).

India: Monopoly (state-owned APEP). Solar Industries and Premier Explosives are trying to enter.

The exception is in China where multiple state-owned entities produce AP.

If we go back further in time, there were actually more producers doing AP. For example, the US had a few producers during the Cold War (PEPCON, Kerr-McGee, WECCO, AP&CC, AMPAC). But decades of industry consolidation driven by defense budget cutbacks reduced the number of suppliers.

Now that governments are increasing defense budgets, AP has emerged as a chokepoint. Every country wants more AP suppliers, but the challenge is that introducing new suppliers is not easy.

Qualification Process

The chemical composition of AP is sensitive because missiles are sophisticated things; a small difference in chemistry can affect performance. Therefore, while producing AP is not a difficult process, getting a consistent chemistry profile is non trivial.

This means each weapons program has its own qualification process for a new supplier, and this takes a lot of time and cost.

Mission Critical, Low % Cost

The cost of AP as a % of total ballistic missile launch cost is tiny. But without AP the missile can't function. To spend money and time to qualify for new suppliers is a waste of resources.

Another reason is that missiles are designed to be stockpiled for decades, so degradation of AP over time is a key concern.

Hazardous Material Regulation

AP is extremely hazardous in nature, and licenses and production sites are tightly regulated. The risks are real, for example, in 1988, PEPCON suffered 2 massive explosions resulting in 2 deaths, 372 injuries, and $100m in damages to buildings.

There is also the need for strict export controls, as AP is easy to smuggle to make dangerous weapons. Hence, governments strictly regulate exports and vet suppliers; the regulatory barriers are high.

Therefore, producers with licensed facilities that already have their AP qualified and integrated into existing weapons programs enjoy a big competitive moat.

In fact, the barriers are so high that even with governments actively trying to diversify suppliers, new entrants have hard time breaking in.

The US market serves as a great case study:

In the US, AMPAC has been the monopoly AP producer, supplying the US government since the 1950s.

Northrop Grumman tried to enter recently. It built its first AP production and received a generic qualification in 2021, but progress has been slow.

AMPAC itself has traded hands several times. The Huntsman family bought it in 2015, sold it to AE Industrial Partners in 2020, and in January 2024 it was acquired by publicly listed Newmarket Corp for $700m.

Newmarket now reports AMPAC under its “Specialty Materials” segment. In 2024, AMPAC delivered $141.2m sales and $17.5m operating profit. Implying an acquisition multiple of 40x forward operating profit, not a cheap price due to the favourable economics.

Vertical Integration

Carlit also produces sodium chlorate and sodium perchlorate which are key inputs in the AP production process with other industrial applications.

This vertical integration is another advantage for Carlit. For a competitor to be cost competitive, it would also need to vertically integrate.

Expanding Upstream

Carlit is expanding beyond AP production into the design and production of solid propellant to capture more value up the chain. Although it has been supplying solid propellant to Japan’s space programs since 2017, but on the defense side (missiles) Carlit has so far only supplied AP.

Carlit is now investing ¥8b to build solid propellant capabilities with plans for experimental mass production in 2027 and commercialization in 2028.

Exporting is also possible. For example, China and Russia already exports AP to Iran. If allied nations face industrial bottlenecks or if conflict in Europe intensifies, Japan could very plausibly step in as a supplier of AP.

Business Segments

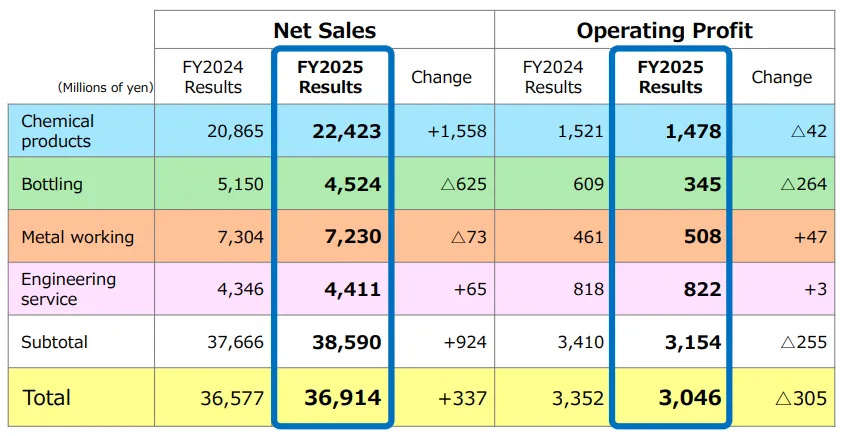

Carlit reports in 4 segments:

Chemical products

Bottling

Metal working

Engineering service

AP actually is a small proportion of sales for Carlit, but we are expecting it to increase sharply (fiscal year ends March):

Although all segments are making operating profits, there are some obvious value destructive segments. For example, bottling and silicon wafer segments are not in their area of expertise, and they have faced decreasing sales.

Engineering services produce the most operating margins 17.6% but the dollar quantum is expected to fall in FY2026 due to industrial paints and painting work impacted by the poor construction machinery market. For engineering and construction work, there are fewer projects compared to FY2025.

AP is subsumed in chemicals segment, FY2026 they are expecting ¥1.55b operating profits, management has commented the increase will be supported by more AP sales, trend is similar to prior years.

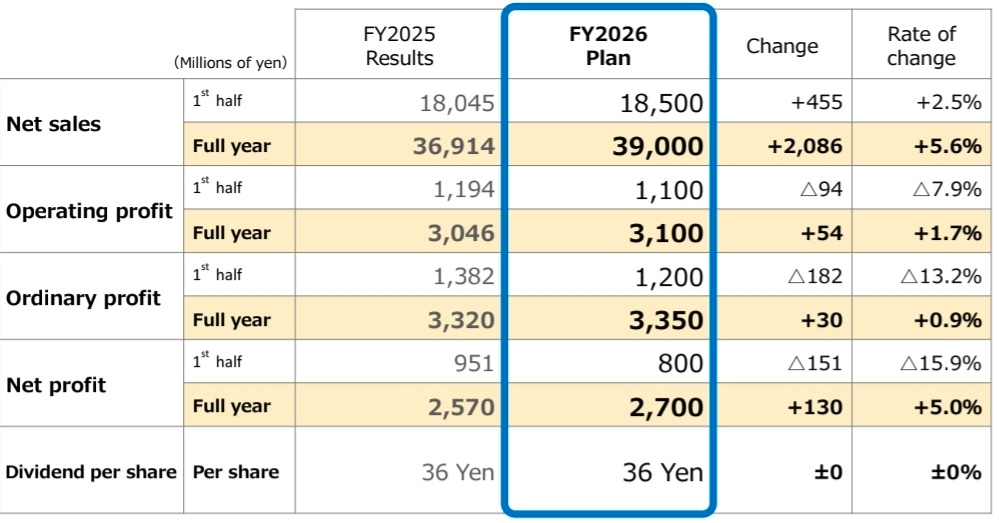

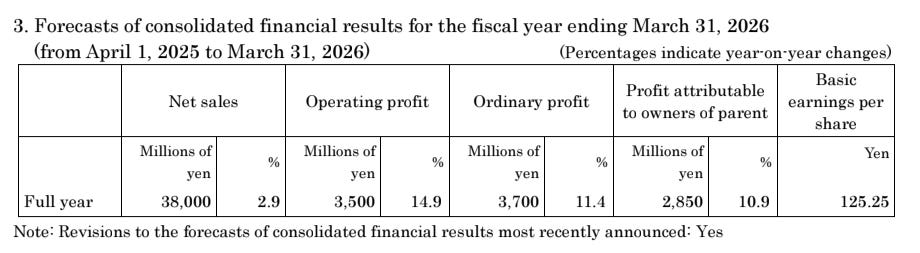

Below is the consolidated plan for FY2026:

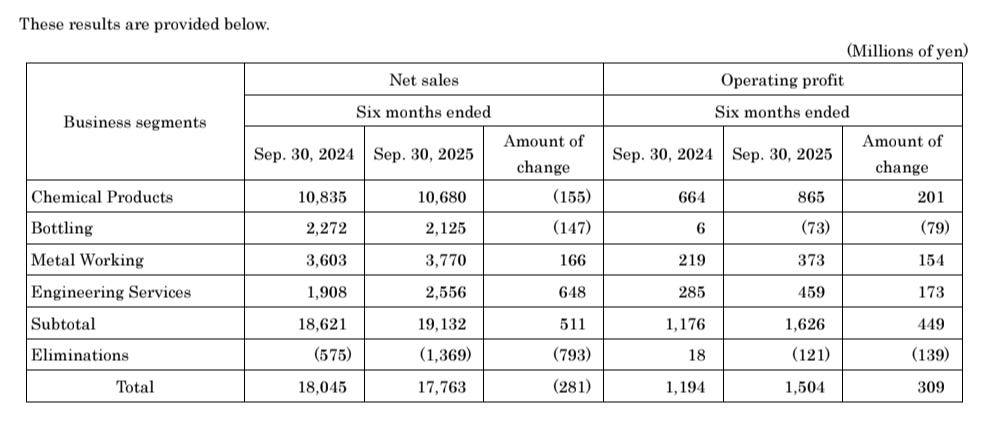

1H2026 Updates

We have reported data on 1H2026, sales is lagging behind at ¥17.8b, but operating profits are ahead at ¥1.5b. Net profit is also better at ¥1.15b.

Management has improved the FY2026 forecast:

Breaking down the segments, we can see that profitability of chemicals have improved significantly. Management commented:

Sodium chlorate sales and profit decreased due to a decline in demand for paper pulp bleaching, despite efforts to ensure stable supply.

For ammonium perchlorate (the raw material in propellants for rockets and defense missiles), net sales remained flat as demand followed sales plans. Profit increased due to the impact of sales price optimization.

Electrodes experienced an increase in sales and profit due to strong replacement demand for both oxygen generation and chlorine generation applications.

Perchloric acid sales and profit decreased. There was solid demand from domestic users but overseas demand was sluggish.

Forward Guidance

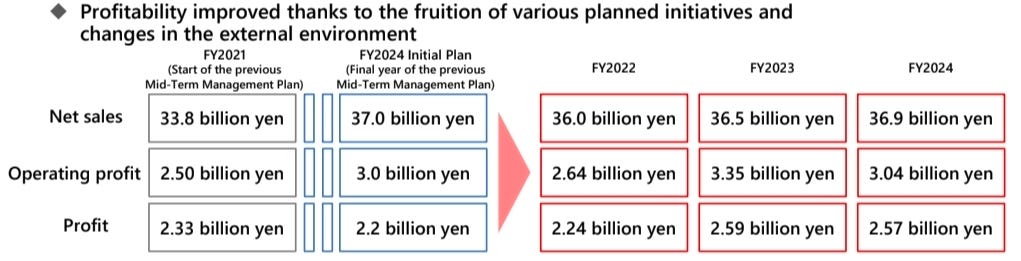

Forward guidance have been quite reliable based on historical mid-term (3 year) plan, the result for FY2024 on both top and bottom lines are very close:

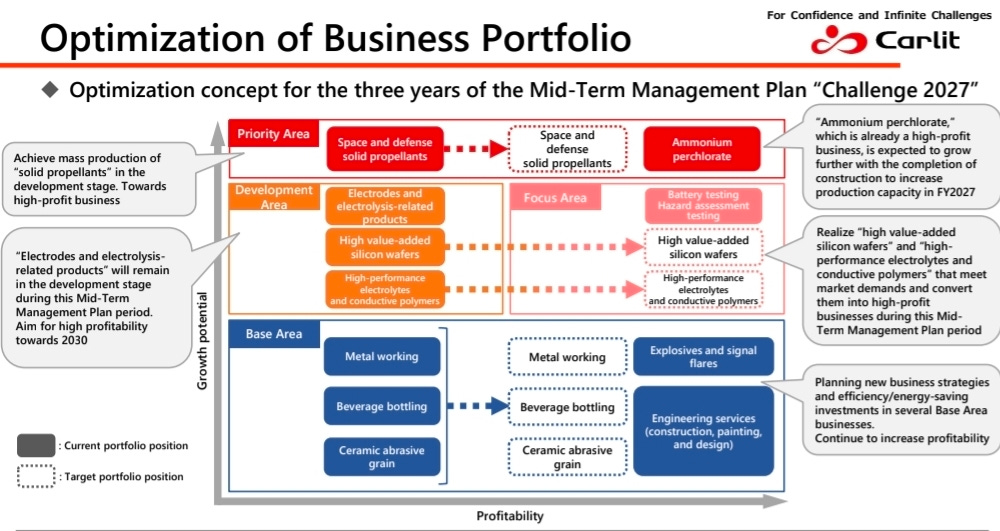

Management has then extended for FY2027 mid-term plan, the focus (red areas) is on the chemical segment, specifically AP. They have singled out this area as the highest growth + profitability:

Capital Allocation

Carlit has been reducing cross-shareholdings, freeing up cash for shareholder returns. In May 2025, Carlit announced a major buyback program of 1.3 million shares (5.4% outstanding shares). Dividend payout ratio has increased from 30% to 40% and management has explicitly stated it aims for price-book ratio >1x.

About 500k shares have been repurchased in FY2026, at cost of ¥999m, average price ~¥2000/share.

Valuation

Currently, Carlit is trading at ¥2177/share. This market re-rating has happened at market cap of ¥49.4b against net assets of ¥37.7b.

The PE ratio is at 18x.

Large-cap defense names like MHI, IHI, and KHI have already re-rated sharply too.

The attractiveness of this investment is dependent on re-rating of Carlit shares given Japan's defense spending and Carlit's monopolisitic position in AP production.

At share price ¥2177 the FY2026 forward PE is 17x, if we believe management's EPS forecast of ¥125.25.

This price is not cheap after the stock rose +87% in the past year. The largest risk for this idea is the Japan government being the largest catalyst.

We recommend building a small starter position at current price.

Risk #1: Natural/Operational Disaster

Facility explosion would be catastrophic. This is how the investment would likely fail.

Risk #2: Japan Defense Budget

Carlit’s growth is partly tied to Japan’s space/defense ambitions. Any major setbacks to Japan’s current space program would dampen future space-related demand.

Privatisation

Carlit’s small market cap is interesting considering its strategic importance as Japan’s sole AP producer. In fact it’s hard to think of another publicly listed company this small that plays such a critical role in national defense. One possible scenario is that the Japanese government pressures a larger defense company (NOF being the most logical candidate) to acquire Carlit and delist it.