3321.T: Mitachi Co Ltd

Preface: Reader interested can go here for the annual reports. FY2024 investor presentation is here. Documents are in Japanese, please use an online translator.

Net-net Situation

Mitachi is an electronics distributor based in Nagoya focusing on semiconductors and electrical components. It’s main customers are in the automotive and amusement industry, the company also has a business manufacturing electronic components and sells assembly equipment for electronic devices.

There are a few interesting points that immediately caught our attention:

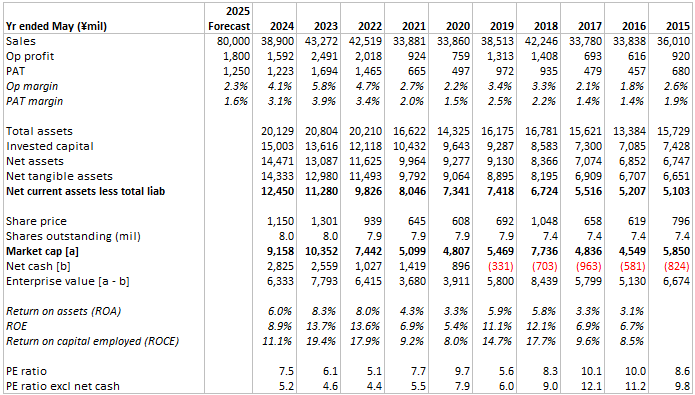

Market cap currently is ¥9.1b with a net cash value of ¥2.8b (31% of market cap).

PE of 7.5x or if we take out net cash, the PE is 5.2x.

Dividend yield is about 4% which is high compared to Japan’s cash rate.

Average ROE of 9.5% over the last 10 years (better than typical net-net stocks).

Since 2002, Mitachi only had one unprofitable year in 2012. It made profits in the GFC and COVID.

Mitachi is forecasting ¥80b sales in fiscal year ending May 2025, this is double FY2024 sales of $39b. This seems to be due to the take over of distribution for DENSO Corporation (Japanese auto components manufacturer).

Mid-term management plan until FY2027 listed sales of ¥100b, operating profit of ¥3b (¥1.6b in FY2024) and ROE of 10% (8.9% in FY2024).

Finally, this is a net-net as Mitachi’s current assets less total liabilities of ¥12.5b exceed market cap of ¥9.1b:

On a forward-looking basis, Mitachi trades at PE of 7.3x and price-to-sales of 0.1x. If we believe the mid-term FY2027 plan, management is saying they can double operating profits to ¥3b from ¥1.6b in just 3 years.

But let’s go deeper into the business operations and management guidance…

Operating Details

Sales by region is 66% in Japan and 33% is overseas, with the largest export markets being China and Philippines. Mitachi has customer concentration, with its largest customer Aisin Group, a member of the Toyota group of companies, accounting for 29% of sales. The second largest customer is Brother Industries at 15% of sales. These customers have been top contributors for many years but still we should deem the concentration as a risk.

FY2024 was not a good year, both operating profit and sales decreased -36% and -10% YOY respectively. Mitachi’s FY2025 report notes that the company expects a recovery of operating profit to ¥1.8b.

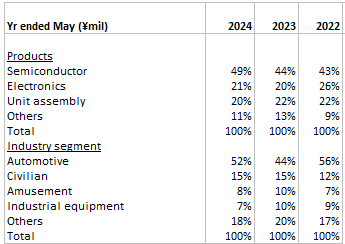

Here is a breakdown of sales by product and segment for the last 3 years:

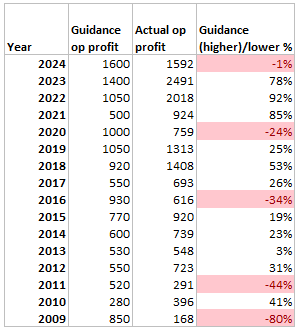

Guidance History

In net-net situations we don’t want to buy a lousy operating business just because it’s cheap. The mid-term FY2027 management’s guidance is important for this reason, and we can check their history for guidance credibility:

Out of 16 years, only 5 years were over-optimistic, we think this is quite good credibility in exercising restrain in guidance.

On 26 Dec 2024 Mitachi released the interim Q2 FY2025 report, the forecast improved slightly from prior forecast:

Sales ¥90b (up from ¥80b)

Operating profit ¥1.9b (up from ¥1.8b)

PAT ¥1.35b (up from ¥1.25b)

Why Sales in FY2025 Grew +100%?

This is due to Mitachi taking on a distribution agreement relating to DENSO Corporation. This arrangement was first announced in August 2023, but Mitachi has said sales will start in Q2 2024. This suggests that the ¥80b forecast sales for FY2025 only factors in three quarters of DENSO contribution.

To go further, since it’s not full year contribution, it seems likely that FY2026 sales will be higher than FY2025.

Details on DENSO Deal

Free deal

Mitachi didn’t pay anything to take on the DENSO sales contract from the previous distributor, Toshiba Electronic Devices & Storage Corporation (a subsidiary of Toshiba). Mitachi explains that they have been working together with Toshiba for mutual benefit under a long-term business partnership agreement, the transfer of DENSO commercial distribution has also been carried out with the aim of maximizing resources held by both partners.

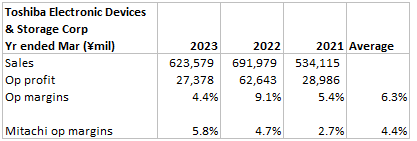

We deduce that DENSO deal should be of low margins as Mitachi is forecasting only 13% growth in operating profits compared to 100% growth in sales. The August 2023 announcement about the DENSO deal also included some financial information about Toshiba Electronic Devices & Storage Corporation.

Given that Toshiba runs at a higher margin, it is logical that Toshiba won’t give away a distribution deal for free if it was a great business. However, we also think that Mitachi’s conservative management would not take up the deal if it was onerous. It’s likely that DENSO is profitable but low margin profile, but we don’t have visibility.

Taking on More Debt

For a distribution business this size, Mitachi will require more working capital. On July 2024, it entered an agreement with major Japanese banks for a committed credit line of up to ¥20b. This amount is more than double Mitachi’s current market cap and ~40% more than the company’s current book value.

Under the arrangement, MUFG has committed up to ¥14b and Mizuho a further ¥6b. Here are the details from the announcement:

The conclusion of this agreement will enable stable and flexible fund raising, which will enable the company to meet capital needs associated with future growth. The purpose of this is to respond to changing business conditions and strengthen our financial base.

Details of the credit line:

1. Contracting parties: MUFG Bank, Ltd. and Mizuho Bank, Ltd.

2. Maximum loan amount: ¥20b (MUFG ¥14b, Mizuho ¥6b). Revolving method.

3. Contracting date: September 18, 2024.

4. Contracting period: MUFG Sep 30, 2024 to Sep 29, 2025 (one year); Mizuho Sep 25, 2024 to Sep 24, 2025 (one year).

5. Contract type: Individual bilateral agreement

6. Use of funds: Working capital

7. Collateral: Unsecured and unguaranteed

The amount of debt involved creates additional risk, especially if Mitachi loses money on the DENSO distribution.

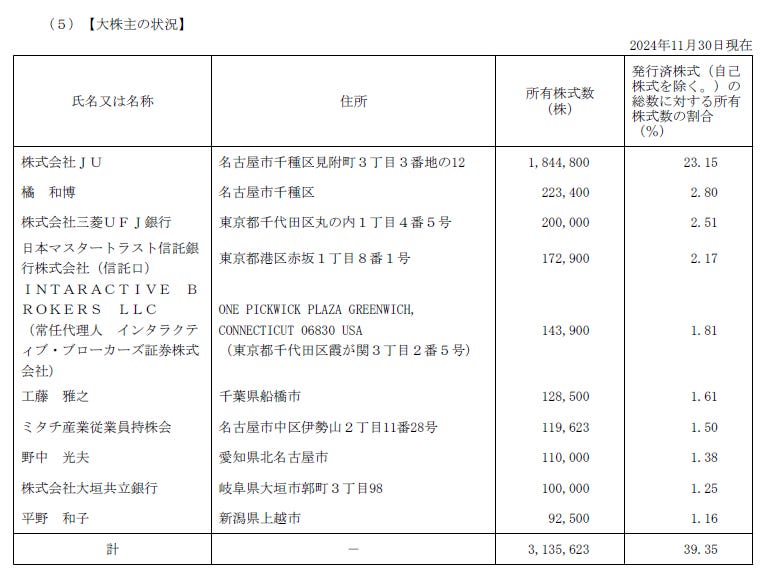

Ownership Structure

Mitachi’s largest shareholder is JU Corporation, an investment vehicle for Mitachi’s president Kazuhiro Tachibana.

JU owns 23.16% of Mitachi’s stock.

Kazuhiro Tachibana himself owns a further 2.8% of shares directly.

The next largest owners are Mitsubishi UFJ Bank 2.5% and Master Trust Bank of Japan 2.2%.

Interactive Brokers own 1.8% (this is quite interesting, we don’t know why?)

While insider ownership is good, the lack of another large shareholder means there are no real checks on the board or management, which isn’t unusual in Japan.

Attractive Situation

It boils down to expectations and valuation. Total returns can be broken down into shareholder yield (dividends + buybacks) and business performance (earnings growth).

If operating earnings can match the guidance of ¥3b in FY2027, that would imply a 21% CAGR over 3 years. Plus we get 4% dividend yield. So if operating income multiple stays the same as today, there is still a possibility of 25% CAGR over the next few years.

There are also tailwinds over the short term from higher demand of semiconductors in newer cars, which is DENSO’s and Mitachi’s key end markets. Note that these companies are simply distributors and should not be overly affected by cyclicality of the semiconductor industry as a whole.

Why This Net-net Exist?

We think these are reasons why Mitachi is mispriced:

Small company with market cap of ¥9b. This is too small to move the needle for big investors.

While Mitachi has made some disclosures about the DENSO deal and its mid-term management report, it’s possible that these filings haven’t been widely read by market participants. The stock is basically flat since August 2023, which is when the deal was announced.

Foreigners only own 6.3% of the company.

Risks

While Mitachi has been consistently profitable, the new DENSO deal could lead to losses. The company is also taking on a lot of debt to fund the increase in working capital.

We don’t have any real insights into the margin profile of the new DENSO business.

As both an importer and exporter, Mitachi is exposed to fluctuations in exchange rates.

If there was a sudden decrease in orders from customers, Mitachi could be left holding excess inventory.

Significant customer concentration.

Conclusion

We will take a position at current market cap of ¥9b (¥1,136/share).